Question: Need help with question 10 to 13! Question A (24 points) Suppose that the monthly log price of an asset, pt, follows a random walk

Need help with question 10 to 13!

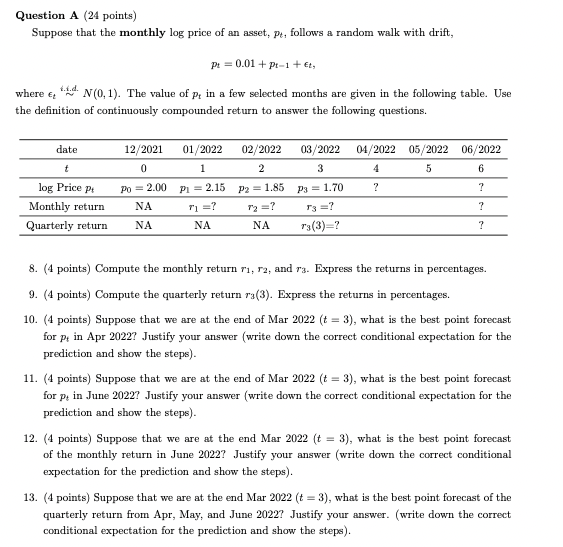

Question A (24 points) Suppose that the monthly log price of an asset, pt, follows a random walk with drift, pt=0.01+pt1+t, where ti.i.d.N(0,1). The value of pt in a few selected months are given in the following table. Use the definition of continuously compounded return to answer the following questions. 8. (4 points) Compute the monthly return r1,r2, and r3. Express the returns in percentages. 9. (4 points) Compute the quarterly return r3(3). Express the returns in percentages. 10. (4 points) Suppose that we are at the end of Mar 2022(t=3), what is the best point forecast for pt in Apr 2022? Justify your answer (write down the correct conditional expectation for the prediction and show the steps). 11. (4 points) Suppose that we are at the end of Mar 2022(t=3), what is the best point forecast for pt in June 2022? Justify your answer (write down the correct conditional expectation for the prediction and show the steps). 12. (4 points) Suppose that we are at the end Mar 2022(t=3), what is the best point forecast of the monthly return in June 2022? Justify your answer (write down the correct conditional expectation for the prediction and show the steps). 13. (4 points) Suppose that we are at the end Mar 2022(t=3), what is the best point forecast of the quarterly return from Apr, May, and June 2022? Justify your answer. (write down the correct conditional expectation for the prediction and show the steps). Question A (24 points) Suppose that the monthly log price of an asset, pt, follows a random walk with drift, pt=0.01+pt1+t, where ti.i.d.N(0,1). The value of pt in a few selected months are given in the following table. Use the definition of continuously compounded return to answer the following questions. 8. (4 points) Compute the monthly return r1,r2, and r3. Express the returns in percentages. 9. (4 points) Compute the quarterly return r3(3). Express the returns in percentages. 10. (4 points) Suppose that we are at the end of Mar 2022(t=3), what is the best point forecast for pt in Apr 2022? Justify your answer (write down the correct conditional expectation for the prediction and show the steps). 11. (4 points) Suppose that we are at the end of Mar 2022(t=3), what is the best point forecast for pt in June 2022? Justify your answer (write down the correct conditional expectation for the prediction and show the steps). 12. (4 points) Suppose that we are at the end Mar 2022(t=3), what is the best point forecast of the monthly return in June 2022? Justify your answer (write down the correct conditional expectation for the prediction and show the steps). 13. (4 points) Suppose that we are at the end Mar 2022(t=3), what is the best point forecast of the quarterly return from Apr, May, and June 2022? Justify your answer. (write down the correct conditional expectation for the prediction and show the steps)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts