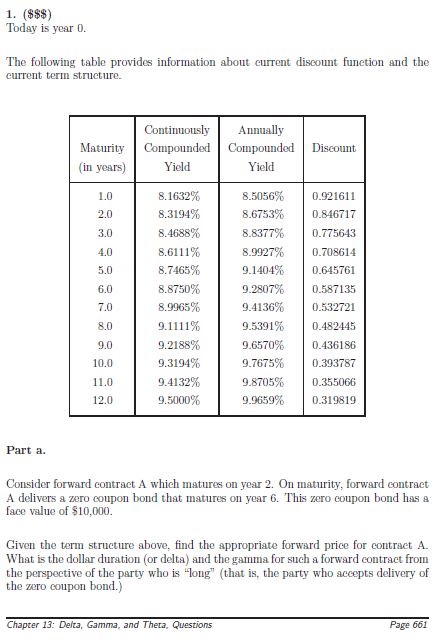

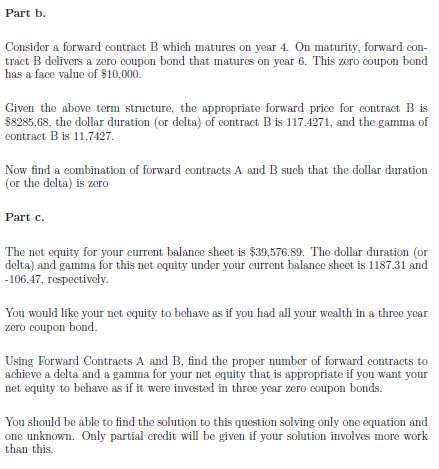

Question: Need help with Question 13 (a,b,c) 1. ($$$) Today is year 0. The following table provides information about current discount function and the current term

Need help with Question 13 (a,b,c)

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock