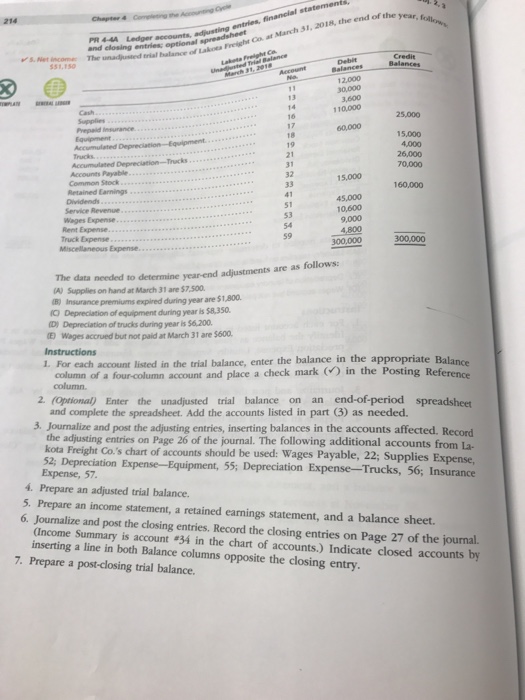

Question: Need help with 6 and 7 please type 214 PR 444 Ledger accounts and closing entries optional p The unadjusted erial balance of Lakoes S.Net

214 PR 444 Ledger accounts and closing entries optional p The unadjusted erial balance of Lakoes S.Net income 551,150 nal alance of Lakoa Freight Co at March 31, 2018, the end of the 12,000 1 10,000 16 Prepaid insurance 15,000 4,000 19 21 31 32 Accounts Payable Common Stock Retained Earnings 15,000 70.00 41 51 53 45,000 160,000 10,600 Service Revenue Wages Expense Truck Expense 59 300,000 300,000 Miscellaneous Expense neded to determine year-end adjustments are as follows: A) Supplies on hand at March 31 are $7,500. B) Insurance premiums expired during year ane $1,800. O Depreciation of equipment during year is $8,350 Depreciation of trucks during year is S6200. Wages accrued but not paid at March 31 are S600. Instructions 1. For each account listed in the trial balance, enter the balance in the appropriate Balance column of a four-column account and place a check mark in the Posting Reference (Optional) Enter the unadjusted trial balance on an end-of-period spreadsheet and complete the spreadsheet. Add the accounts listed in part 3) as needed. 3 Journalize and post the adjusting entries, inserting balances in the accounts affected. Record the adjusting entries on Page 26 of the journal. The following additional ac kota Freight Co.'s chart of accounts should be used: Wages Payable, 22; Supplies 52 Depreciation Expense-Equipment, 55; Depreciation Expense-Trucks, 56, Insurance Expense, 57. 4. Prepare an adjusted trial balance. 5. Prepare an income statement, a retained earnings statement, and a balance sheet. 6. Journalize and post the closing entries. Record the closing entries on Page 27 of the journal. (Income Summary is account #34 in the chart of accounts.) Indicate closed accounts by inserting a line in both Balance columns opposite the closing entry. 7. Prepare a post-closing trial balance

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts