Question: need help solving 1.2 and Q.2 Q1. On Friday, April 3, 2020 JD bought shares of the following stocks and held this portfolio for a

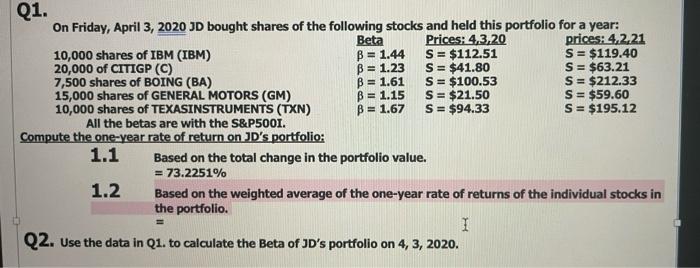

Q1. On Friday, April 3, 2020 JD bought shares of the following stocks and held this portfolio for a year: Beta Prices: 4.3.20 prices: 4.2.21 10,000 shares of IBM (IBM) B = 1.44 S = $112.51 S = $119.40 20,000 of CITIGP (C) B = 1.23 S = $41.80 S = $63.21 7,500 shares of BOING (BA) B = 1.61 S = $100.53 S = $212.33 15,000 shares of GENERAL MOTORS (GM) B = 1.15 S = $21.50 S = $59.60 10,000 shares of TEXASINSTRUMENTS (TXN) B= 1.67 S = $94.33 S = $195.12 All the betas are with the S&P5001. Compute the one-year rate of return on JD's portfolio: 1.1 Based on the total change in the portfolio value. = 73.2251% 1.2 Based on the weighted average of the one-year rate of returns of the individual stocks in the portfolio I Q2. Use the data in Q1. to calculate the Beta of JD's portfolio on 4, 3, 2020

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts