Question: Need help for list the detailed answer for Q2 Estimate Annual (GBP) Dec-19 Dec-20 ROE (%): 10 10 EPS: 0.80 0.9 DPS: policy of pay-out

Need help for list the detailed answer for Q2

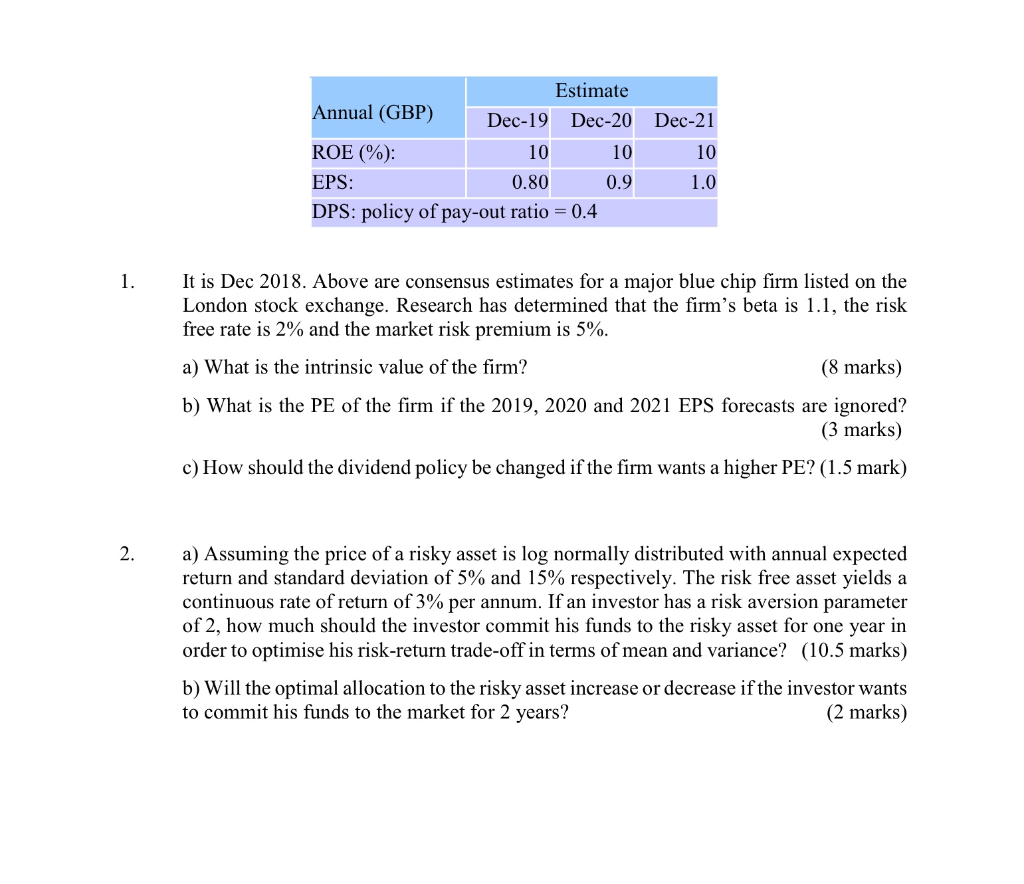

Estimate Annual (GBP) Dec-19 Dec-20 ROE (%): 10 10 EPS: 0.80 0.9 DPS: policy of pay-out ratio = 0.4 Dec-21 10 1.0 UD (70). It is Dec 2018. Above are consensus estimates for a major blue chip firm listed on the London stock exchange. Research has determined that the firm's beta is 1.1, the risk free rate is 2% and the market risk premium is 5%. a) What is the intrinsic value of the firm? (8 marks) b) What is the PE of the firm if the 2019, 2020 and 2021 EPS forecasts are ignored? (3 marks) c) How should the dividend policy be changed if the firm wants a higher PE? (1.5 mark) a) Assuming the price of a risky asset is log normally distributed with annual expected return and standard deviation of 5% and 15% respectively. The risk free asset yields a continuous rate of return of 3% per annum. If an investor has a risk aversion parameter of 2, how much should the investor commit his funds to the risky asset for one year in order to optimise his risk-return trade-off in terms of mean and variance? (10.5 marks) b) Will the optimal allocation to the risky asset increase or decrease if the investor wants to commit his funds to the market for 2 years? (2 marks) Estimate Annual (GBP) Dec-19 Dec-20 ROE (%): 10 10 EPS: 0.80 0.9 DPS: policy of pay-out ratio = 0.4 Dec-21 10 1.0 UD (70). It is Dec 2018. Above are consensus estimates for a major blue chip firm listed on the London stock exchange. Research has determined that the firm's beta is 1.1, the risk free rate is 2% and the market risk premium is 5%. a) What is the intrinsic value of the firm? (8 marks) b) What is the PE of the firm if the 2019, 2020 and 2021 EPS forecasts are ignored? (3 marks) c) How should the dividend policy be changed if the firm wants a higher PE? (1.5 mark) a) Assuming the price of a risky asset is log normally distributed with annual expected return and standard deviation of 5% and 15% respectively. The risk free asset yields a continuous rate of return of 3% per annum. If an investor has a risk aversion parameter of 2, how much should the investor commit his funds to the risky asset for one year in order to optimise his risk-return trade-off in terms of mean and variance? (10.5 marks) b) Will the optimal allocation to the risky asset increase or decrease if the investor wants to commit his funds to the market for 2 years? (2 marks)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts