Question: need help with this question asap . i attached some information that may be helpful. Consider the model constituted by three stocks, and there are

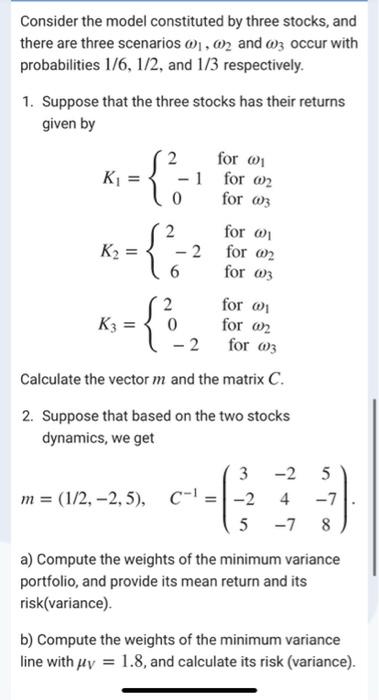

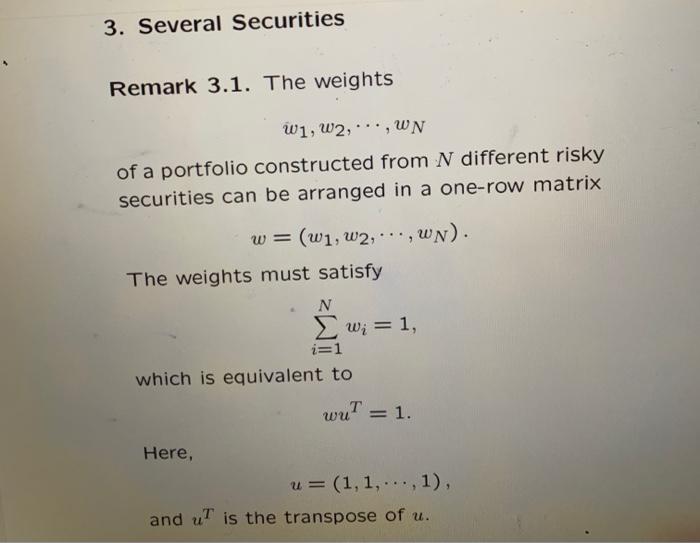

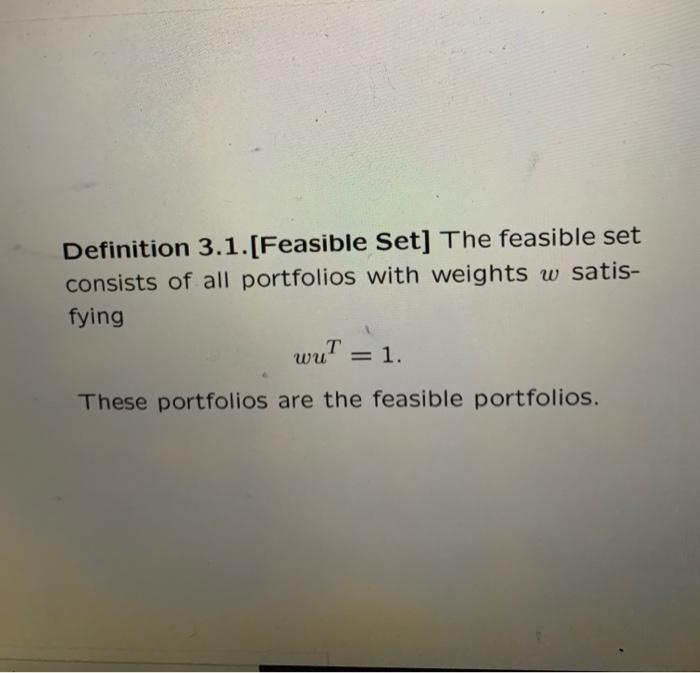

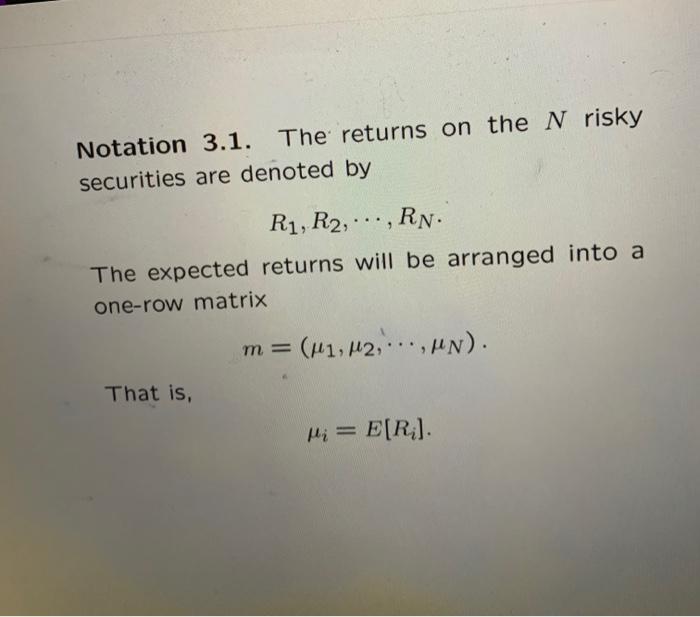

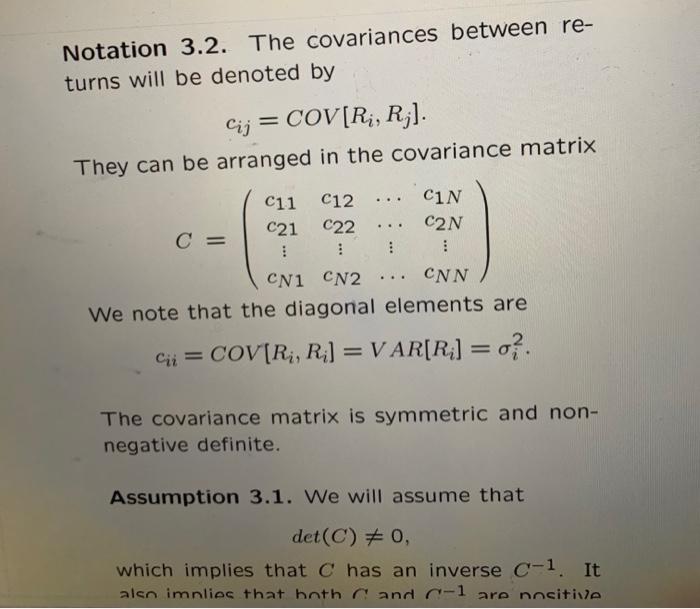

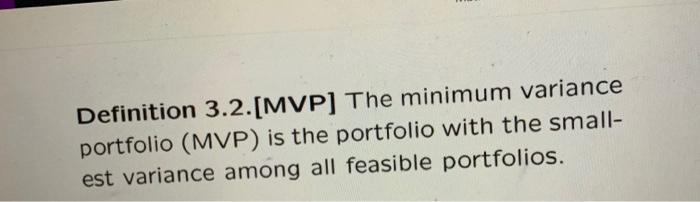

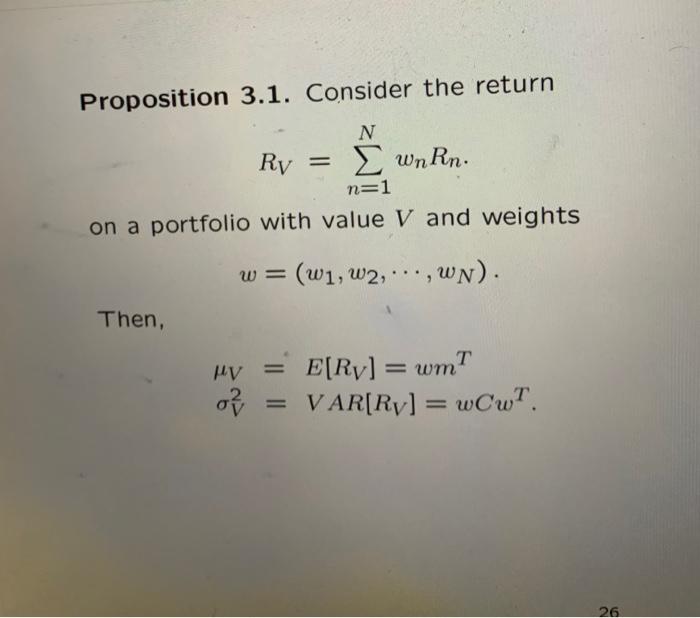

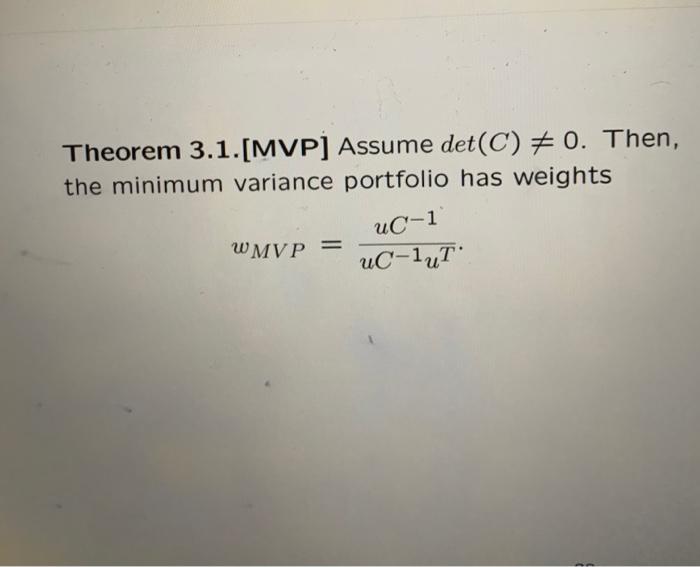

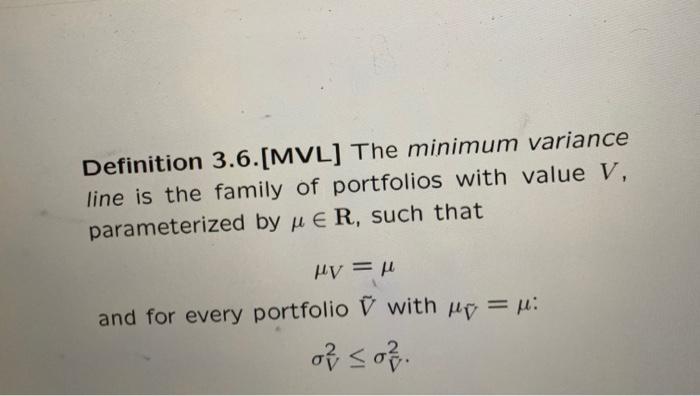

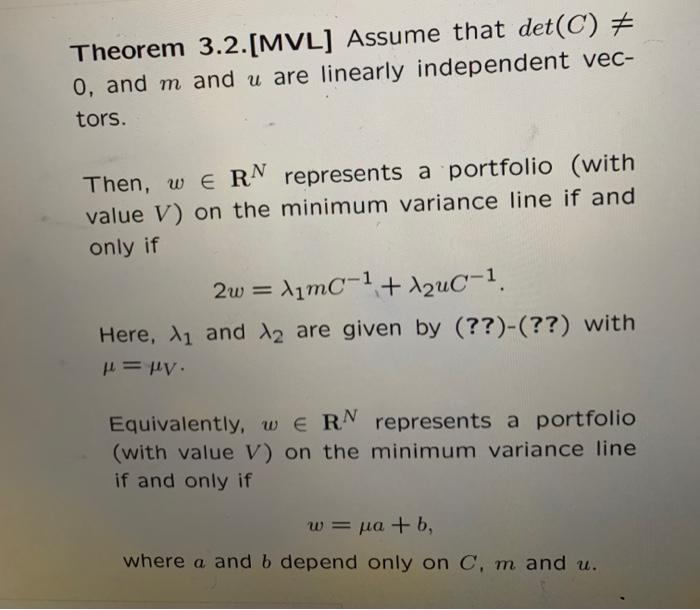

Consider the model constituted by three stocks, and there are three scenarios 0,02 and 03 occur with probabilities 1/6, 1/2, and 1/3 respectively. 1. Suppose that the three stocks has their returns given by for a K = 1 for 2 0 for 63 K2 = = 2 -2 6 for 1 for 02 for 03 2 for K3 = 0 for an 2 for 63 Calculate the vector m and the matrix C. { 2. Suppose that based on the two stocks dynamics, we get 4 -7 3 -2 5 m = (1/2, -2,5), c-' = -2 4 -7 5 8 a) Compute the weights of the minimum variance portfolio, and provide its mean return and its risk(variance) b) Compute the weights of the minimum variance line with My = 1.8, and calculate its risk (variance). 3. Several Securities Remark 3.1. The weights W1, W2, ...,WN of a portfolio constructed from N different risky securities can be arranged in a one-row matrix w = (w1, W2, ..., WN). The weights must satisfy N w; = 1, i=1 which is equivalent to wut = 1. Here, u= (1,1,...,1), and uT is the transpose of u. Definition 3.1.[Feasible Set] The feasible set consists of all portfolios with weights w satis- fying wut = 1. These portfolios are the feasible portfolios. Notation 3.1. The returns on the N risky securities are denoted by R1, R2, ..., Rn. The expected returns will be arranged into a one-row matrix m = (M1, M2,...,un). That is, Hi = E[R] Notation 3.2. The covariances between re- turns will be denoted by Cij = COV[Ri, R;]. They can be arranged in the covariance matrix C11 C12 CIN C21 C22 C2N C = : : CN1 CN2 CNN We note that the diagonal elements are COV[Ri, R;] = VAR[R;] = 0?. The covariance matrix is symmetric and non- negative definite. Assumption 3.1. We will assume that det(C) = 0, which implies that has an inverse C-1. It also imnlies that both cand c-l are nositive Definition 3.2.[MVP] The minimum variance portfolio (MVP) is the portfolio with the small- est variance among all feasible portfolios. Proposition 3.1. Consider the return Ry = N wnRn. n=1 on a portfolio with value V and weights w = (w1, W2, ...,wN). Then, 03 E[Ry] =wmt VAR[Ry] =wCwT. 26 Theorem 3.1.[MVP) Assume det(C) = 0. Then, the minimum variance portfolio has weights UC-1 WMVP = UC-14T Definition 3.6.[MVL) The minimum variance line is the family of portfolios with value V, parameterized by u ER, such that HV = and for every portfolio with hi =u: of so Theorem 3.2.[MVL] Assume that det(C) E 0, and m and u are linearly independent vec- tors. Then, we RN represents a portfolio (with value V) on the minimum variance line if and only if 2w = limc-1 + 12uc-1. Here, 11 and 12 are given by (??)-(??) with | = ly, Equivalently, we RN represents a portfolio (with value V) on the minimum variance line V) if and only if w=pa +b, where a and b depend only on C, m and u. Consider the model constituted by three stocks, and there are three scenarios 0,02 and 03 occur with probabilities 1/6, 1/2, and 1/3 respectively. 1. Suppose that the three stocks has their returns given by for a K = 1 for 2 0 for 63 K2 = = 2 -2 6 for 1 for 02 for 03 2 for K3 = 0 for an 2 for 63 Calculate the vector m and the matrix C. { 2. Suppose that based on the two stocks dynamics, we get 4 -7 3 -2 5 m = (1/2, -2,5), c-' = -2 4 -7 5 8 a) Compute the weights of the minimum variance portfolio, and provide its mean return and its risk(variance) b) Compute the weights of the minimum variance line with My = 1.8, and calculate its risk (variance). 3. Several Securities Remark 3.1. The weights W1, W2, ...,WN of a portfolio constructed from N different risky securities can be arranged in a one-row matrix w = (w1, W2, ..., WN). The weights must satisfy N w; = 1, i=1 which is equivalent to wut = 1. Here, u= (1,1,...,1), and uT is the transpose of u. Definition 3.1.[Feasible Set] The feasible set consists of all portfolios with weights w satis- fying wut = 1. These portfolios are the feasible portfolios. Notation 3.1. The returns on the N risky securities are denoted by R1, R2, ..., Rn. The expected returns will be arranged into a one-row matrix m = (M1, M2,...,un). That is, Hi = E[R] Notation 3.2. The covariances between re- turns will be denoted by Cij = COV[Ri, R;]. They can be arranged in the covariance matrix C11 C12 CIN C21 C22 C2N C = : : CN1 CN2 CNN We note that the diagonal elements are COV[Ri, R;] = VAR[R;] = 0?. The covariance matrix is symmetric and non- negative definite. Assumption 3.1. We will assume that det(C) = 0, which implies that has an inverse C-1. It also imnlies that both cand c-l are nositive Definition 3.2.[MVP] The minimum variance portfolio (MVP) is the portfolio with the small- est variance among all feasible portfolios. Proposition 3.1. Consider the return Ry = N wnRn. n=1 on a portfolio with value V and weights w = (w1, W2, ...,wN). Then, 03 E[Ry] =wmt VAR[Ry] =wCwT. 26 Theorem 3.1.[MVP) Assume det(C) = 0. Then, the minimum variance portfolio has weights UC-1 WMVP = UC-14T Definition 3.6.[MVL) The minimum variance line is the family of portfolios with value V, parameterized by u ER, such that HV = and for every portfolio with hi =u: of so Theorem 3.2.[MVL] Assume that det(C) E 0, and m and u are linearly independent vec- tors. Then, we RN represents a portfolio (with value V) on the minimum variance line if and only if 2w = limc-1 + 12uc-1. Here, 11 and 12 are given by (??)-(??) with | = ly, Equivalently, we RN represents a portfolio (with value V) on the minimum variance line V) if and only if w=pa +b, where a and b depend only on C, m and u

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts