Question: need some help with Case Study: Consolidated Balance Sheet At Date Of Purchase This case study will provide a thorough illustration as to the concepts

need some help with

need some help with

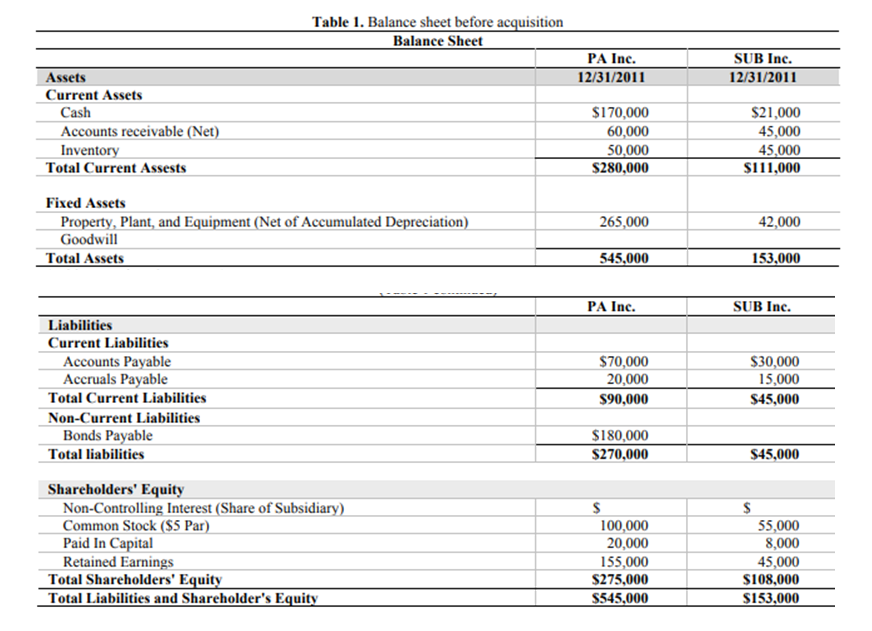

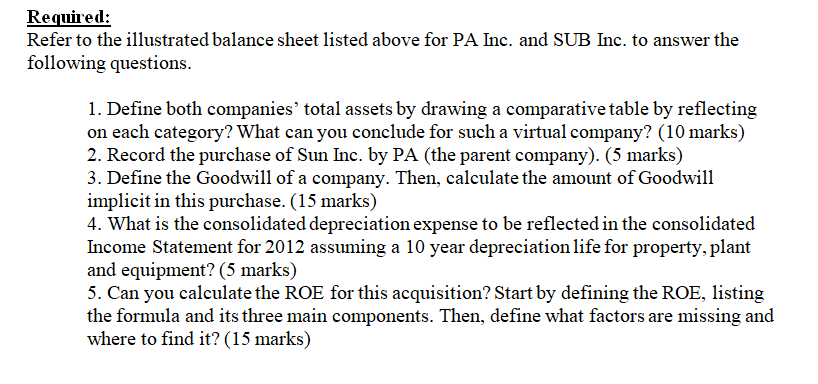

Case Study: Consolidated Balance Sheet At Date Of Purchase This case study will provide a thorough illustration as to the concepts of consolidations on the date of acquisition. On this date, an ensuing Consolidated Balance Sheet is created, whereby the acquiring and the acquired companies are combined as a single entity. Interestingly, there are options as to the consolidation basis which may be utilized, which also includes the push- down method of accounting. The pushdown method was illustrated in a previous case study and it is highly recommended that the reader resort to this, which can be found in Harris & Dilling (2015). An overview of this critical topic will be discussed, followed by a comprehensive illustration demonstrating the results of consolidated results as of the date of acquisition. Note that the resulting Balance Sheet will be the same with the push-down accounting result. This case study is recommended as a group project for an Advanced Accounting course as well as for a graduate Financial Statement Analysis class. Facts: On December 31, 2011, PA. Inc. purchased 95 percent of Sub. Inc. for $120,000 cash. The Balance Sheet of each corporation just prior to the acquisition is presented below. Additionally, book value and fair value for all of Sub's assets and liabilities are equal, with the exception of Property, Plant and Equipment, whose fair value is $47,000. Table 1. Balance sheet before acquisition Balance Sheet PA Inc. 12/31/2011 SUB Inc. 12/31/2011 Assets Current Assets Cash Accounts receivable (Net) Inventory Total Current Assests $170,000 60,000 50,000 $280,000 $21,000 45,000 45,000 $111,000 265,000 42,000 Fixed Assets Property, Plant, and Equipment (Net of Accumulated Depreciation) Goodwill Total Assets 545,000 153,000 PA Inc. SUB Inc. Liabilities Current Liabilities Accounts Payable Accruals Payable Total Current Liabilities Non-Current Liabilities Bonds Payable Total liabilities $70,000 20,000 $90,000 $30,000 15,000 $45,000 $180,000 $270,000 $45,000 Shareholders' Equity Non-Controlling Interest (Share of Subsidiary) Common Stock ($5 Par) Paid In Capital Retained Earnings Total Shareholders' Equity Total Liabilities and Shareholder's Equity $ 100,000 20,000 155,000 $275,000 $545,000 $ 55,000 8,000 45,000 $108,000 $153,000 Required: Refer to the illustrated balance sheet listed above for PA Inc. and SUB Inc. to answer the following questions. 1. Define both companies' total assets by drawing a comparative table by reflecting on each category? What can you conclude for such a virtual company? (10 marks) 2. Record the purchase of Sun Inc. by PA (the parent company). (5 marks) 3. Define the Goodwill of a company. Then, calculate the amount of Goodwill implicit in this purchase. (15 marks) 4. What is the consolidated depreciation expense to be reflected in the consolidated Income Statement for 2012 assuming a 10 year depreciation life for property, plant and equipment? (5 marks) 5. Can you calculate the ROE for this acquisition? Start by defining the ROE, listing the formula and its three main components. Then, define what factors are missing and where to find it? (15 marks) Case Study: Consolidated Balance Sheet At Date Of Purchase This case study will provide a thorough illustration as to the concepts of consolidations on the date of acquisition. On this date, an ensuing Consolidated Balance Sheet is created, whereby the acquiring and the acquired companies are combined as a single entity. Interestingly, there are options as to the consolidation basis which may be utilized, which also includes the push- down method of accounting. The pushdown method was illustrated in a previous case study and it is highly recommended that the reader resort to this, which can be found in Harris & Dilling (2015). An overview of this critical topic will be discussed, followed by a comprehensive illustration demonstrating the results of consolidated results as of the date of acquisition. Note that the resulting Balance Sheet will be the same with the push-down accounting result. This case study is recommended as a group project for an Advanced Accounting course as well as for a graduate Financial Statement Analysis class. Facts: On December 31, 2011, PA. Inc. purchased 95 percent of Sub. Inc. for $120,000 cash. The Balance Sheet of each corporation just prior to the acquisition is presented below. Additionally, book value and fair value for all of Sub's assets and liabilities are equal, with the exception of Property, Plant and Equipment, whose fair value is $47,000. Table 1. Balance sheet before acquisition Balance Sheet PA Inc. 12/31/2011 SUB Inc. 12/31/2011 Assets Current Assets Cash Accounts receivable (Net) Inventory Total Current Assests $170,000 60,000 50,000 $280,000 $21,000 45,000 45,000 $111,000 265,000 42,000 Fixed Assets Property, Plant, and Equipment (Net of Accumulated Depreciation) Goodwill Total Assets 545,000 153,000 PA Inc. SUB Inc. Liabilities Current Liabilities Accounts Payable Accruals Payable Total Current Liabilities Non-Current Liabilities Bonds Payable Total liabilities $70,000 20,000 $90,000 $30,000 15,000 $45,000 $180,000 $270,000 $45,000 Shareholders' Equity Non-Controlling Interest (Share of Subsidiary) Common Stock ($5 Par) Paid In Capital Retained Earnings Total Shareholders' Equity Total Liabilities and Shareholder's Equity $ 100,000 20,000 155,000 $275,000 $545,000 $ 55,000 8,000 45,000 $108,000 $153,000 Required: Refer to the illustrated balance sheet listed above for PA Inc. and SUB Inc. to answer the following questions. 1. Define both companies' total assets by drawing a comparative table by reflecting on each category? What can you conclude for such a virtual company? (10 marks) 2. Record the purchase of Sun Inc. by PA (the parent company). (5 marks) 3. Define the Goodwill of a company. Then, calculate the amount of Goodwill implicit in this purchase. (15 marks) 4. What is the consolidated depreciation expense to be reflected in the consolidated Income Statement for 2012 assuming a 10 year depreciation life for property, plant and equipment? (5 marks) 5. Can you calculate the ROE for this acquisition? Start by defining the ROE, listing the formula and its three main components. Then, define what factors are missing and where to find it? (15 marks)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts