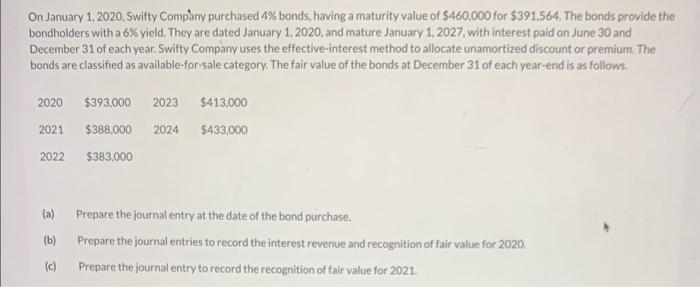

Question: need help with the empty boxes On January 1, 2020, Swifty Company purchased 4% bonds, having a maturity value of $460,000 for $391,564. The bonds

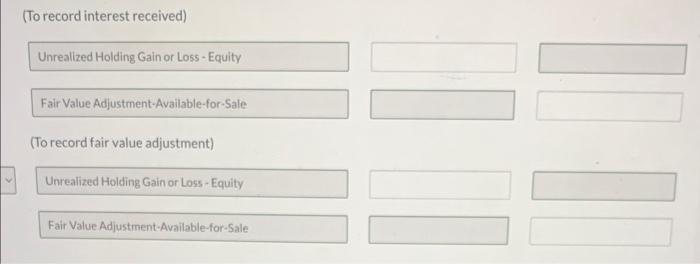

On January 1, 2020, Swifty Company purchased 4% bonds, having a maturity value of $460,000 for $391,564. The bonds provide the bondholders with a 6% yield. They are dated January 1, 2020, and mature January 1, 2027, with interest paid on June 30 and December 31 of each year. Swifty Company uses the effective-interest method to allocate unamortized discount or premium. The bonds are classified as available-for-sale category. The fair value of the bonds at December 31 of each year-end is as follows. (a) Prepare the journal entry at the date of the bond purchase. (b) Prepare the journal entries to record the interest revenue and recognition of fair value for 2020. (c) Prepare the journal entry to record the recognition of fair value for 2021. (To record interest received) Unrealized Holding Gain or Loss - Equity Fair Value Adjustment-Available-for-Sale (To record fair value adjustment) Unrealized Holding Gain or Loss - Equity Fair Value Adjustment-Available-for-Sale

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts