Question: Need Urgent Help! Time Series Concepts 1. Let Y: represent a stochastic process. Under what conditions is Yt covariance stationary? Realizations from four stochastic processes

Need Urgent Help!

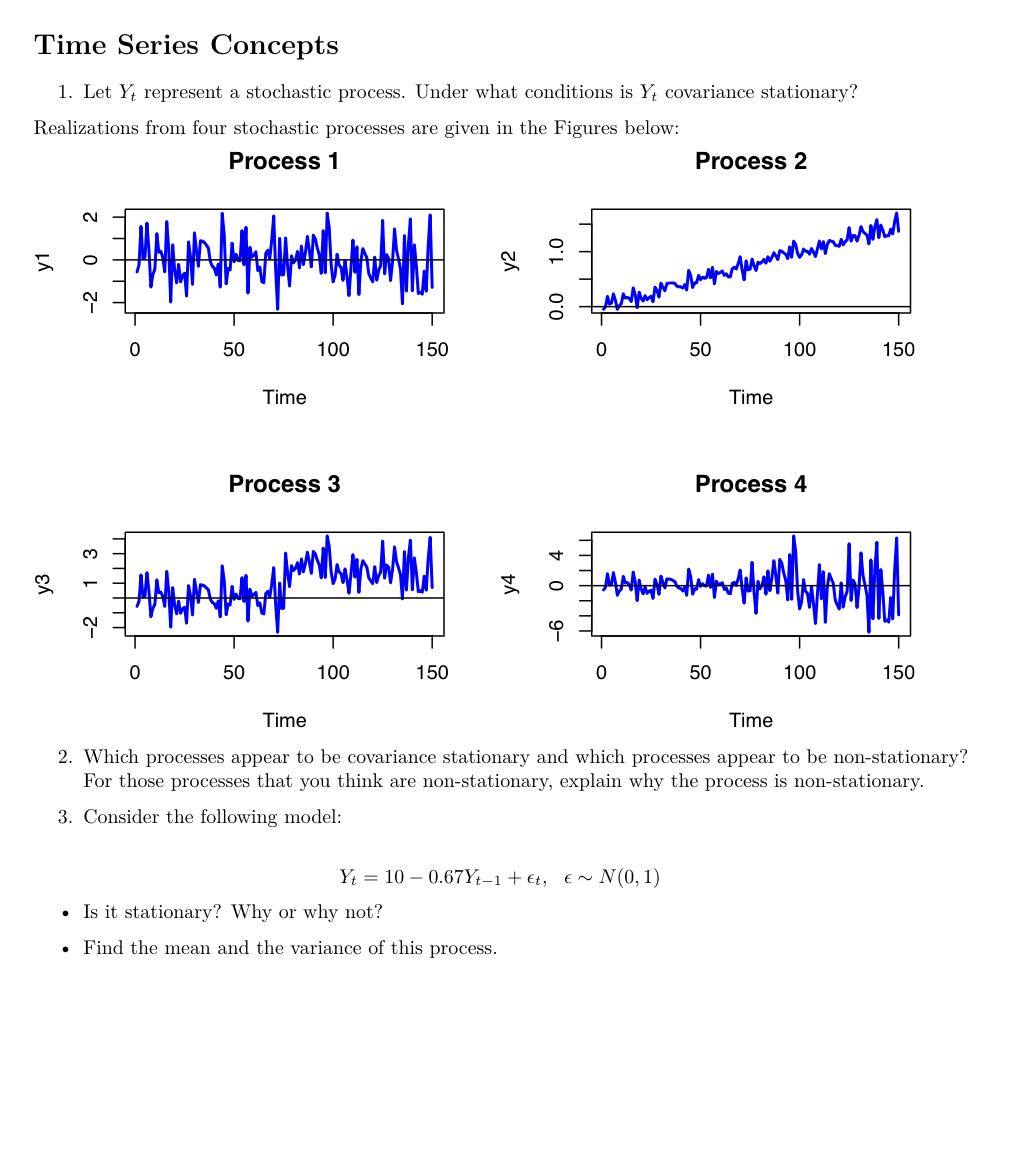

Time Series Concepts 1. Let Y: represent a stochastic process. Under what conditions is Yt covariance stationary? Realizations from four stochastic processes are given in the Figures below: Process 1 Process 2 N C! a 0 EL '- N C) ' d O 50 100 150 0 50 100 150 Time Time no w a v a o '1\" 'i' O 50 100 150 0 50 100 150 Time Time 2. Which processes appear to be covariance stationary and which processes appear to be non-stationary? For those processes that you think are non-stationary, explain why the process is non-stationary. 3. Consider the following model: Ya: = 10 0.67Yi1 + Q, E N N(0,1) - Is it stationary? Why or why not? - Find the mean and the variance of this process

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts