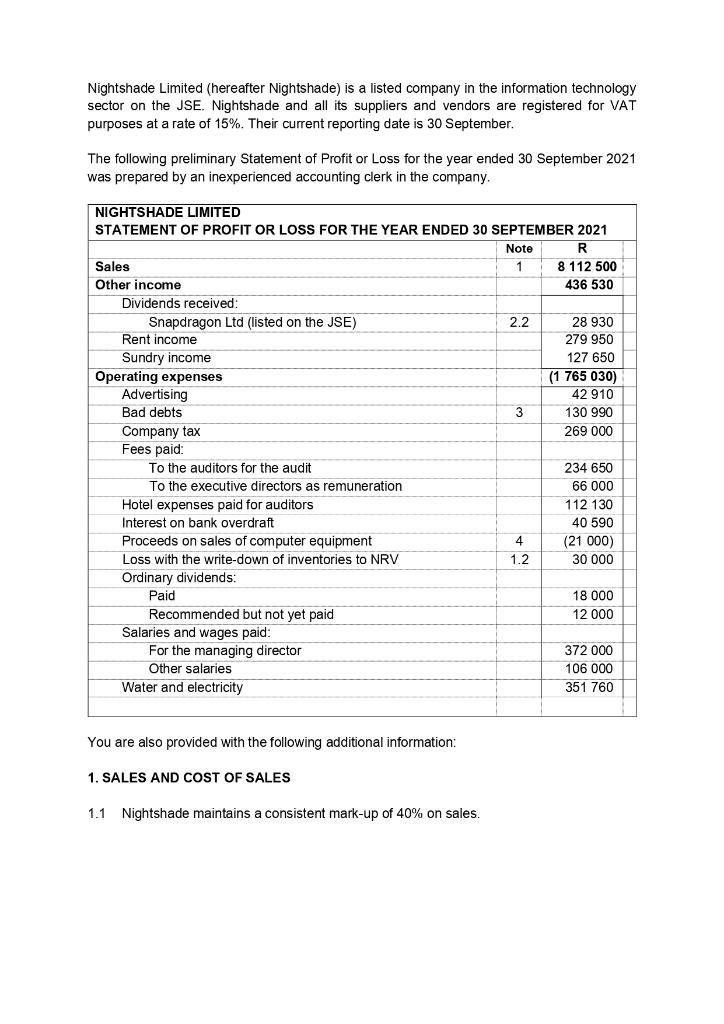

Nightshade Limited (hereafter Nightshade) is a listed company in the information technology sector on the JSE....

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

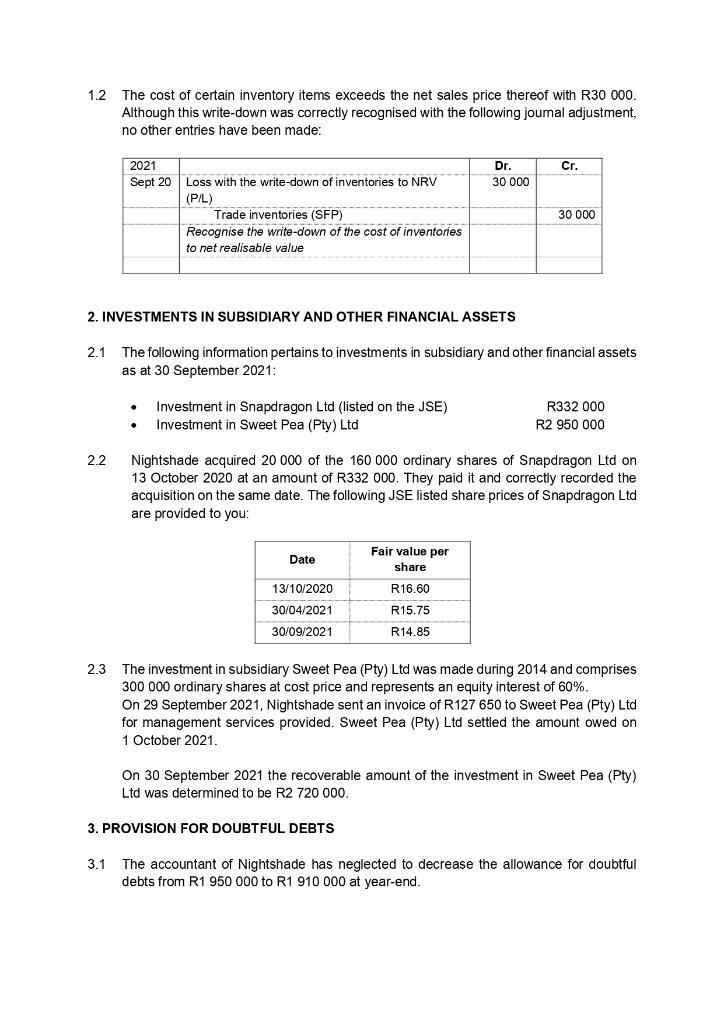

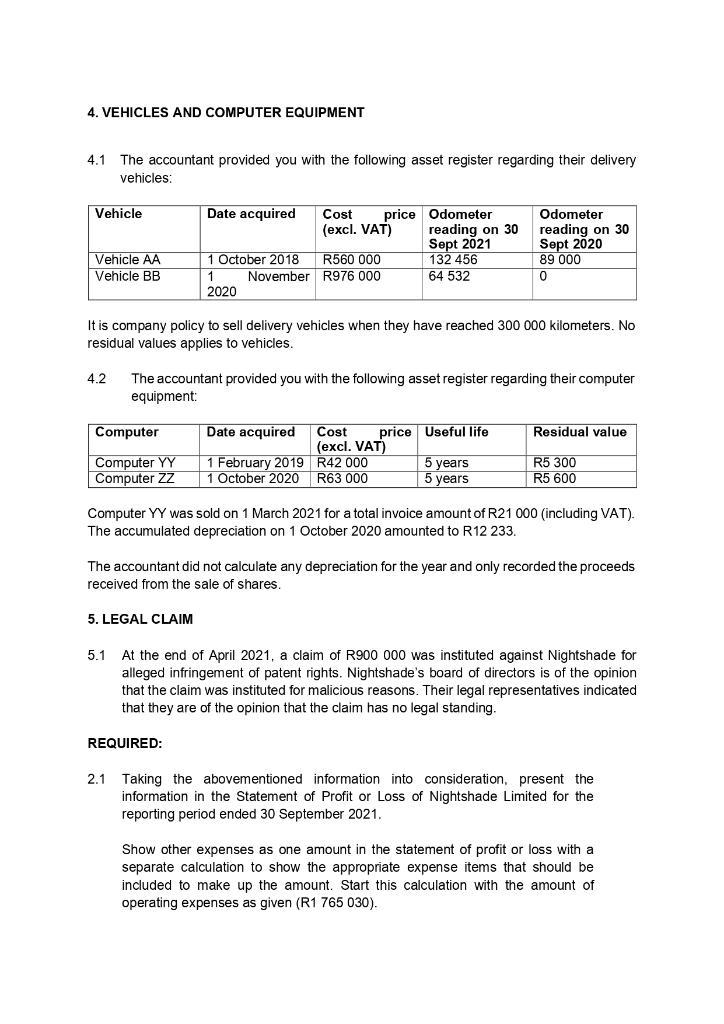

Nightshade Limited (hereafter Nightshade) is a listed company in the information technology sector on the JSE. Nightshade and all its suppliers and vendors are registered for VAT purposes at a rate of 15%. Their current reporting date is 30 September. The following preliminary Statement of Profit or Loss for the year ended 30 September 2021 was prepared by an inexperienced accounting clerk in the company. NIGHTSHADE LIMITED STATEMENT OF PROFIT OR LOSS FOR THE YEAR ENDED 30 SEPTEMBER 2021 Sales Other income Dividends received: Snapdragon Ltd (listed on the JSE) Rent income Sundry income Operating expenses Advertising Bad debts Company tax Fees paid: To the auditors for the audit To the executive directors as remuneration Hotel expenses paid for auditors Interest on bank overdraft Proceeds on sales of computer equipment Loss with the write-down of inventories to NRV Ordinary dividends: Paid Recommended but not yet paid Salaries and wages paid: For the managing director Other salaries Water and electricity You are also provided with the following additional information: 1. SALES AND COST OF SALES 1.1 Nightshade maintains a consistent mark-up of 40% on sales. Note 1 2.2 3 4 +2 1.2 R 8 112 500 436 530 28 930 279 950 127 650 (1 765 030) 42 910 130 990 269 000 234 650 66 000 112 130 40 590 (21 000) 30 000 18 000 12 000 372 000 106 000 351 760 1.2 The cost of certain inventory items exceeds the net sales price thereof with R30 000. Although this write-down was correctly recognised with the following journal adjustment, no other entries have been made: 2.2 2021 Sept 20 Loss with the write-down of inventories to NRV (P/L) 2. INVESTMENTS IN SUBSIDIARY AND OTHER FINANCIAL ASSETS 3.1 Trade inventories (SFP) Recognise the write-down of the cost of inventories to net realisable value . 2.1 The following information pertains to investments in subsidiary and other financial assets as at 30 September 2021: Investment in Snapdragon Ltd (listed on the JSE) Investment in Sweet Pea (Pty) Ltd Dr. 30 000 Date 13/10/2020 30/04/2021 30/09/2021 Cr. Fair value per share R16.60 R15.75 R14.85 30 000 Nightshade acquired 20 000 of the 160 000 ordinary shares of Snapdragon Ltd on 13 October 2020 at an amount of R332 000. They paid it and correctly recorded the acquisition on the same date. The following JSE listed share prices of Snapdragon Ltd are provided to you: R332 000 R2 950 000 2.3 The investment in subsidiary Sweet Pea (Pty) Ltd was made during 2014 and comprises 300 000 ordinary shares at cost price and represents an equity interest of 60%. On 29 September 2021, Nightshade sent an invoice of R127 650 to Sweet Pea (Pty) Ltd for management services provided. Sweet Pea (Pty) Ltd settled the amount owed on 1 October 2021. On 30 September 2021 the recoverable amount of the investment in Sweet Pea (Pty) Ltd was determined to be R2 720 000. 3. PROVISION FOR DOUBTFUL DEBTS The accountant of Nightshade has neglected to decrease the allowance for doubtful debts from R1 950 000 to R1 910 000 at year-end. 4. VEHICLES AND COMPUTER EQUIPMENT 4.1 The accountant provided you with the following asset register regarding their delivery vehicles: Vehicle Vehicle AA Vehicle BB Computer Computer YY Computer ZZ Date acquired 1 October 2018 1 2020 November 5. LEGAL CLAIM Cost (excl. VAT) REQUIRED: price Odometer R560 000 R976 000 It is company policy to sell delivery vehicles when they have reached 300 000 kilometers. No residual values applies to vehicles. Date acquired February 2019 1 October 2020 4.2 The accountant provided you with the following asset register regarding their computer equipment: reading on 30 Sept 2021 132 456 64 532 Cost price (excl. VAT) R42 000 R63 000 Odometer reading on 30 Sept 2020 89 000 0 Useful life 5 years 5 years Residual value Computer YY was sold on 1 March 2021 for a total invoice amount of R21 000 (including VAT) The accumulated depreciation on 1 October 2020 amounted to R12 233. R5 300 R5 600 The accountant did not calculate any depreciation for the year and only recorded the proceeds received from the sale of shares. 5.1 At the end of April 2021, a claim of R900 000 was instituted against Nightshade for alleged infringement of patent rights. Nightshade's board of directors is of the opinion that the claim was instituted for malicious reasons. Their legal representatives indicated that they are of the opinion that the claim has no legal standing. 2.1 Taking the abovementioned information into consideration, present the information in the Statement of Profit or Loss of Nightshade Limited for the reporting period ended 30 September 2021. Show other expenses as one amount in the statement of profit or loss with a separate calculation to show the appropriate expense items that should be included to make up the amount. Start this calculation with the amount of operating expenses as given (R1 765 030). 2.2 Disclose the following notes in the financial statements of Nightshade Limited forthe reporting period ended 30 September 2021: PLEASE NOTE: . . Note 4: Investment in subsidiary Note 5: Contingent liability . No comparative figures are required. Notes in respect accounting policy, compliance with IFRS and measurement bases arenot required. Inventories are valued at the lower of cost, according to the first-in-first-out method andnet realisable value and the company uses the perpetual inventory system. Round off all amounts to the nearest Rand. Show all the necessary calculations as marks are awarded for these. Nightshade Limited (hereafter Nightshade) is a listed company in the information technology sector on the JSE. Nightshade and all its suppliers and vendors are registered for VAT purposes at a rate of 15%. Their current reporting date is 30 September. The following preliminary Statement of Profit or Loss for the year ended 30 September 2021 was prepared by an inexperienced accounting clerk in the company. NIGHTSHADE LIMITED STATEMENT OF PROFIT OR LOSS FOR THE YEAR ENDED 30 SEPTEMBER 2021 Sales Other income Dividends received: Snapdragon Ltd (listed on the JSE) Rent income Sundry income Operating expenses Advertising Bad debts Company tax Fees paid: To the auditors for the audit To the executive directors as remuneration Hotel expenses paid for auditors Interest on bank overdraft Proceeds on sales of computer equipment Loss with the write-down of inventories to NRV Ordinary dividends: Paid Recommended but not yet paid Salaries and wages paid: For the managing director Other salaries Water and electricity You are also provided with the following additional information: 1. SALES AND COST OF SALES 1.1 Nightshade maintains a consistent mark-up of 40% on sales. Note 1 2.2 3 4 +2 1.2 R 8 112 500 436 530 28 930 279 950 127 650 (1 765 030) 42 910 130 990 269 000 234 650 66 000 112 130 40 590 (21 000) 30 000 18 000 12 000 372 000 106 000 351 760 1.2 The cost of certain inventory items exceeds the net sales price thereof with R30 000. Although this write-down was correctly recognised with the following journal adjustment, no other entries have been made: 2.2 2021 Sept 20 Loss with the write-down of inventories to NRV (P/L) 2. INVESTMENTS IN SUBSIDIARY AND OTHER FINANCIAL ASSETS 3.1 Trade inventories (SFP) Recognise the write-down of the cost of inventories to net realisable value . 2.1 The following information pertains to investments in subsidiary and other financial assets as at 30 September 2021: Investment in Snapdragon Ltd (listed on the JSE) Investment in Sweet Pea (Pty) Ltd Dr. 30 000 Date 13/10/2020 30/04/2021 30/09/2021 Cr. Fair value per share R16.60 R15.75 R14.85 30 000 Nightshade acquired 20 000 of the 160 000 ordinary shares of Snapdragon Ltd on 13 October 2020 at an amount of R332 000. They paid it and correctly recorded the acquisition on the same date. The following JSE listed share prices of Snapdragon Ltd are provided to you: R332 000 R2 950 000 2.3 The investment in subsidiary Sweet Pea (Pty) Ltd was made during 2014 and comprises 300 000 ordinary shares at cost price and represents an equity interest of 60%. On 29 September 2021, Nightshade sent an invoice of R127 650 to Sweet Pea (Pty) Ltd for management services provided. Sweet Pea (Pty) Ltd settled the amount owed on 1 October 2021. On 30 September 2021 the recoverable amount of the investment in Sweet Pea (Pty) Ltd was determined to be R2 720 000. 3. PROVISION FOR DOUBTFUL DEBTS The accountant of Nightshade has neglected to decrease the allowance for doubtful debts from R1 950 000 to R1 910 000 at year-end. 4. VEHICLES AND COMPUTER EQUIPMENT 4.1 The accountant provided you with the following asset register regarding their delivery vehicles: Vehicle Vehicle AA Vehicle BB Computer Computer YY Computer ZZ Date acquired 1 October 2018 1 2020 November 5. LEGAL CLAIM Cost (excl. VAT) REQUIRED: price Odometer R560 000 R976 000 It is company policy to sell delivery vehicles when they have reached 300 000 kilometers. No residual values applies to vehicles. Date acquired February 2019 1 October 2020 4.2 The accountant provided you with the following asset register regarding their computer equipment: reading on 30 Sept 2021 132 456 64 532 Cost price (excl. VAT) R42 000 R63 000 Odometer reading on 30 Sept 2020 89 000 0 Useful life 5 years 5 years Residual value Computer YY was sold on 1 March 2021 for a total invoice amount of R21 000 (including VAT) The accumulated depreciation on 1 October 2020 amounted to R12 233. R5 300 R5 600 The accountant did not calculate any depreciation for the year and only recorded the proceeds received from the sale of shares. 5.1 At the end of April 2021, a claim of R900 000 was instituted against Nightshade for alleged infringement of patent rights. Nightshade's board of directors is of the opinion that the claim was instituted for malicious reasons. Their legal representatives indicated that they are of the opinion that the claim has no legal standing. 2.1 Taking the abovementioned information into consideration, present the information in the Statement of Profit or Loss of Nightshade Limited for the reporting period ended 30 September 2021. Show other expenses as one amount in the statement of profit or loss with a separate calculation to show the appropriate expense items that should be included to make up the amount. Start this calculation with the amount of operating expenses as given (R1 765 030). 2.2 Disclose the following notes in the financial statements of Nightshade Limited forthe reporting period ended 30 September 2021: PLEASE NOTE: . . Note 4: Investment in subsidiary Note 5: Contingent liability . No comparative figures are required. Notes in respect accounting policy, compliance with IFRS and measurement bases arenot required. Inventories are valued at the lower of cost, according to the first-in-first-out method andnet realisable value and the company uses the perpetual inventory system. Round off all amounts to the nearest Rand. Show all the necessary calculations as marks are awarded for these.

Expert Answer:

Answer rating: 100% (QA)

To analyze the provided information and answer the questions lets start with th... View the full answer

Related Book For

Smith and Roberson Business Law

ISBN: 978-0538473637

15th Edition

Authors: Richard A. Mann, Barry S. Roberts

Posted Date:

Students also viewed these accounting questions

-

In its statement of profit or loss for the year ended 30 June 2016, Lulu Ltd reported the following condensed data: Required (a) Prepare a fully classified statement of profit or loss. (b) Calculate...

-

You work as department head in the information technology (IT) department at First Federal Bank. Part of your job is to conduct an ongoing assessment of risk for the institution and to recommend...

-

The following statement of profit or loss extracts are from entities employing different inventory recording methods. Required (a) Using the information provided, prepare closing general journal...

-

Complete the horizontal analysis of the following comparative income statement? Mile Wide Organic Woolens, Inc. Comparative Income Statement For Years Ending December 31, 2012 and 2013 Increase...

-

Tiffany & Company is a luxury jeweler and specialty retailer that sells timepieces, sterling silverware, china, crystal, fragrances, and accessories through its retail stores worldwide. Signet...

-

An Oklahoma manufacturer makes two products: speaker telephones (X1) and pushbutton telephones (X2). The following goal programming model has been formulated to find the number of each to produce...

-

In 2001, the City of New York and the Dormitory Authority of the State of New York (DASNY) entered into an agreement to build a forensic biology laboratory in Manhattan. Per the agreement, DASNY...

-

Clark Property Management is responsible for the maintenance, rental, and day-to-day operation of a large apartment complex on the east side of New Orleans. George Clark is especially concerned about...

-

Activity 3 Response: As an investigation of scientific question B, consider an object that is not the human body, but that also has a consistently higher temperature than the environment. Based on...

-

1. A typical tube-style incandescent light bulb lasts for 1,000 hours and is available to consumers for $3.00 per bulb. A manufacturer has produced a tube-style halogen light bulb that gives the same...

-

Each of the Scriptures below concern a given, criminal procedure topic. All Scriptures are from the New International Version, 1984. Begin this assignment by meditating on the given Scriptures. Open...

-

No matter how great bankers are at their jobs, they will ultimately be "failures" if credit risk and interest rate risk is not managed properly. The good thing is that bankers have found different...

-

Question #1 Talent Inc. is considering a project that has the following cash flow and WACC data. WACC: 12% Year 0 1 2 3 Cash flows -$1,500 $500 ...

-

Prepare a bank reconciliation for March 31, 2012, given the following A. The bank statement balance is $4,000 B. The cash account balance is $3,000 C. The Outstanding checks total $1,500 D. Deposits...

-

Identify sources of income that are generally excluded from Active Business Income. How does Active Business Income affect the calculation of the Small Business Deduction pursuant to ITA 125(1)? The...

-

A seasonal viral infection due to a virus named RandomV is prevalent in Delhi. About 1 in 1000 people in Delhi are expected to be infected by RandomV. The virus spreads from an infected person to...

-

EDD-ANJ Below is the data in the usual notations about 5 jobs (A through E), find the value of Xin the table below using the EDD rule. Jobs PT DD Jobs PT CT-FT 20 30 30 50 10 25 16 80 18 60 A B C D E...

-

Trade credit from suppliers is a very costly source of funds when discounts are lost. Explain why many firms rely on this source of funds to finance their temporary working capital.

-

Charles and Jack orally agreed to become partners in a tool and die business. Charles, who had experience in tool and die work, was to operate the business. Jack was to take no active part but was to...

-

Plaintiff, Mary Mansi, claims that eighteen checks on her account contain forgeries but were paid by the defendant bank, Sterling National Bank. These checks bore signatures which, according to the...

-

Payroll Advance, Inc. (Appellant) appeals from the judgment of the trial court entered in favor of Barbara Yates (Respondent) on Appellants petition for injunctive relief and breach of contract of an...

-

Do you think the trend discussed in the case will help companies hire more skilled managers and employees to staff foreign operations? Explain. According to a recent report by the Chronicle of Higher...

-

Some companies agree that the move toward internationalization by U.S. universities primarily reflect an attempt to get more money because foreign buyers are willing to pay top dollar to obtain a...

-

Form teams of five. Each team will come up with a list of five positives and five negatives for the trend discussed in the case. Each team will outline a set of implications of what this trend means...

Study smarter with the SolutionInn App