Question: Need helpHow to calculate this problem, please show the steps, thank you! Question 4 (Total 11 Marks) The following table shows the prices of several

Need helpHow to calculate this problem, please show the steps, thank you!

Need helpHow to calculate this problem, please show the steps, thank you!

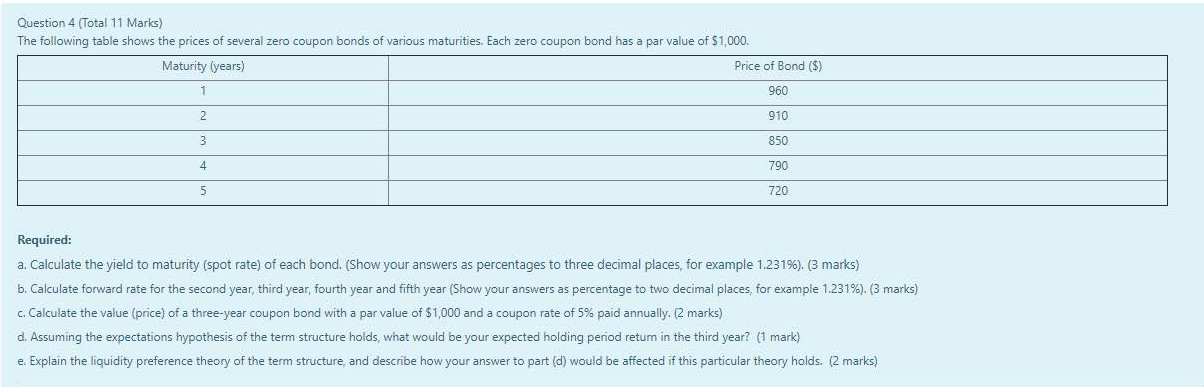

Question 4 (Total 11 Marks) The following table shows the prices of several zero coupon bonds of various maturities. Each zero coupon bond has a par value of $1,000. Maturity (years) Price of Bond ($) 1 960 2 910 3 850 4 790 5 720 Required: a. Calculate the yield to maturity (spot rate) of each bond. (Show your answers as percentages to three decimal places, for example 1.231%). (3 marks) b. Calculate forward rate for the second year, third year, fourth year and fifth year (Show your answers as percentage to two decimal places for example 1.231%). (3 marks) c. Calculate the value (price) of a three-year coupon bond with a par value of $1,000 and a coupon rate of 5% paid annually. (2 marks) d. Assuming the expectations hypothesis of the term structure holds, what would be your expected holding period retum in the third year? (1 mark) e. Explain the liquidity preference theory of the term structure and describe how your answer to part (d) would be affected if this particular theory holds. (2 marks) Question 4 (Total 11 Marks) The following table shows the prices of several zero coupon bonds of various maturities. Each zero coupon bond has a par value of $1,000. Maturity (years) Price of Bond ($) 1 960 2 910 3 850 4 790 5 720 Required: a. Calculate the yield to maturity (spot rate) of each bond. (Show your answers as percentages to three decimal places, for example 1.231%). (3 marks) b. Calculate forward rate for the second year, third year, fourth year and fifth year (Show your answers as percentage to two decimal places for example 1.231%). (3 marks) c. Calculate the value (price) of a three-year coupon bond with a par value of $1,000 and a coupon rate of 5% paid annually. (2 marks) d. Assuming the expectations hypothesis of the term structure holds, what would be your expected holding period retum in the third year? (1 mark) e. Explain the liquidity preference theory of the term structure and describe how your answer to part (d) would be affected if this particular theory holds. (2 marks)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts