Question: need help with number 4 2. (12.5pts) Let A(0) = 100, A(1) = 105, S(0) = 90 and 100, with probability : S(1) = 80,

need help with number 4

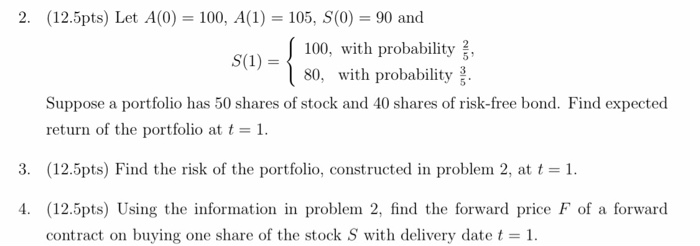

2. (12.5pts) Let A(0) = 100, A(1) = 105, S(0) = 90 and 100, with probability : S(1) = 80, with probability Suppose a portfolio has 50 shares of stock and 40 shares of risk-free bond. Find expected return of the portfolio at t = 1. 3. (12.5pts) Find the risk of the portfolio, constructed in problem 2, at t = 1. 4. (12.5pts) Using the information in problem 2, find the forward price F of a forward contract on buying one share of the stock S with delivery date t = 1

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock