Question: need help with these please nope it all the inf there ok get those wrong Pop Corporation acquired 70 percent of Soda Company's voting common

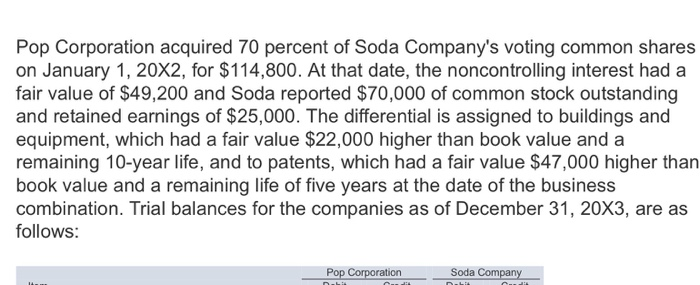

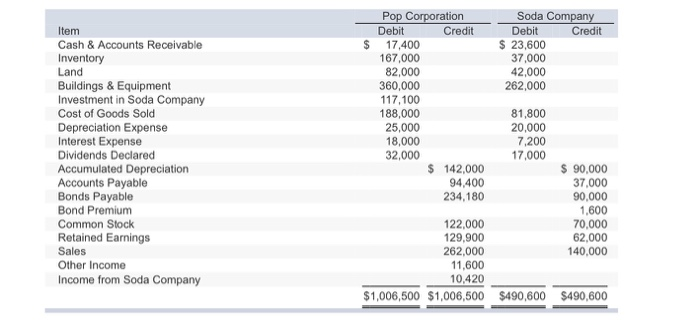

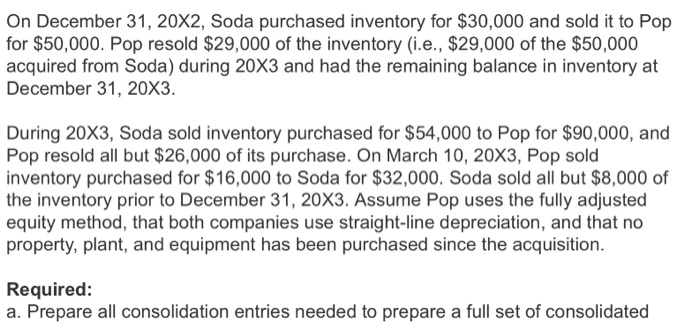

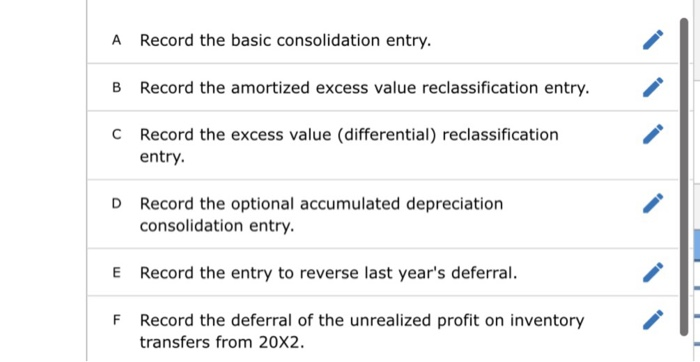

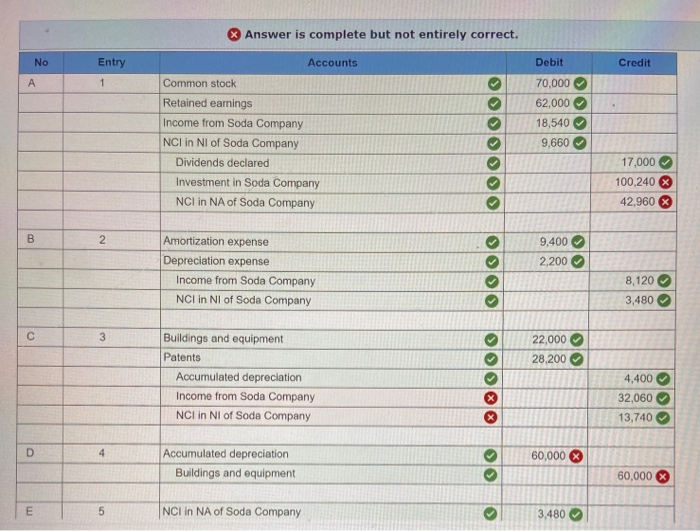

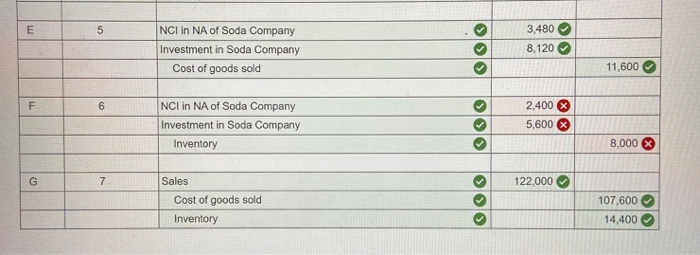

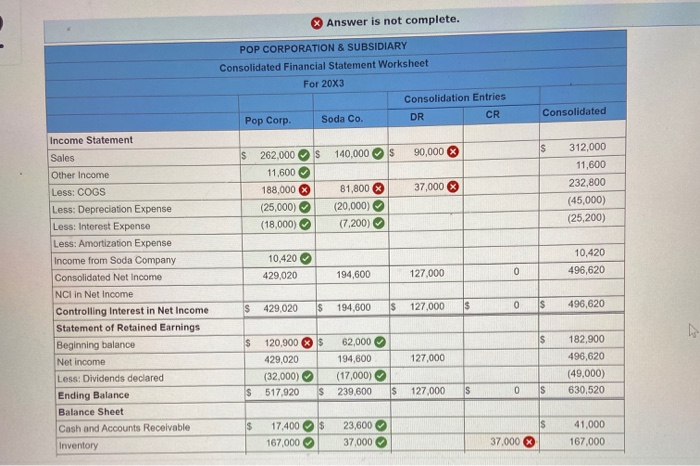

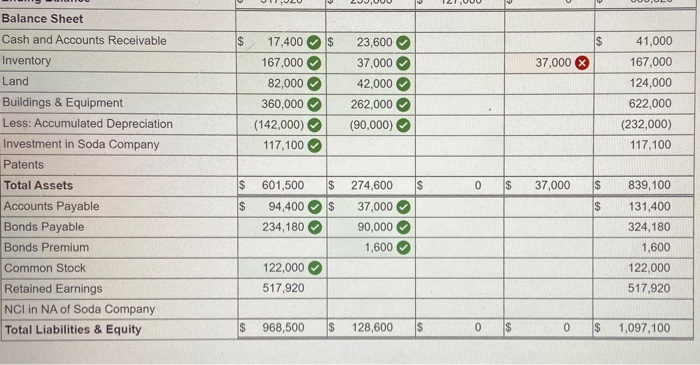

Pop Corporation acquired 70 percent of Soda Company's voting common shares on January 1, 20X2, for $114,800. At that date, the noncontrolling interest had a fair value of $49,200 and Soda reported $70,000 of common stock outstanding and retained earnings of $25,000. The differential is assigned to buildings and equipment, which had a fair value $22,000 higher than book value and a remaining 10-year life, and to patents, which had a fair value $47,000 higher than book value and a remaining life of five years at the date of the business combination. Trial balances for the companies as of December 31, 20X3, are as follows: Pop Corporation Soda Company RELI $ Soda Company Debit Credit $ 23,600 37,000 42,000 262,000 Item Cash & Accounts Receivable Inventory Land Buildings & Equipment Investment in Soda Company Cost of Goods Sold Depreciation Expense Interest Expense Dividends Declared Accumulated Depreciation Accounts Payable Bonds Payable Bond Premium Common Stock Retained Earnings Sales Other Income Income from Soda Company Pop Corporation Debit Credit 17,400 167.000 82,000 360,000 117,100 188,000 25,000 18,000 32,000 $ 142,000 94,400 234,180 81,800 20,000 7,200 17,000 $ 90,000 37,000 90,000 1,600 70,000 62,000 140,000 122,000 129,900 262,000 11,600 10,420 $1,006,500 $1,006,500 $490,600 $490,600 On December 31, 20X2, Soda purchased inventory for $30,000 and sold it to Pop for $50,000. Pop resold $29,000 of the inventory (i.e., $29,000 of the $50,000 acquired from Soda) during 20X3 and had the remaining balance in inventory at December 31, 20X3. During 20X3, Soda sold inventory purchased for $54,000 to Pop for $90,000, and Pop resold all but $26,000 of its purchase. On March 10, 20X3, Pop sold inventory purchased for $16,000 to Soda for $32,000. Soda sold all but $8,000 of the inventory prior to December 31, 20X3. Assume Pop uses the fully adjusted equity method, that both companies use straight-line depreciation, and that no property, plant, and equipment has been purchased since the acquisition. Required: a. Prepare all consolidation entries needed to prepare a full set of consolidated A Record the basic consolidation entry. B Record the amortized excess value reclassification entry. C Record the excess value (differential) reclassification entry. D Record the optional accumulated depreciation consolidation entry. E Record the entry to reverse last year's deferral. F Record the deferral of the unrealized profit on inventory transfers from 20x2. Answer is complete but not entirely correct. Entry Credit No Accounts Common stock Retained earnings Income from Soda Company NCI in Nl of Soda Company Dividends declared Investment in Soda Company NCI in NA of Soda Company Debit 70,000 62,000 18,540 9,660 17,000 100,240 % 42,960 x 9,400 2,200 Amortization expense Depreciation expense Income from Soda Company NCI in NI of Soda Company 000 0000 0000 0000000 8,120 3,480 Buildings and equipment Patents Accumulated depreciation Income from Soda Company 22,000 28,200 4,400 32,060 13,740 NCI in Nl of Soda Company Accumulated depreciation Buildings and equipment 60,000 60,000 X NCI in NA of Soda Company 3.480 NCI IN NA of Soda Company Investment in Soda Company Cost of goods sold 3,480 8,120 11,600 NCI in NA of Soda Company Investment in Soda Company Inventory 2,400 X 5,600 % 8,000 $ 122,000 Sales Cost of goods sold 107,600 14,400 Inventory * Answer is not complete. POP CORPORATION & SUBSIDIARY Consolidated Financial Statement Worksheet For 20X3 Consolidation Entries Pop Corp. Soda Co. DR CR Consolidated $ 140,000 $ 90,000 262,000 11,600 188,000 (25,000) (18,000) 37,000 81,800 (20,000) (7,200) 312,000 11,600 232,800 (45,000) (25,200) Income Statement Sales Other Income Less: COGS Less: Depreciation Expense Less: Interest Expense Less: Amortization Expense Income from Soda Company Consolidated Net Income NCI in Net Income Controlling Interest in Net Income Statement of Retained Earnings Beginning balance 10,420 429,020 10,420 496,620 194,600 127.000 429.020 $ 194,600 $ 127,000 496,620 Net income 120,900 $ 429,020 (32,000) 517.920 $ 127,000 62,000 194.800 (17,000) 239,600 182,900 496.620 (49,000) 630,520 $ 127,000 0 $ Less: Dividends declared Ending Balance Balance Sheet Cash and Accounts Receivable Inventory $ 17,400 167,000 23,600 37.000 37.000 $ 41,000 167.000 200.000 21.UUU $ 37,000 17,400 167,000 82,000 360,000 (142,000) 117,100 23,600 37,000 42,000 262,000 (90,000) 41,000 167,000 124,000 622,000 (232,000) 117,100 Balance Sheet Cash and Accounts Receivable Inventory Land Buildings & Equipment Less: Accumulated Depreciation Investment in Soda Company Patents Total Assets Accounts Payable Bonds Payable Bonds Premium Common Stock Retained Earnings NCI in NA of Soda Company Total Liabilities & Equity $ 0 $ 37,000 $ $ $ 601,500 94,400 234,180 $ $ 274,600 37,000 90,000 1,600 839,100 131,400 324,180 1,600 122,000 517,920 122,000 517,920 $ 968,500 $ 128,600S 0 S 0 $ 1,097,100

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts