Question: need to solve section B and C SECTION C On April 20x4 Runner Co acquired Bon of Jogger Co's equity shares when the retained ang

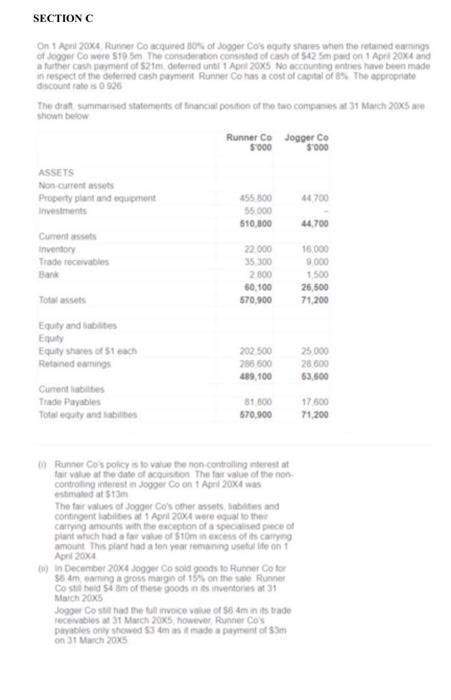

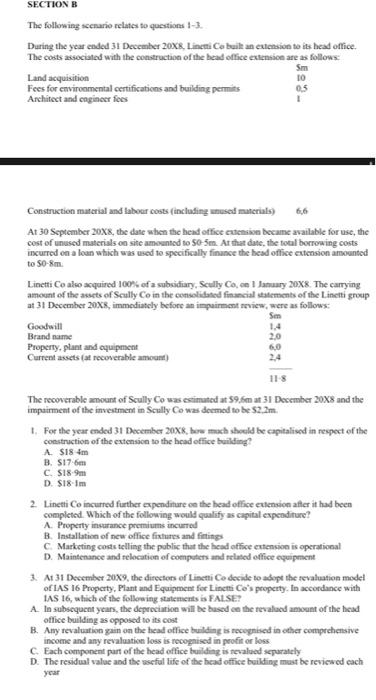

SECTION C On April 20x4 Runner Co acquired Bon of Jogger Co's equity shares when the retained ang of Jogger Co were 5195 The consideration consisted of cash of 542 Simpadon 1 or 20x4 and a further cash payment of 2m deferredunt 1 April 2005 No accountingentes have been made in respect of me deferred cash payment Runner Co has a cost of capital of 8 The propriate discount rates 926 The dealt samme statements of financial position of the two companies at 31 March 2015 shown below Runner Co Jogger Co 5000 S'000 44700 ASSETS Non-currentes Property plant and equipment Investments Current assets inventory Trade recevables Bank 155 800 55.000 510.000 44,700 22.000 35300 2.800 50.100 570.900 16.000 9000 1500 26,500 71.200 Total assets Equity and abilities Equity Equity shares of 51 each Retained earnings Current abilities Trade Payables Total cost and its 202500 286 600 489 100 25.000 28.500 53,600 31 800 570.900 17.500 71.200 Runner os policy is to value the non controlling interest fair value of the date of acquisition The far value of the non controlling interest in Jogger Co on 1 April 20X& was med at $13m The far values of Jogger Co's other assets and contingent les of 1 April 20x4 were equal to the Carrying amounts with the exception of a specialised piece of plant which had a fare of $10m in excess of its Carg amount This plant had a ton year romaning turli on April 20% In December 2004 Jogger Co sold goods to Runner Color $5 m caring a gross margin of 15% on the sale Runner Costed som of these goods in inventores at 31 March 20X5 Jogger Cost had the invice Value of $5 ministrade receivables at 31 Mach 2005however Runner Cos payable only showed 53 made a payment of on 31 March 2005 SECTION B The following scenario relates to questions !-3. During the year ended 31 December 20XB, Lineni Ce built an extension to its head office. The costs associated with the construction of the head office extension are as follows: Land acquisition Fees for environmental certifications and building permits 0.5 Architect and cogineer fees 1 Sm TO Construction material and labour costs (including unused materials) At 30 September 20X8, the date when the head office extension became available for use, the cost of unused materials on site amounted to 50-5m. At that date, the total borrowing costs incurred on a loan which was used to specifically finance the head office extension amounted to S0-8m Linetti Co also acquired 100% of a subsidiary, Scully Co, on January 20X8. The carrying amount of the assets of Scully Co in the consolidated financial statements of the Linetti group at 31 December 20x8, immediately before an impairment view, were as follows: Sm Goodwill Brand name 2.0 Property, plant and equipment 60 Current assets at recoverable amount 2,4 118 The recoverable amount of Scully Co was estimated at 59.fm at 31 December 20X8 and the impairment of the investment in Scally Co was deemed to be 52.2m For the year ended 31 December 20X6. bermach should be capitalised in respect of the construction of the extension to the head office building? A. $18 4m B. S17-6m C. $18-9m DS181m 2. Linetti Co incurred further expenditure on the head office extension after it had been completed. Which of the following would qualify as capital expenditure? A Property insurance premiums incurred B. Installation of new office fixtures and finting C Marketing coststelling the public that the head office extension is operational D. Maintenance and relocation of computers and related office equipment 3. At 31 December 20X9, the directors of Linetti o decide to adopt the evaluation model of IAS 16 Property. Piant and Equipment for Linea Co's property. In accordance with IAS 16, which of the following statements is FALSE? A. In subsequent years, the depreciation will be based on the evalued amount of the head office building as opposed to its cost B. Any revaluation gain on the head office building is recognised in other comprchesive income and any revaluation loss is recognised in profit or loss C. Each component part of the head office building is revalued separately D. The residual value and the seful life of the head office building must be reviewed cach year SECTION C On April 20x4 Runner Co acquired Bon of Jogger Co's equity shares when the retained ang of Jogger Co were 5195 The consideration consisted of cash of 542 Simpadon 1 or 20x4 and a further cash payment of 2m deferredunt 1 April 2005 No accountingentes have been made in respect of me deferred cash payment Runner Co has a cost of capital of 8 The propriate discount rates 926 The dealt samme statements of financial position of the two companies at 31 March 2015 shown below Runner Co Jogger Co 5000 S'000 44700 ASSETS Non-currentes Property plant and equipment Investments Current assets inventory Trade recevables Bank 155 800 55.000 510.000 44,700 22.000 35300 2.800 50.100 570.900 16.000 9000 1500 26,500 71.200 Total assets Equity and abilities Equity Equity shares of 51 each Retained earnings Current abilities Trade Payables Total cost and its 202500 286 600 489 100 25.000 28.500 53,600 31 800 570.900 17.500 71.200 Runner os policy is to value the non controlling interest fair value of the date of acquisition The far value of the non controlling interest in Jogger Co on 1 April 20X& was med at $13m The far values of Jogger Co's other assets and contingent les of 1 April 20x4 were equal to the Carrying amounts with the exception of a specialised piece of plant which had a fare of $10m in excess of its Carg amount This plant had a ton year romaning turli on April 20% In December 2004 Jogger Co sold goods to Runner Color $5 m caring a gross margin of 15% on the sale Runner Costed som of these goods in inventores at 31 March 20X5 Jogger Cost had the invice Value of $5 ministrade receivables at 31 Mach 2005however Runner Cos payable only showed 53 made a payment of on 31 March 2005 SECTION B The following scenario relates to questions !-3. During the year ended 31 December 20XB, Lineni Ce built an extension to its head office. The costs associated with the construction of the head office extension are as follows: Land acquisition Fees for environmental certifications and building permits 0.5 Architect and cogineer fees 1 Sm TO Construction material and labour costs (including unused materials) At 30 September 20X8, the date when the head office extension became available for use, the cost of unused materials on site amounted to 50-5m. At that date, the total borrowing costs incurred on a loan which was used to specifically finance the head office extension amounted to S0-8m Linetti Co also acquired 100% of a subsidiary, Scully Co, on January 20X8. The carrying amount of the assets of Scully Co in the consolidated financial statements of the Linetti group at 31 December 20x8, immediately before an impairment view, were as follows: Sm Goodwill Brand name 2.0 Property, plant and equipment 60 Current assets at recoverable amount 2,4 118 The recoverable amount of Scully Co was estimated at 59.fm at 31 December 20X8 and the impairment of the investment in Scally Co was deemed to be 52.2m For the year ended 31 December 20X6. bermach should be capitalised in respect of the construction of the extension to the head office building? A. $18 4m B. S17-6m C. $18-9m DS181m 2. Linetti Co incurred further expenditure on the head office extension after it had been completed. Which of the following would qualify as capital expenditure? A Property insurance premiums incurred B. Installation of new office fixtures and finting C Marketing coststelling the public that the head office extension is operational D. Maintenance and relocation of computers and related office equipment 3. At 31 December 20X9, the directors of Linetti o decide to adopt the evaluation model of IAS 16 Property. Piant and Equipment for Linea Co's property. In accordance with IAS 16, which of the following statements is FALSE? A. In subsequent years, the depreciation will be based on the evalued amount of the head office building as opposed to its cost B. Any revaluation gain on the head office building is recognised in other comprchesive income and any revaluation loss is recognised in profit or loss C. Each component part of the head office building is revalued separately D. The residual value and the seful life of the head office building must be reviewed cach year

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts