Question: need help with problem below Problem 2 [15 points = 5 + 5 + 5] Let B = {B(t) : t > 0} denote a

need help with problem below

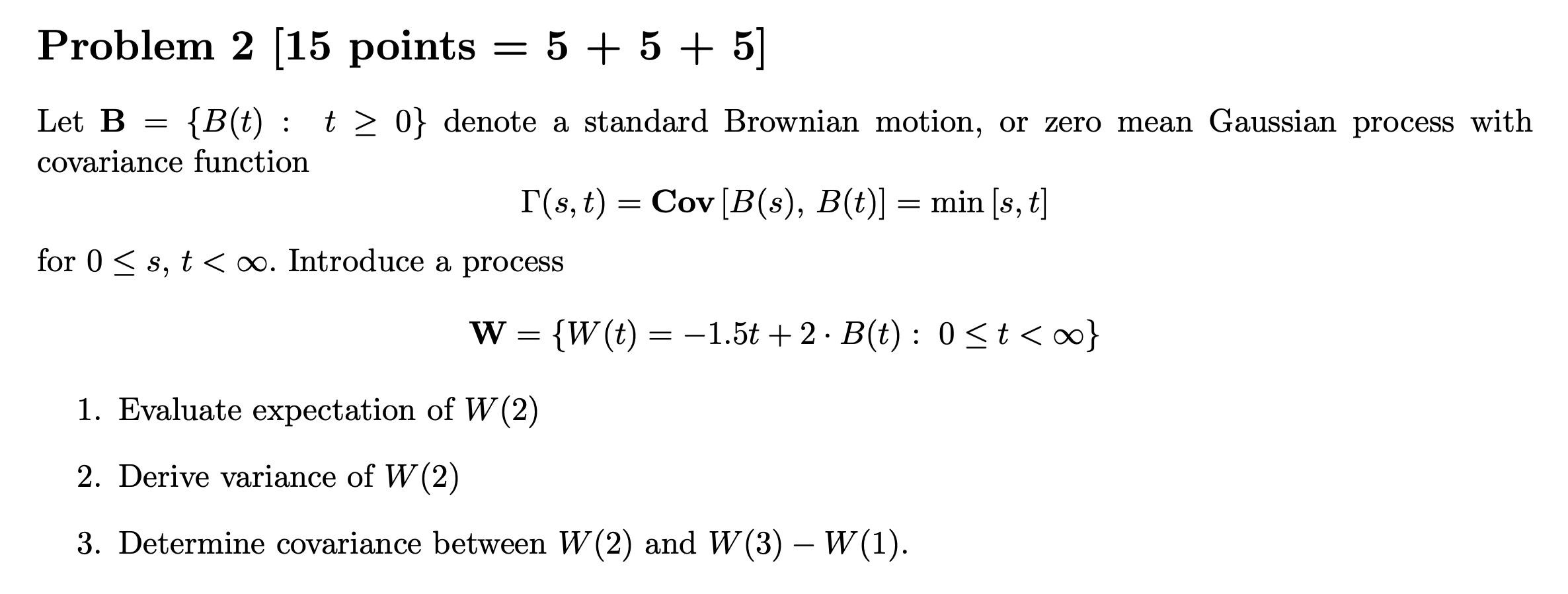

Problem 2 [15 points = 5 + 5 + 5] Let B = {B(t) : t > 0} denote a standard Brownian motion, or zero mean Gaussian process with covariance function T(s, t) = Cov [B(s), B(t)] = min [s, t] for 0 _ s, t

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock