Question: NEED HELP!!!!!.....Please read the instructions very carefully pleae. Mastery Problem: Statement of Cash Flows Championship Boxing, Inc. Championship Boxing, Inc. is a small manufacturer of

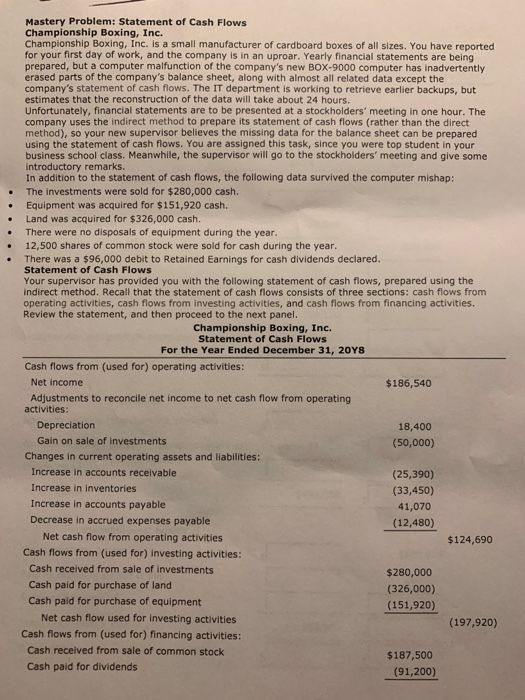

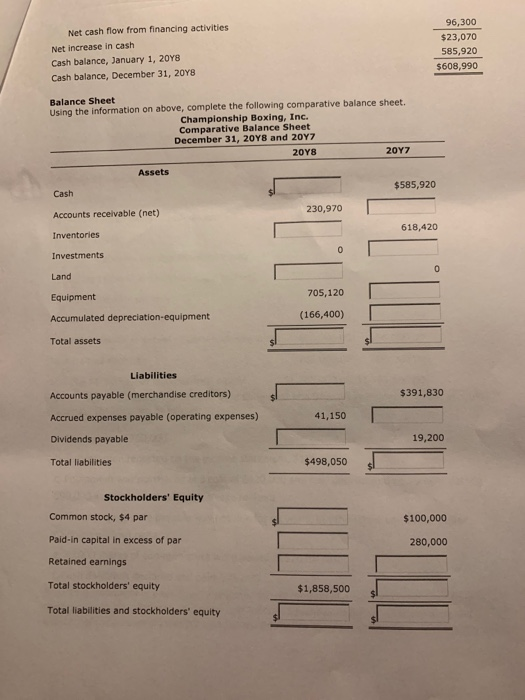

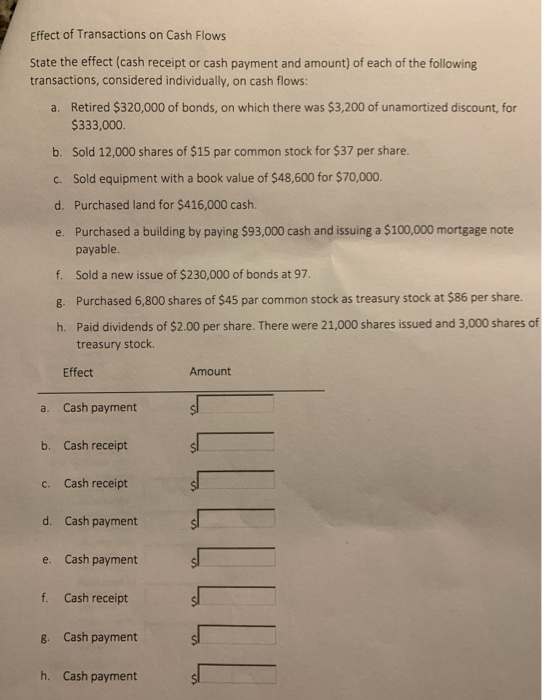

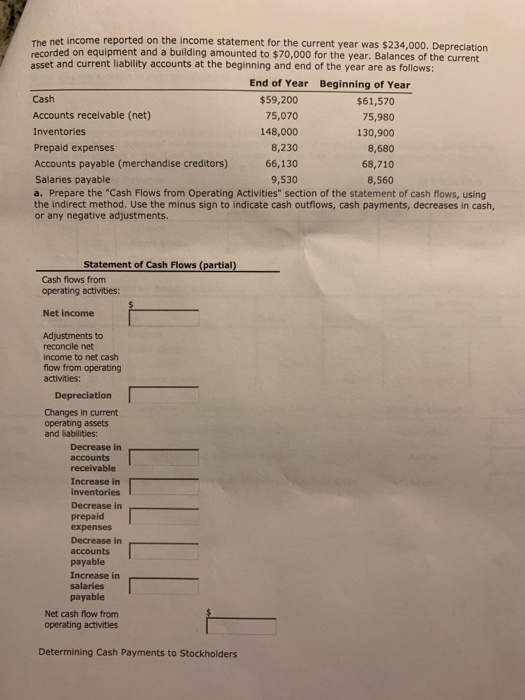

Mastery Problem: Statement of Cash Flows Championship Boxing, Inc. Championship Boxing, Inc. is a small manufacturer of cardboard boxes of all sizes. You have reported for your first day of work, and the company is in an uproar. Yearly financial statements are being prepared, but a computer malfunction of the company's new BOX-9000 computer has inadvertently erased parts of the company's balance sheet, along with almost all related data except the company's statement of cash flows. The IT department is working to retrieve earlier backups, but estimates that the reconstruction of the data will take about 24 hours. Unfortunately, financial statements are to be presented at a stockholders' meeting in one hour. The company uses the indirect method to prepare its statement of cash flows (rather than the direct method), so your new supervisor believes the missing data for the balance sheet can be prepared using the statement of cash flows. You are assigned this task, since you were top student in your business school class. Meanwhile, the supervisor will go to the stockholders' meeting and give some introductory remarks. In addition to the statement of cash flows, the following data survived the computer mishap: The investments were sold for $280,000 cash. Equipment was acquired for $151,920 cash. Land was acquired for $326,000 cash. There were no disposals of equipment during the year. 12,500 shares of common stock were sold for cash during the year. There was a $96,000 debit to Retained Earnings for cash dividends declared. Statement of Cash Flows Your supervisor has provided you with the following statement of cash flows, prepared using the indirect method. Recall that the statement of cash flows consists of three sections: cash flows from operating activities, cash flows from investing activities, and cash flows from financing activities. Review the statement, and then proceed to the next panel. Championship Boxing, Inc. Statement of Cash Flows For the Year Ended December 31, 20Y8 Cash flows from (used for) operating activities: Net income $186,540 Adjustments to reconcile net income to net cash flow from operating activities: Depreciation 18,400 Gain on sale of investments (50,000) Changes in current operating assets and liabilities: Increase in accounts receivable (25,390) Increase in inventories (33,450) Increase in accounts payable 41,070 Decrease in accrued expenses payable (12,480) Net cash flow from operating activities $124,690 Cash flows from (used for) investing activities: Cash received from sale of investments $280,000 Cash paid for purchase of land (326,000) Cash pald for purchase of equipment (151,920) Net cash flow used for investing activities Cash flows from (used for) financing activities: (197,920) Cash received from sale of common stock $187,500 Cash paid for dividends (91,200) 96,300 Net cash flow from financing activities $23,070 Net increase in cash 585,920 Cash balance, January 1, 20Y8 $608,990 Cash balance, December 31, 20Y8 Using the information on above, complete the following comparative balance sheet. Championship Boxing, Inc. Comparative Balance Sheet December 31, 20Y8 and 20Y7 Balance Sheet 20Y7 208 Assets $585,920 Cash 230,970 Accounts receivable (net) 618,420 Inventories Investments Land 705,120 Equipment (166,400) Accumulated depreciation-equipment Total assets Liabilities $391,830 Accounts payable (merchandise creditors) 41,150 Accrued expenses payable (operating expenses) 19,200 Dividends payable $498,050 Total liabilities Stockholders' Equity Common stock, $4 par $100,000 Paid-in capital in excess of par 280,000 Retained earnings Total stockholders' equity $1,858,500 Total liabilities and stockholders' equity Effect of Transactions on Cash Flows State the effect (cash receipt or cash payment and amount) of each of the following transactions, considered individually, on cash flows: Retired $320,000 of bonds, on which there was $3,200 of unamortized discount, for $333,000. a. b. Sold 12,000 shares of $15 par common stock for $37 per share. c. Sold equipment with a book value of $48,600 for $70,000. d. Purchased land for $416,000 cash. Purchased a building by paying $93,000 cash and issuing a $100,000 mortgage note payable. e. f. Sold a new issue of $230,000 of bonds at 97. g. Purchased 6,800 shares of $45 par common stock as treasury stock at $86 per share. Paid dividends of $2.00 per share. There were 21,000 shares issued and 3,000 shares of h. treasury stock. Effect Amount Cash payment a. b. Cash receipt Cash receipt C. d. Cash payment Cash payment e. Cash receipt f. Cash payment g. h. Cash payment LLLLLLL The net income reported on the income statement for the current year was $234,000. Depreciation recorded on equipment and a building amounted to $70,000 for the year. Balances of the current asset and current liability accounts at the beginning and end of the year are as follows: End of Year Beginning of Year Cash $59,200 $61,570 Accounts receivable (net) 75,070 75,980 Inventories 148,000 130,900 8,230 Prepaid expenses 8,680 Accounts payable (merchandise creditors) 66,130 68,710 Salaries payable a. Prepare the "Cash Flows from Operating Activities" section of the statement of cash flows, using the indirect method. Use the minus sign to indicate cash outflows, cash payments, decreases in cash, or any negative adjustments. 9,530 8,560 Statement of Cash Flows (partial) Cash flows from operating activities: Net income Adjustments to reconcile net income to net cash flow from operating activities: Depreciation Changes in current operating assets and liabilities: Decrease in accounts receivable Increase in inventories Decrease in prepaid expenses Decrease in accounts payable Increase in salaries payable Net cash flow from operating activities Determining Cash Payments to Stockholders LLLL The board of directors declared cash dividends totaling $150,300 during the current year. The comparative balance sheet indicates dividends payable of $40,600 at the beginning of the year and $36,500 at the end of the year. What was the amount of cash payments to stockholders during the year

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts