Question: **need assistance with all problems after 5a-9** Chapter 5 Recording Capital Asset and Capital Project Transactions City Hall Annex Construction Fund and Governmental Activities at

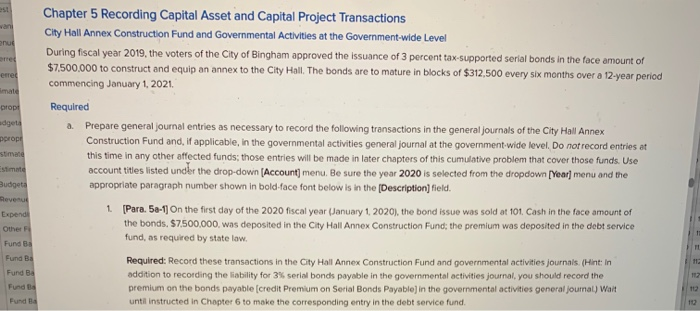

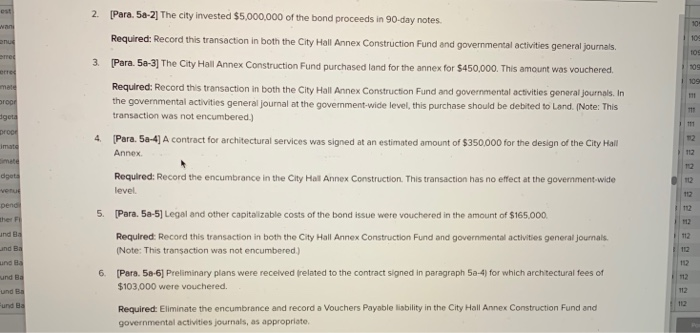

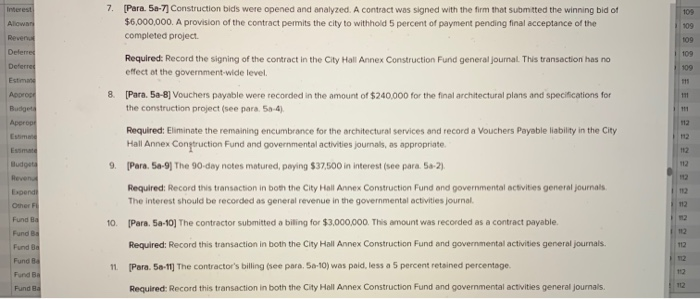

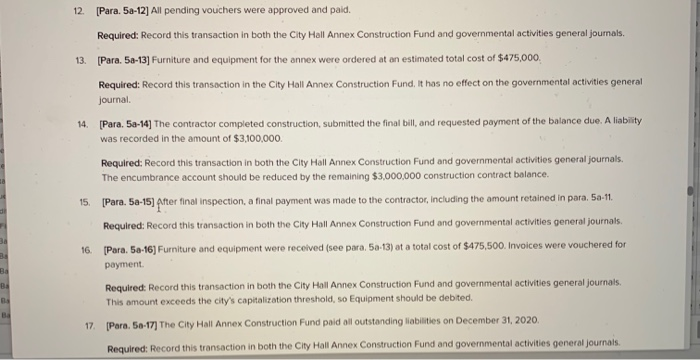

Chapter 5 Recording Capital Asset and Capital Project Transactions City Hall Annex Construction Fund and Governmental Activities at the Government wide Level During fiscal year 2019, the voters of the City of Bingham approved the issuance of 3 percent tax-supported serial bonds in the face amount of $7,500,000 to construct and equip an annex to the City Hall. The bonds are to mature in blocks of $312.500 every six months over a 12-year period commencing January 1, 2021. proot dgets prope Stima stimate udget Required a Prepare general journal entries as necessary to record the following transactions in the general journals of the City Hall Annex Construction Fund and, if applicable, in the governmental activities general journal at the government wide level. Do not record entries at this time in any other affected funds; those entries will be made in later chapters of this cumulative problem that cover those funds. Use account titles listed under the drop-down (Account) menu. Be sure the year 2020 is selected from the dropdown (Year) menu and the appropriate paragraph number shown in bold-face font below is in the Description] field. 1 Para 50-1] On the first day of the 2020 fiscal year (January 1 2020), the bond issue was sold at 101 Cash in the face amount of the bonds. $7,500,000, was deposited in the City Hall Annex Construction Fund; the premium was deposited in the debt service fund, as required by state law. Other Fund Be Fund Be Fund B Required: Record these transactions in the City Hall Annex Construction Fund and governmental activities journals. (Hint: In addition to recording the liability for 3 serial bonds payable in the governmental activities journal, you should record the premium on the bonds payable (credit Premium on Serial Bonds Payable in the governmental activities general journal) Wait unti instructed in Chapter 6 to make the corresponding entry in the debt service fund. 2. Para. 5a-2] The city invested $5,000,000 of the bond proceeds in 90-day notes. Required: Record this transaction in both the City Hall Annex Construction Fund and governmental activities general journals. 3 Para. 50-3] The City Hall Annex Construction Fund purchased land for the annex for $450,000. This amount was vouchered Required: Record this transaction in both the City Hall Annex Construction Fund and governmental activities general journals. In the governmental activities general journal at the government-wide level, this purchase should be debited to Land. (Note: This transaction was not encumbered.) prope 4 Para 50-4] A contract for architectural services was signed at an estimated amount of $350,000 for the design of the City Hall Annex geta Required: Record the encumbrance in the City Hall Annex Construction. This transaction has no effect at the government wide level 5. Para. 50-5] Legal and other capitalizable costs of the bond issue were vouchered in the amount of $165.000 Required: Record this transaction in both the City Hall Annex Construction Fund and governmental activities general journals. (Note: This transaction was not encumbered) 6. Para 50-6] Preliminary plans were received related to the contract signed in paragraph 50-4) for which architectural fees of $103,000 were vouchered. Required: Eliminate the encumbrance and record a Vouchers Payable liability in the City Hall Annex Construction Fund and governmental activities journals, as appropriate 7. [Para 5a-7) Construction bids were opened and analyzed. A contract was signed with the firm that submitted the winning bid of $6,000,000. A provision of the contract permits the city to withhold 5 percent of payment pending final acceptance of the completed project Interest Allowan Reven Deferred Deferre Estimand Required: Record the signing of the contract in the City Hall Annex Construction Fund general journal. This transaction has no effect at the government-wide level. Apprope [Para. 5a-8] Vouchers payable were recorded in the amount of $240,000 for the final architectural plans and specifications for the construction project (see para 5a-4) Budget Approp Required: Eliminate the remaining encumbrance for the architectural services and record a Vouchers Payable liability in the City Hall Annex Contruction Fund and governmental activities journals, as appropriate 9. [Para. 50-9] The 90-day notes matured, paying $37,500 in interest (see para. 5a-2) Required: Record this transaction in both the City Hall Annex Construction Fund and governmental activities general journals The interest should be recorded as general revenue in the governmental activities journal Essmate Budget Revena Bendl Other F Fund Ba Fund Be Funda Funda Fund B 10. [Para. 5a-10) The contractor submitted a biling for $3,000,000. This amount was recorded as a contract payable. Required: Record this transaction in both the City Hall Annex Construction Fund and governmental activities general journals. 11. Para 50-11] The contractor's billing (see para. 5-10) was paid, less a 5 percent retained percentage Funda Required: Record this transaction in both the City Hall Annex Construction Fund and governmental activities general Journals. 12. [Para 50-12] All pending vouchers were approved and paid. Required: Record this transaction in both the City Hall Annex Construction Fund and governmental activities general journals. 13. [Para 50-13] Furniture and equipment for the annex were ordered at an estimated total cost of $475,000 Required: Record this transaction in the City Hall Annex Construction Fund, It has no effect on the governmental activities general journal 14. [Para. 5-14] The contractor completed construction, submitted the final bill, and requested payment of the balance due. A liability was recorded in the amount of $3,100,000 Required: Record this transaction in both the City Hall Annex Construction Fund and governmental activities general journals. The encumbrance account should be reduced by the remaining $3,000,000 construction contract balance. 15. [Para. 50-15) After final inspection, a final payment was made to the contractor, including the amount retained in para 50-11. Required: Record this transaction in both the City Hall Annex Construction Fund and governmental activities general journals. 16. (Para. 50-16] Furniture and equipment were received (see para. 5a-13) at a total cost of $475,500. Invoices were vouchered for payment Required: Record this transaction in both the City Hall Annex Construction Fund and governmental activities general journals. This amount exceeds the city's capitalization threshold, so Equipment should be debited. 17. Para. 56-17) The City Hall Annex Construction Fund paid all outstanding abilities on December 31, 2020 Required: Record this transaction in both the City Hall Annex Construction Fund and governmental activities general journals. 17. (Para58-17) The City Hall Annex Construction Fund paid all outstanding liabilities on December 31, 2020. Required: Record this transaction in both the City Hall Annex Construction Fund and governmental activities general journals. Total construction costs for the City Hall Annex Construction Project should be capitalized in the Buildings account in governmental activities. [Para. 50-18] Remaining cash in the City Hall Annex Construction Fund was transferred to the debt service fund. Required: Record this transaction in the City Hall Annex Construction Fund. Do not record the transfer in the debt service fund until you are instructed to do so in Chapter 6. This transaction involves two governmental funds, thus it has no effect on the governmental activities general journal. 19. Verify the accuracy of all your preceding entries in the general journals of the City Hall Annex Construction Fund and governmental activities at the government-wide level, then click (Post entries of each entity to post the entries to the respective general ledgers. For the City Hall Annex Construction Fund only prepare year-end closing entries for 2020 and post them to the fund's general ledger (Note: You must click on the box for (Closing Entry to checkmark it,"Closing Entry checkbox will appear next to the [Add credit) field for the account being closed. Be sure the checkmark is present for each account being closed.) Click [Post entries) to post the closing entry Closing entries will be made in the governmental activities general journal in Chapter 9 of this cumulative problem. Ignore those entries for now. Chapter 5 Recording Capital Asset and Capital Project Transactions City Hall Annex Construction Fund and Governmental Activities at the Government wide Level During fiscal year 2019, the voters of the City of Bingham approved the issuance of 3 percent tax-supported serial bonds in the face amount of $7,500,000 to construct and equip an annex to the City Hall. The bonds are to mature in blocks of $312.500 every six months over a 12-year period commencing January 1, 2021. proot dgets prope Stima stimate udget Required a Prepare general journal entries as necessary to record the following transactions in the general journals of the City Hall Annex Construction Fund and, if applicable, in the governmental activities general journal at the government wide level. Do not record entries at this time in any other affected funds; those entries will be made in later chapters of this cumulative problem that cover those funds. Use account titles listed under the drop-down (Account) menu. Be sure the year 2020 is selected from the dropdown (Year) menu and the appropriate paragraph number shown in bold-face font below is in the Description] field. 1 Para 50-1] On the first day of the 2020 fiscal year (January 1 2020), the bond issue was sold at 101 Cash in the face amount of the bonds. $7,500,000, was deposited in the City Hall Annex Construction Fund; the premium was deposited in the debt service fund, as required by state law. Other Fund Be Fund Be Fund B Required: Record these transactions in the City Hall Annex Construction Fund and governmental activities journals. (Hint: In addition to recording the liability for 3 serial bonds payable in the governmental activities journal, you should record the premium on the bonds payable (credit Premium on Serial Bonds Payable in the governmental activities general journal) Wait unti instructed in Chapter 6 to make the corresponding entry in the debt service fund. 2. Para. 5a-2] The city invested $5,000,000 of the bond proceeds in 90-day notes. Required: Record this transaction in both the City Hall Annex Construction Fund and governmental activities general journals. 3 Para. 50-3] The City Hall Annex Construction Fund purchased land for the annex for $450,000. This amount was vouchered Required: Record this transaction in both the City Hall Annex Construction Fund and governmental activities general journals. In the governmental activities general journal at the government-wide level, this purchase should be debited to Land. (Note: This transaction was not encumbered.) prope 4 Para 50-4] A contract for architectural services was signed at an estimated amount of $350,000 for the design of the City Hall Annex geta Required: Record the encumbrance in the City Hall Annex Construction. This transaction has no effect at the government wide level 5. Para. 50-5] Legal and other capitalizable costs of the bond issue were vouchered in the amount of $165.000 Required: Record this transaction in both the City Hall Annex Construction Fund and governmental activities general journals. (Note: This transaction was not encumbered) 6. Para 50-6] Preliminary plans were received related to the contract signed in paragraph 50-4) for which architectural fees of $103,000 were vouchered. Required: Eliminate the encumbrance and record a Vouchers Payable liability in the City Hall Annex Construction Fund and governmental activities journals, as appropriate 7. [Para 5a-7) Construction bids were opened and analyzed. A contract was signed with the firm that submitted the winning bid of $6,000,000. A provision of the contract permits the city to withhold 5 percent of payment pending final acceptance of the completed project Interest Allowan Reven Deferred Deferre Estimand Required: Record the signing of the contract in the City Hall Annex Construction Fund general journal. This transaction has no effect at the government-wide level. Apprope [Para. 5a-8] Vouchers payable were recorded in the amount of $240,000 for the final architectural plans and specifications for the construction project (see para 5a-4) Budget Approp Required: Eliminate the remaining encumbrance for the architectural services and record a Vouchers Payable liability in the City Hall Annex Contruction Fund and governmental activities journals, as appropriate 9. [Para. 50-9] The 90-day notes matured, paying $37,500 in interest (see para. 5a-2) Required: Record this transaction in both the City Hall Annex Construction Fund and governmental activities general journals The interest should be recorded as general revenue in the governmental activities journal Essmate Budget Revena Bendl Other F Fund Ba Fund Be Funda Funda Fund B 10. [Para. 5a-10) The contractor submitted a biling for $3,000,000. This amount was recorded as a contract payable. Required: Record this transaction in both the City Hall Annex Construction Fund and governmental activities general journals. 11. Para 50-11] The contractor's billing (see para. 5-10) was paid, less a 5 percent retained percentage Funda Required: Record this transaction in both the City Hall Annex Construction Fund and governmental activities general Journals. 12. [Para 50-12] All pending vouchers were approved and paid. Required: Record this transaction in both the City Hall Annex Construction Fund and governmental activities general journals. 13. [Para 50-13] Furniture and equipment for the annex were ordered at an estimated total cost of $475,000 Required: Record this transaction in the City Hall Annex Construction Fund, It has no effect on the governmental activities general journal 14. [Para. 5-14] The contractor completed construction, submitted the final bill, and requested payment of the balance due. A liability was recorded in the amount of $3,100,000 Required: Record this transaction in both the City Hall Annex Construction Fund and governmental activities general journals. The encumbrance account should be reduced by the remaining $3,000,000 construction contract balance. 15. [Para. 50-15) After final inspection, a final payment was made to the contractor, including the amount retained in para 50-11. Required: Record this transaction in both the City Hall Annex Construction Fund and governmental activities general journals. 16. (Para. 50-16] Furniture and equipment were received (see para. 5a-13) at a total cost of $475,500. Invoices were vouchered for payment Required: Record this transaction in both the City Hall Annex Construction Fund and governmental activities general journals. This amount exceeds the city's capitalization threshold, so Equipment should be debited. 17. Para. 56-17) The City Hall Annex Construction Fund paid all outstanding abilities on December 31, 2020 Required: Record this transaction in both the City Hall Annex Construction Fund and governmental activities general journals. 17. (Para58-17) The City Hall Annex Construction Fund paid all outstanding liabilities on December 31, 2020. Required: Record this transaction in both the City Hall Annex Construction Fund and governmental activities general journals. Total construction costs for the City Hall Annex Construction Project should be capitalized in the Buildings account in governmental activities. [Para. 50-18] Remaining cash in the City Hall Annex Construction Fund was transferred to the debt service fund. Required: Record this transaction in the City Hall Annex Construction Fund. Do not record the transfer in the debt service fund until you are instructed to do so in Chapter 6. This transaction involves two governmental funds, thus it has no effect on the governmental activities general journal. 19. Verify the accuracy of all your preceding entries in the general journals of the City Hall Annex Construction Fund and governmental activities at the government-wide level, then click (Post entries of each entity to post the entries to the respective general ledgers. For the City Hall Annex Construction Fund only prepare year-end closing entries for 2020 and post them to the fund's general ledger (Note: You must click on the box for (Closing Entry to checkmark it,"Closing Entry checkbox will appear next to the [Add credit) field for the account being closed. Be sure the checkmark is present for each account being closed.) Click [Post entries) to post the closing entry Closing entries will be made in the governmental activities general journal in Chapter 9 of this cumulative problem. Ignore those entries for now

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts