Question: Need help with this question Suppose that a portfolio consists of two assets and the total change of portfolio's value, denoted by X, can be

Need help with this question

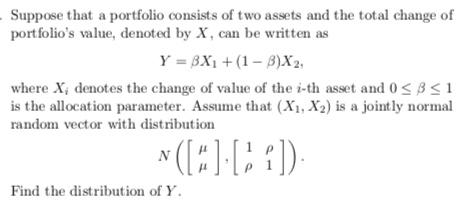

Suppose that a portfolio consists of two assets and the total change of portfolio's value, denoted by X, can be written as Y=X1+(1)X2, where Xi denotes the change of value of the i-th asset and 01 is the allocation parameter. Assume that (X1,X2) is a jointly normal random vector with distribution N([],[11]). Find the distribution of Y

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock