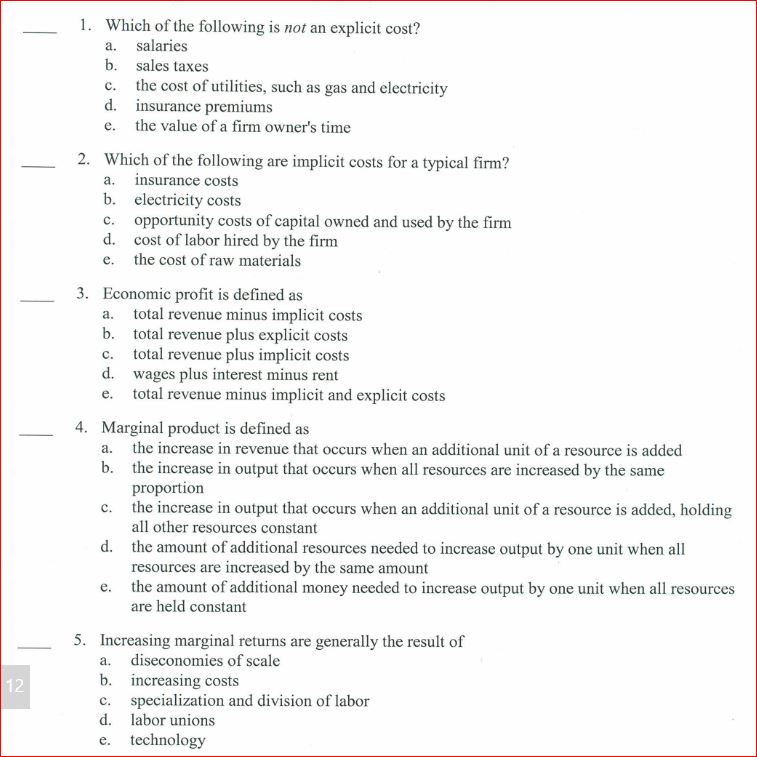

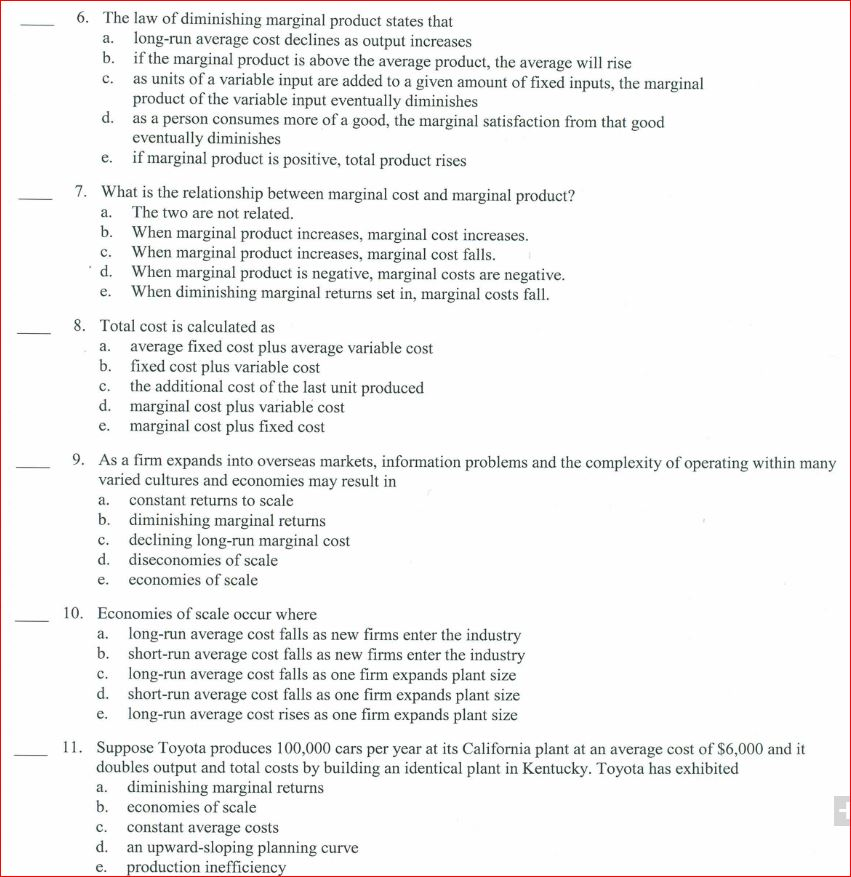

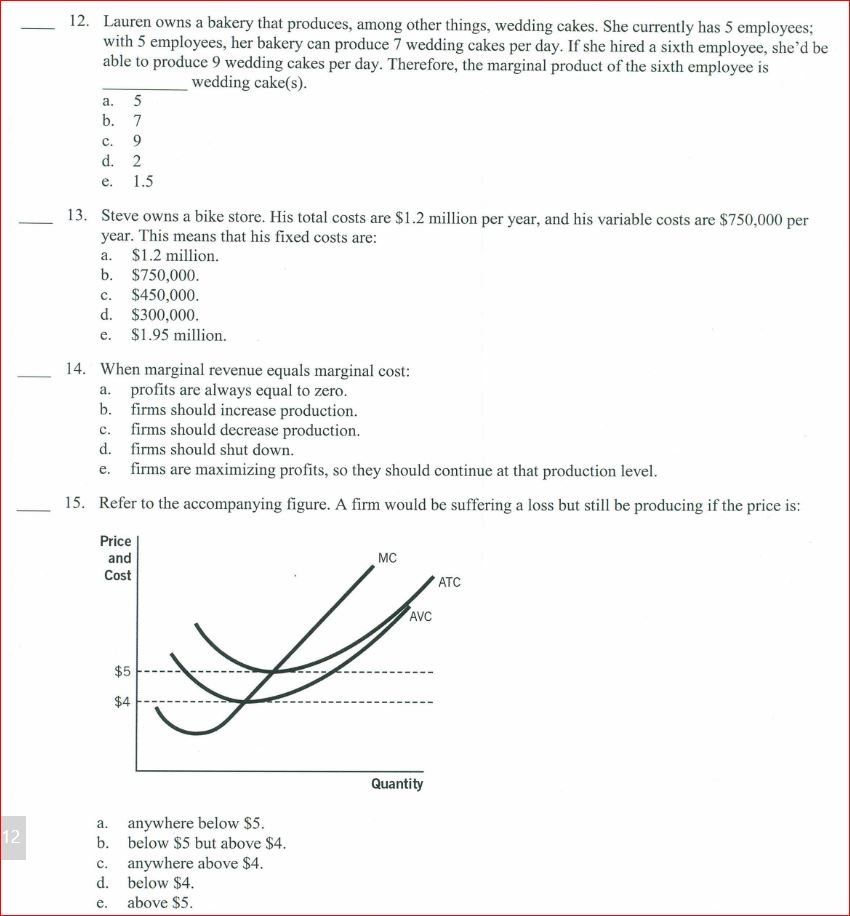

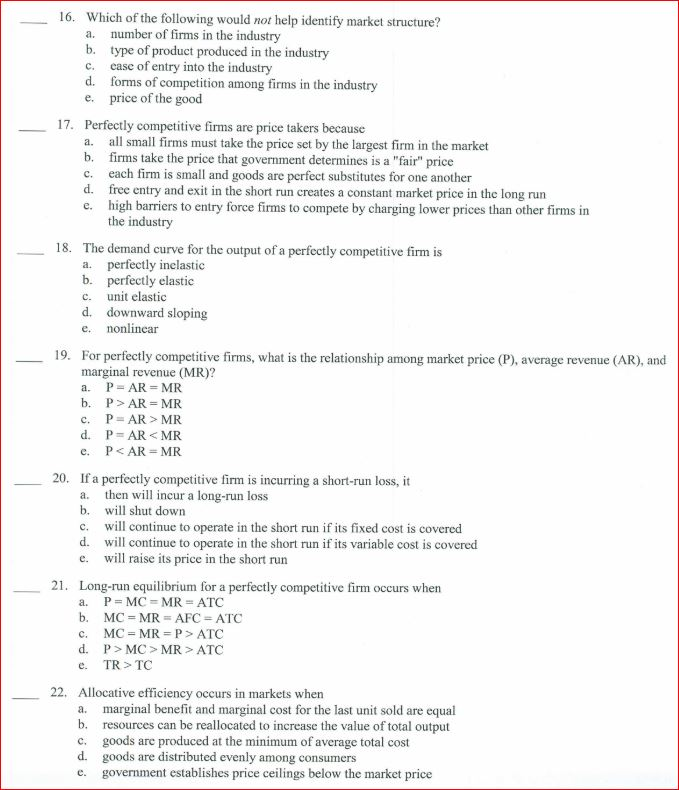

12 1. Which of the following is not an explicit cost? a. salaries b. sales taxes...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

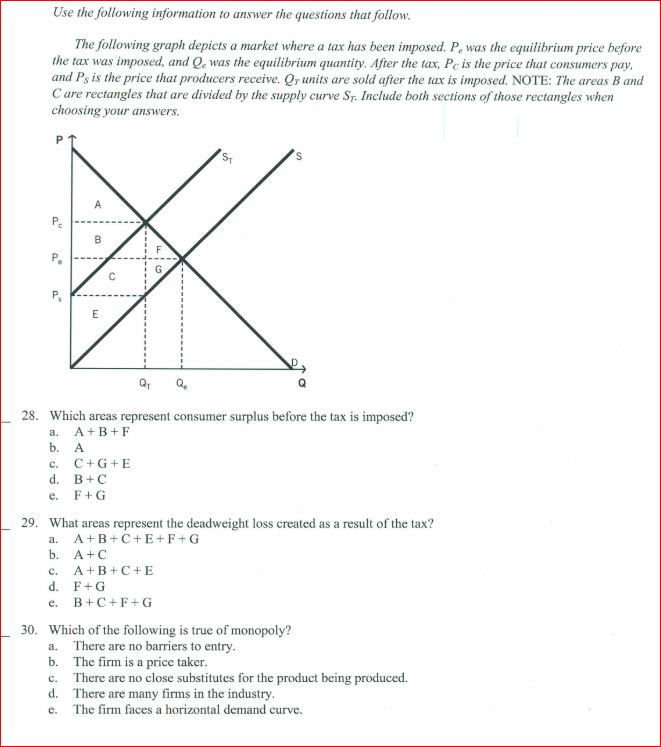

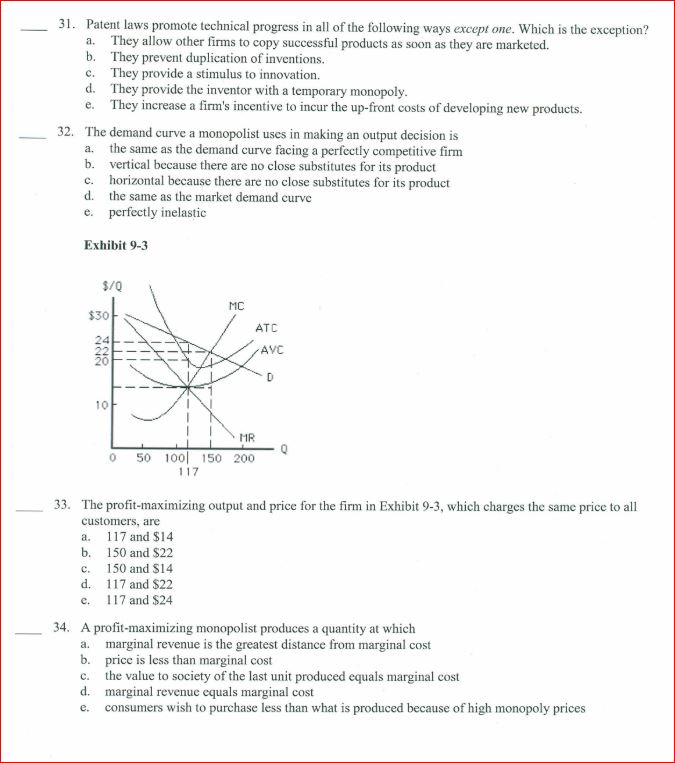

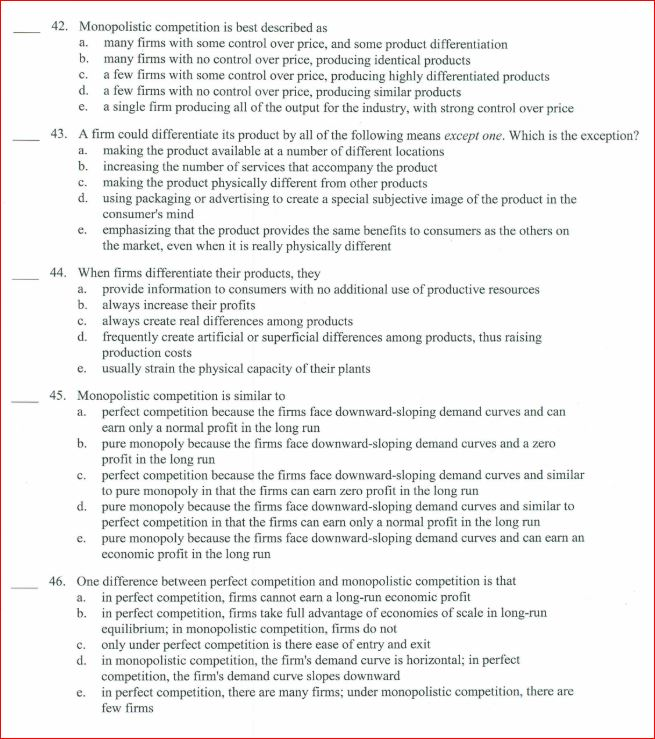

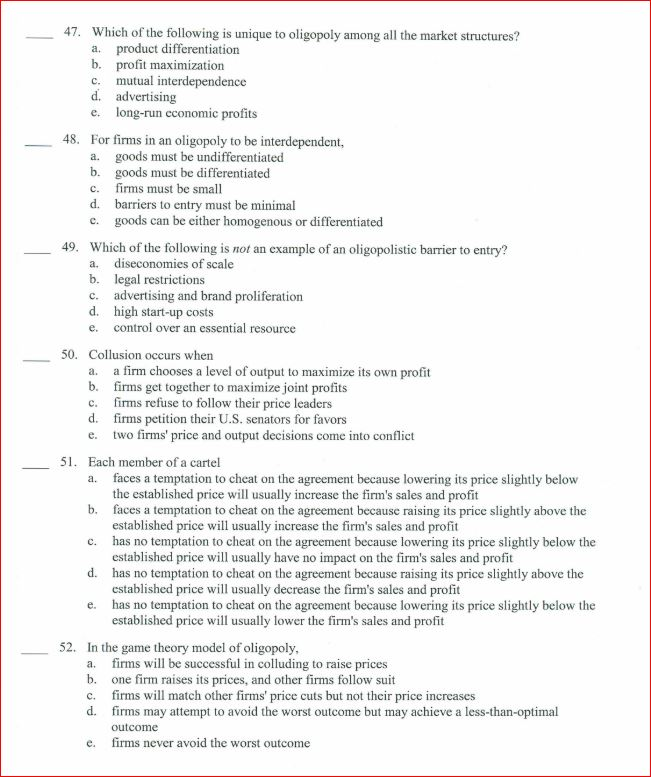

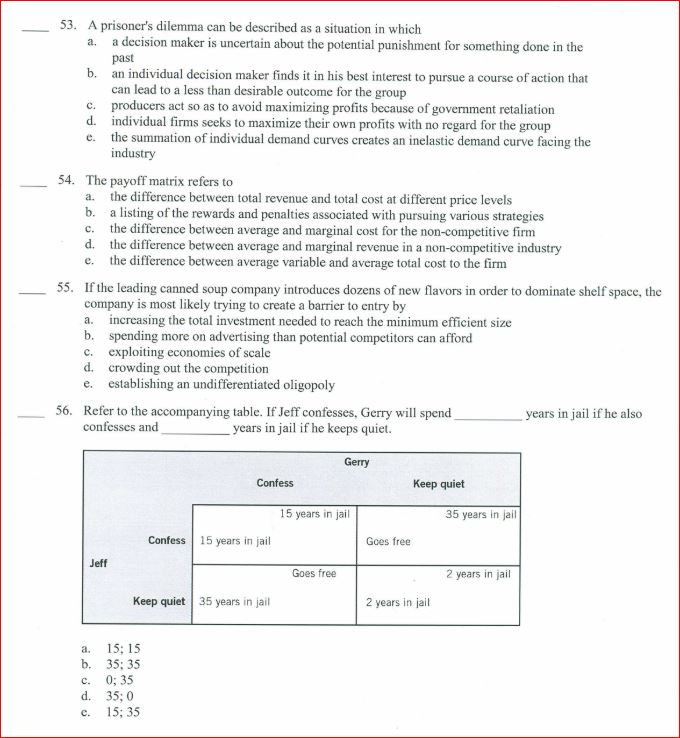

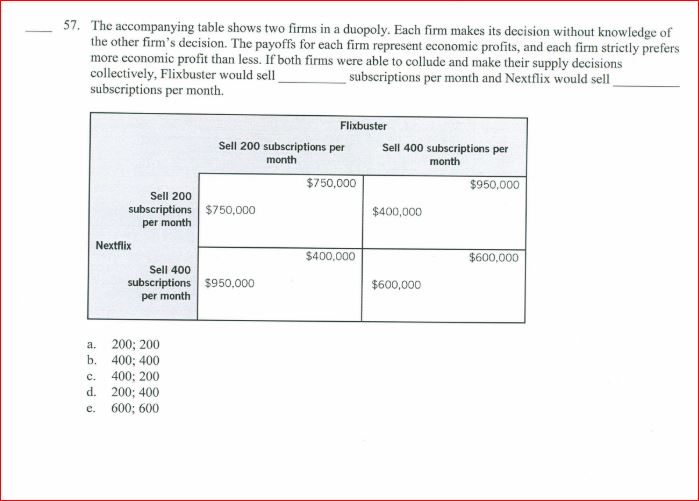

12 1. Which of the following is not an explicit cost? a. salaries b. sales taxes c. the cost of utilities, such as gas and electricity insurance premiums d. e. the value of a firm owner's time 2. Which of the following are implicit costs for a typical firm? a. insurance costs b. electricity costs c. d. opportunity costs of capital owned and used by the firm cost of labor hired by the firm the cost of raw materials e. 3. Economic profit is defined as a. total revenue minus implicit costs b. total revenue plus explicit costs total revenue plus implicit costs d. wages plus interest minus rent C. e. total revenue minus implicit and explicit costs 4. Marginal product is defined as a. the increase in revenue that occurs when an additional unit of a resource is added b. the increase in output that occurs when all resources are increased by the same proportion c. the increase in output that occurs when an additional unit of a resource is added, holding all other resources constant d. the amount of additional resources needed to increase output by one unit when all resources are increased by the same amount e. the amount of additional money needed to increase output by one unit when all resources are held constant 5. Increasing marginal returns are generally the result of a. diseconomies of scale b. increasing costs c. specialization and division of labor d. labor unions e. technology 6. The law of diminishing marginal product states that a. long-run average cost declines as output increases b. if the marginal product is above the average product, the average will rise C. as units of a variable input are added to a given amount of fixed inputs, the marginal product of the variable input eventually diminishes d. as a person consumes more of a good, the marginal satisfaction from that good eventually diminishes if marginal product is positive, total product rises e. 7. What is the relationship between marginal cost and marginal product? a. The two are not related. b. When marginal product increases, marginal cost increases. C. When marginal product increases, marginal cost falls. d. When marginal product is negative, marginal costs are negative. e. When diminishing marginal returns set in, marginal costs fall. 8. Total cost is calculated as a. average fixed cost plus average variable cost b. fixed cost plus variable cost C. the additional cost of the last unit produced d. marginal cost plus variable cost e. marginal cost plus fixed cost 9. As a firm expands into overseas markets, information problems and the complexity of operating within many varied cultures and economies may result in a. constant returns to scale b. diminishing marginal returns c. declining long-run marginal cost d. diseconomies of scale e. economies of scale 10. Economies of scale occur where b. a. long-run average cost falls as new firms enter the industry short-run average cost falls as new firms enter the industry C. long-run average cost falls as one firm expands plant size d. short-run average cost falls as one firm expands plant size e. long-run average cost rises as one firm expands plant size 11. Suppose Toyota produces 100,000 cars per year at its California plant at an average cost of $6,000 and it doubles output and total costs by building an identical plant in Kentucky. Toyota has exhibited a. diminishing marginal returns b. economies of scale C. constant average costs d. e. an upward-sloping planning curve production inefficiency 12 12. Lauren owns a bakery that produces, among other things, wedding cakes. She currently has 5 employees; with 5 employees, her bakery can produce 7 wedding cakes per day. If she hired a sixth employee, she'd be able to produce 9 wedding cakes per day. Therefore, the marginal product of the sixth employee is wedding cake(s). 5 7 C. 9 d. 2 e. 1.5 a. b. 13. Steve owns a bike store. His total costs are $1.2 million per year, and his variable costs are $750,000 per year. This means that his fixed costs are: a. $1.2 million. b. $750,000. c. $450,000. d. $300,000. e. $1.95 million. 14. When marginal revenue equals marginal cost: a. profits are always equal to zero. b. firms should increase production. c. firms should decrease production. d. firms should shut down. e. firms are maximizing profits, so they should continue at that production level. 15. Refer to the accompanying figure. A firm would be suffering a loss but still be producing if the price is: Price and Cost $5 $4 a. anywhere below $5. b. below $5 but above $4. C. anywhere above $4. d. below $4. e. above $5. MC AVC Quantity ATC 16. Which of the following would not help identify market structure? a. number of firms in the industry b. type of product produced in the industry c. ease of entry into the industry d. forms of competition among firms in the industry e. price of the good 17. Perfectly competitive firms are price takers because a. b. c. d. e. all small firms must take the price set by the largest firm in the market firms take the price that government determines is a "fair" price each firm is small and goods are perfect substitutes for one another free entry and exit in the short run creates a constant market price in the long run high barriers to entry force firms to compete by charging lower prices than other firms in the industry 18. The demand curve for the output of a perfectly competitive firm is a. perfectly inelastic b. perfectly elastic c. unit elastic d. downward sloping e. nonlinear 19. For perfectly competitive firms, what is the relationship among market price (P), average revenue (AR), and marginal revenue (MR)? a. P = AR = MR C. d. e. b. P> AR = MR P = AR > MR P= AR<MR P<AR=MR 20. If a perfectly competitive firm is incurring a short-run loss, it a. then will incur a long-run loss b. will shut down c. will continue to operate in the short run if its fixed cost is covered d. will continue to operate in the short run if its variable cost is covered e. will raise its price in the short run 21. Long-run equilibrium for a perfectly competitive firm occurs when P = MC=MR = ATC â. b. MCMR = AFC = ATC C. MC MR P> ATC d. P> MC> MR > ATC e. TR> TC 22. Allocative efficiency occurs in markets when a. marginal benefit and marginal cost for the last unit sold are equal b. resources can be reallocated to increase the value of total output c. goods are produced at the minimum of average total cost d. goods are distributed evenly among consumers e. government establishes price ceilings below the market price 23. The term productive efficiency refers to a. any short-run equilibrium position of the competitive firm b. the production of all goods and services that consumers need c. the production of a good at the lowest long-run average cost d. the equality between average total and average variable cost satisfying the condition that MR = MC e. 24. Social welfare is a. a government program through which society takes care of low-income people the overall well-being of people in the economy b. c. measured by spending on party supplies, restaurant meals, and movie tickets d. e. All the answers are correct. applies to sociology, not economics 25. The market for watches is perfectly competitive and is currently in equilibrium. What will happen if watches become more popular among college students? a. In the short run, firms will experience economic profits, but in the long run, firms will leave the market, bringing economic profits back down to zero. b. In the short run, firms will experience economic profits, but in the long run, firms will enter the market, bringing economic profits back down to zero. c. In the short run, firms will incur economic losses, but in the long run, firms will leave the market, bringing economic profits back down to zero. d. In the short run, firms will incur economic losses, but in the long run, firms will enter the market, bringing economic profits back down to zero. In both the short run and the long run, firms will experience zero economic profits. e. 26. Consumer surplus is defined as the: a. difference between the willingness to pay for a good and the willingness to sell it. total revenue earned from producing and selling some good. b. C. difference between the willingness to pay for a good and the price paid to get it. quantity of units that consumers want to buy at the market price. d. e. difference between the price the seller receives and the willingness to sell it. 27. Producer surplus is defined as the: b. a. difference between the willingness to pay for a good and the willingness to sell it. difference between the price the seller receives and the willingness to sell it. difference between the willingness to pay for a good and the price paid to get it. d. quantity of units that consumers want to buy at the market price. c. e. total revenue earned from producing and selling some good. Use the following information to answer the questions that follow. The following graph depicts a market where a tax has been imposed. P, was the equilibrium price before the tax was imposed, and Qe was the equilibrium quantity. After the tax, Pe is the price that consumers pay, and Ps is the price that producers receive. Qr units are sold after the tax is imposed. NOTE: The areas B and C are rectangles that are divided by the supply curve Sr. Include both sections of those rectangles when choosing your answers. A B X C P₂ E 0" 28. Which areas represent consumer surplus before the tax is imposed? a. A+B+F b. A C. C+G+E d. B+C e. F+G ST 29. What areas represent the deadweight loss created as a result of the tax? a. A+B+C+E+F+G b. A+C C. A+B+C+E d. F+G e. B+C+F+G 30. Which of the following is true of monopoly? a. There are no barriers to entry. b. The firm is a price taker. c. There are no close substitutes for the product being produced. There are many firms in the industry. d. e. The firm faces a horizontal demand curve. 31. Patent laws promote technical progress in all of the following ways except one. Which is the exception? a. They allow other firms to copy successful products as soon as they are marketed. b. They prevent duplication of inventions. c. They provide a stimulus to innovation. d. They provide the inventor with a temporary monopoly. e. They increase a firm's incentive to incur the up-front costs of developing new products. 32. The demand curve a monopolist uses in making an output decision is a. the same as the demand curve facing a perfectly competitive firm vertical because there are no close substitutes for its product c. horizontal because there are no close substitutes for its product b. the same as the market demand curve d. e. perfectly inelastic Exhibit 9-3 $/Q $30 24 NNN ONA 10 ill 111 MR 50 100 150 200 117 MC a. b. 150 and $22 c. 150 and $14 d. 117 and $22 e. 117 and $24 117 and $14 ATC AVC 33. The profit-maximizing output and price for the firm in Exhibit 9-3, which charges the same price to all customers, are D 34. A profit-maximizing monopolist produces a quantity at which a. marginal revenue is the greatest distance from marginal cost b. price is less than marginal cost c. the value to society of the last unit produced equals marginal cost d. e. marginal revenue equals marginal cost consumers wish to purchase less than what is produced because of high monopoly prices 35. Barriers to entry a. prevent monopolies from earning profit in the long run b. prevent monopolies from earning profit in the short run may allow monopolies to earn profit in the long run d. prevent government from regulating a monopoly e. prevent a natural monopoly from raising its price C. 36. Which of the following would not be considered price discrimination? a. Long distance telephone rates are cheaper late at night. b. Airline fares are cheaper if you reserve several weeks in advance. The price of lettuce is 59 cents a head and two for a dollar. c. d. The price of a brand-name prescription drug is higher than the price of a generic brand. e. Senior citizens pay less for a movie. 37. Three natural barriers to entry in Monopolies are: a. control of resources, economies of scale, and licensing. b. economies of scale, problems raising capital, and control of resources. c. problems raising capital, patents and copyright law, and licensing. d. control of resources, patents and copyright law, and economies of scale. e. control of resources, economies of scale, and licensing. 38. Two government-created barriers to entry in Monopolies are: licensing and economies of scale. a. b. c. d. e. licensing and control of resources. economies of scale and patent system/copyright law. licensing and patent system/copyright law. economies of scale and control of resources. 39. Patents and copyrights can: a. create strong incentives to develop new drugs. b. provide heavy competition in markets. c. never lead to deadweight loss. d. assure firms that their products will make a profit. e. be considered natural barriers. 40. Inefficient output and price, few choices, and rent seeking are all problems associated with: a. externalities. b. competitive markets. c. monopolies. d. scarcity. e. trade. 41. Most economists are against monopolies because: a. monopolists do not maximize profits. b. monopolies produce too much of product. C. monopolies offer more choices than are needed. d. monopolies can never produce the quantity that a perfectly competitive market would produce. e. monopolies do not offer any choice. 42. Monopolistic competition is best described as a. many firms with some control over price, and some product differentiation b. many firms with no control over price, producing identical products c. a few firms with some control over price, producing highly differentiated products d. a few firms with no control over price, producing similar products e. a single firm producing all of the output for the industry, with strong control over price 43. A firm could differentiate its product by all of the following means except one. Which is the exception? a. making the product available at a number of different locations increasing the number of services that accompany the product b. c. making the product physically different from other products d. using packaging or advertising to create a special subjective image of the product in the consumer's mind e. emphasizing that the product provides the same benefits to consumers as the others on the market, even when it is really physically different 44. When firms differentiate their products, they a. provide information to consumers with no additional use of productive resources always increase their profits b. c. always create real differences among products d. frequently create artificial or superficial differences among products, thus raising production costs e. usually strain the physical capacity of their plants 45. Monopolistic competition is similar to a. perfect competition because the firms face downward-sloping demand curves and can earn only a normal profit in the long run b. pure monopoly because the firms face downward-sloping demand curves and a zero profit in the long run c. perfect competition because the firms face downward-sloping demand curves and similar to pure monopoly in that the firms can earn zero profit in the long run d. pure monopoly because the firms face downward-sloping demand curves and similar to perfect competition in that the firms can earn only a normal profit in the long run e. pure monopoly because the firms face downward-sloping demand curves and can earn an economic profit in the long run 46. One difference between perfect competition and monopolistic competition is that in perfect competition, firms cannot earn a long-run economic profit in perfect competition, firms take full advantage of economies of scale in long-run equilibrium; in monopolistic competition, firms do not a. b. c. only under perfect competition is there ease of entry and exit d. in monopolistic competition, the firm's demand curve is horizontal; in perfect competition, the firm's demand curve slopes downward e. in perfect competition, there are many firms; under monopolistic competition, there are few firms 47. Which of the following is unique to oligopoly among all the market structures? a. product differentiation b. profit maximization c. mutual interdependence d. advertising e. long-run economic profits 48. For firms in an oligopoly to be interdependent, goods must be undifferentiated goods must be differentiated firms must be small a. b. c. d. barriers to entry must be minimal e. goods can be either homogenous or differentiated 49. Which of the following is not an example of an oligopolistic barrier to entry? a. diseconomies of scale b. legal restrictions c. advertising and brand proliferation d. e. 50. Collusion occurs when a. b. a firm chooses a level of output to maximize its own profit firms get together to maximize joint profits C. firms refuse to follow their price leaders d. firms petition their U.S. senators for favors e. two firms' price and output decisions come into conflict high start-up costs control over an essential resource 51. Each member of a cartel a. faces a temptation to cheat on the agreement because lowering its price slightly below the established price will usually increase the firm's sales and profit b. faces a temptation to cheat on the agreement because raising its price slightly above the established price will usually increase the firm's sales and profit has no temptation to cheat on the agreement because lowering its price slightly below the established price will usually have no impact on the firm's sales and profit C. d. has no temptation to cheat on the agreement because raising its price slightly above the established price will usually decrease the firm's sales and profit e. has no temptation to cheat on the agreement because lowering its price slightly below the established price will usually lower the firm's sales and profit 52. In the game theory model of oligopoly, a. firms will be successful in colluding to raise prices b. one firm raises its prices, and other firms follow suit C. firms will match other firms' price cuts but not their price increases d. firms may attempt to avoid the worst outcome but may achieve a less-than-optimal outcome firms never avoid the worst outcome e. 53. A prisoner's dilemma can be described as a situation in which a. a decision maker is uncertain about the potential punishment for something done in the past b. an individual decision maker finds it in his best interest to pursue a course of action that can lead to a less than desirable outcome for the group c. d. e. 54. The payoff matrix refers to a. the difference between total revenue and total cost at different price levels b. a listing of the rewards and penalties associated with pursuing various strategies C. the difference between average and marginal cost for the non-competitive firm d. the difference between average and marginal revenue in a non-competitive industry e. the difference between average variable and average total cost to the firm producers act so as to avoid maximizing profits because of government retaliation individual firms seeks to maximize their own profits with no regard for the group the summation of individual demand curves creates an inelastic demand curve facing the industry 55. If the leading canned soup company introduces dozens of new flavors in order to dominate shelf space, the company is most likely trying to create a barrier to entry by a. increasing the total investment needed to reach the minimum efficient size b. spending more on advertising than potential competitors can afford c. exploiting economies of scale d. crowding out the competition e. establishing an undifferentiated oligopoly 56. Refer to the accompanying table. If Jeff confesses, Gerry will spend confesses and years in jail if he keeps quiet. Jeff a. b. 15; 15 35; 35: C. 0; 35 d. 35; 0 C. Confess Keep quiet 35 years in jail 15; 35 Confess 15 years in jail Gerry 15 years in jail Goes free Goes free Keep quiet 2 years in jail 35 years in jail 2 years in jail years in jail if he also 57. The accompanying table shows two firms in a duopoly. Each firm makes its decision without knowledge of the other firm's decision. The payoffs for each firm represent economic profits, and each firm strictly prefers more economic profit than less. If both firms were able to collude and make their supply decisions collectively, Flixbuster would sell subscriptions per month and Nextflix would sell subscriptions per month. Nextflix a. b. C. d. e. Sell 200 subscriptions $750,000 per month Sell 400 subscriptions $950,000 per month 200; 200 400; 400 Sell 200 subscriptions per month 400; 200 200; 400 600; 600 Flixbuster $750,000 $400,000 Sell 400 subscriptions per month $400,000 $600,000 $950,000 $600,000 12 1. Which of the following is not an explicit cost? a. salaries b. sales taxes c. the cost of utilities, such as gas and electricity insurance premiums d. e. the value of a firm owner's time 2. Which of the following are implicit costs for a typical firm? a. insurance costs b. electricity costs c. d. opportunity costs of capital owned and used by the firm cost of labor hired by the firm the cost of raw materials e. 3. Economic profit is defined as a. total revenue minus implicit costs b. total revenue plus explicit costs total revenue plus implicit costs d. wages plus interest minus rent C. e. total revenue minus implicit and explicit costs 4. Marginal product is defined as a. the increase in revenue that occurs when an additional unit of a resource is added b. the increase in output that occurs when all resources are increased by the same proportion c. the increase in output that occurs when an additional unit of a resource is added, holding all other resources constant d. the amount of additional resources needed to increase output by one unit when all resources are increased by the same amount e. the amount of additional money needed to increase output by one unit when all resources are held constant 5. Increasing marginal returns are generally the result of a. diseconomies of scale b. increasing costs c. specialization and division of labor d. labor unions e. technology 6. The law of diminishing marginal product states that a. long-run average cost declines as output increases b. if the marginal product is above the average product, the average will rise C. as units of a variable input are added to a given amount of fixed inputs, the marginal product of the variable input eventually diminishes d. as a person consumes more of a good, the marginal satisfaction from that good eventually diminishes if marginal product is positive, total product rises e. 7. What is the relationship between marginal cost and marginal product? a. The two are not related. b. When marginal product increases, marginal cost increases. C. When marginal product increases, marginal cost falls. d. When marginal product is negative, marginal costs are negative. e. When diminishing marginal returns set in, marginal costs fall. 8. Total cost is calculated as a. average fixed cost plus average variable cost b. fixed cost plus variable cost C. the additional cost of the last unit produced d. marginal cost plus variable cost e. marginal cost plus fixed cost 9. As a firm expands into overseas markets, information problems and the complexity of operating within many varied cultures and economies may result in a. constant returns to scale b. diminishing marginal returns c. declining long-run marginal cost d. diseconomies of scale e. economies of scale 10. Economies of scale occur where b. a. long-run average cost falls as new firms enter the industry short-run average cost falls as new firms enter the industry C. long-run average cost falls as one firm expands plant size d. short-run average cost falls as one firm expands plant size e. long-run average cost rises as one firm expands plant size 11. Suppose Toyota produces 100,000 cars per year at its California plant at an average cost of $6,000 and it doubles output and total costs by building an identical plant in Kentucky. Toyota has exhibited a. diminishing marginal returns b. economies of scale C. constant average costs d. e. an upward-sloping planning curve production inefficiency 12 12. Lauren owns a bakery that produces, among other things, wedding cakes. She currently has 5 employees; with 5 employees, her bakery can produce 7 wedding cakes per day. If she hired a sixth employee, she'd be able to produce 9 wedding cakes per day. Therefore, the marginal product of the sixth employee is wedding cake(s). 5 7 C. 9 d. 2 e. 1.5 a. b. 13. Steve owns a bike store. His total costs are $1.2 million per year, and his variable costs are $750,000 per year. This means that his fixed costs are: a. $1.2 million. b. $750,000. c. $450,000. d. $300,000. e. $1.95 million. 14. When marginal revenue equals marginal cost: a. profits are always equal to zero. b. firms should increase production. c. firms should decrease production. d. firms should shut down. e. firms are maximizing profits, so they should continue at that production level. 15. Refer to the accompanying figure. A firm would be suffering a loss but still be producing if the price is: Price and Cost $5 $4 a. anywhere below $5. b. below $5 but above $4. C. anywhere above $4. d. below $4. e. above $5. MC AVC Quantity ATC 16. Which of the following would not help identify market structure? a. number of firms in the industry b. type of product produced in the industry c. ease of entry into the industry d. forms of competition among firms in the industry e. price of the good 17. Perfectly competitive firms are price takers because a. b. c. d. e. all small firms must take the price set by the largest firm in the market firms take the price that government determines is a "fair" price each firm is small and goods are perfect substitutes for one another free entry and exit in the short run creates a constant market price in the long run high barriers to entry force firms to compete by charging lower prices than other firms in the industry 18. The demand curve for the output of a perfectly competitive firm is a. perfectly inelastic b. perfectly elastic c. unit elastic d. downward sloping e. nonlinear 19. For perfectly competitive firms, what is the relationship among market price (P), average revenue (AR), and marginal revenue (MR)? a. P = AR = MR C. d. e. b. P> AR = MR P = AR > MR P= AR<MR P<AR=MR 20. If a perfectly competitive firm is incurring a short-run loss, it a. then will incur a long-run loss b. will shut down c. will continue to operate in the short run if its fixed cost is covered d. will continue to operate in the short run if its variable cost is covered e. will raise its price in the short run 21. Long-run equilibrium for a perfectly competitive firm occurs when P = MC=MR = ATC â. b. MCMR = AFC = ATC C. MC MR P> ATC d. P> MC> MR > ATC e. TR> TC 22. Allocative efficiency occurs in markets when a. marginal benefit and marginal cost for the last unit sold are equal b. resources can be reallocated to increase the value of total output c. goods are produced at the minimum of average total cost d. goods are distributed evenly among consumers e. government establishes price ceilings below the market price 23. The term productive efficiency refers to a. any short-run equilibrium position of the competitive firm b. the production of all goods and services that consumers need c. the production of a good at the lowest long-run average cost d. the equality between average total and average variable cost satisfying the condition that MR = MC e. 24. Social welfare is a. a government program through which society takes care of low-income people the overall well-being of people in the economy b. c. measured by spending on party supplies, restaurant meals, and movie tickets d. e. All the answers are correct. applies to sociology, not economics 25. The market for watches is perfectly competitive and is currently in equilibrium. What will happen if watches become more popular among college students? a. In the short run, firms will experience economic profits, but in the long run, firms will leave the market, bringing economic profits back down to zero. b. In the short run, firms will experience economic profits, but in the long run, firms will enter the market, bringing economic profits back down to zero. c. In the short run, firms will incur economic losses, but in the long run, firms will leave the market, bringing economic profits back down to zero. d. In the short run, firms will incur economic losses, but in the long run, firms will enter the market, bringing economic profits back down to zero. In both the short run and the long run, firms will experience zero economic profits. e. 26. Consumer surplus is defined as the: a. difference between the willingness to pay for a good and the willingness to sell it. total revenue earned from producing and selling some good. b. C. difference between the willingness to pay for a good and the price paid to get it. quantity of units that consumers want to buy at the market price. d. e. difference between the price the seller receives and the willingness to sell it. 27. Producer surplus is defined as the: b. a. difference between the willingness to pay for a good and the willingness to sell it. difference between the price the seller receives and the willingness to sell it. difference between the willingness to pay for a good and the price paid to get it. d. quantity of units that consumers want to buy at the market price. c. e. total revenue earned from producing and selling some good. Use the following information to answer the questions that follow. The following graph depicts a market where a tax has been imposed. P, was the equilibrium price before the tax was imposed, and Qe was the equilibrium quantity. After the tax, Pe is the price that consumers pay, and Ps is the price that producers receive. Qr units are sold after the tax is imposed. NOTE: The areas B and C are rectangles that are divided by the supply curve Sr. Include both sections of those rectangles when choosing your answers. A B X C P₂ E 0" 28. Which areas represent consumer surplus before the tax is imposed? a. A+B+F b. A C. C+G+E d. B+C e. F+G ST 29. What areas represent the deadweight loss created as a result of the tax? a. A+B+C+E+F+G b. A+C C. A+B+C+E d. F+G e. B+C+F+G 30. Which of the following is true of monopoly? a. There are no barriers to entry. b. The firm is a price taker. c. There are no close substitutes for the product being produced. There are many firms in the industry. d. e. The firm faces a horizontal demand curve. 31. Patent laws promote technical progress in all of the following ways except one. Which is the exception? a. They allow other firms to copy successful products as soon as they are marketed. b. They prevent duplication of inventions. c. They provide a stimulus to innovation. d. They provide the inventor with a temporary monopoly. e. They increase a firm's incentive to incur the up-front costs of developing new products. 32. The demand curve a monopolist uses in making an output decision is a. the same as the demand curve facing a perfectly competitive firm vertical because there are no close substitutes for its product c. horizontal because there are no close substitutes for its product b. the same as the market demand curve d. e. perfectly inelastic Exhibit 9-3 $/Q $30 24 NNN ONA 10 ill 111 MR 50 100 150 200 117 MC a. b. 150 and $22 c. 150 and $14 d. 117 and $22 e. 117 and $24 117 and $14 ATC AVC 33. The profit-maximizing output and price for the firm in Exhibit 9-3, which charges the same price to all customers, are D 34. A profit-maximizing monopolist produces a quantity at which a. marginal revenue is the greatest distance from marginal cost b. price is less than marginal cost c. the value to society of the last unit produced equals marginal cost d. e. marginal revenue equals marginal cost consumers wish to purchase less than what is produced because of high monopoly prices 35. Barriers to entry a. prevent monopolies from earning profit in the long run b. prevent monopolies from earning profit in the short run may allow monopolies to earn profit in the long run d. prevent government from regulating a monopoly e. prevent a natural monopoly from raising its price C. 36. Which of the following would not be considered price discrimination? a. Long distance telephone rates are cheaper late at night. b. Airline fares are cheaper if you reserve several weeks in advance. The price of lettuce is 59 cents a head and two for a dollar. c. d. The price of a brand-name prescription drug is higher than the price of a generic brand. e. Senior citizens pay less for a movie. 37. Three natural barriers to entry in Monopolies are: a. control of resources, economies of scale, and licensing. b. economies of scale, problems raising capital, and control of resources. c. problems raising capital, patents and copyright law, and licensing. d. control of resources, patents and copyright law, and economies of scale. e. control of resources, economies of scale, and licensing. 38. Two government-created barriers to entry in Monopolies are: licensing and economies of scale. a. b. c. d. e. licensing and control of resources. economies of scale and patent system/copyright law. licensing and patent system/copyright law. economies of scale and control of resources. 39. Patents and copyrights can: a. create strong incentives to develop new drugs. b. provide heavy competition in markets. c. never lead to deadweight loss. d. assure firms that their products will make a profit. e. be considered natural barriers. 40. Inefficient output and price, few choices, and rent seeking are all problems associated with: a. externalities. b. competitive markets. c. monopolies. d. scarcity. e. trade. 41. Most economists are against monopolies because: a. monopolists do not maximize profits. b. monopolies produce too much of product. C. monopolies offer more choices than are needed. d. monopolies can never produce the quantity that a perfectly competitive market would produce. e. monopolies do not offer any choice. 42. Monopolistic competition is best described as a. many firms with some control over price, and some product differentiation b. many firms with no control over price, producing identical products c. a few firms with some control over price, producing highly differentiated products d. a few firms with no control over price, producing similar products e. a single firm producing all of the output for the industry, with strong control over price 43. A firm could differentiate its product by all of the following means except one. Which is the exception? a. making the product available at a number of different locations increasing the number of services that accompany the product b. c. making the product physically different from other products d. using packaging or advertising to create a special subjective image of the product in the consumer's mind e. emphasizing that the product provides the same benefits to consumers as the others on the market, even when it is really physically different 44. When firms differentiate their products, they a. provide information to consumers with no additional use of productive resources always increase their profits b. c. always create real differences among products d. frequently create artificial or superficial differences among products, thus raising production costs e. usually strain the physical capacity of their plants 45. Monopolistic competition is similar to a. perfect competition because the firms face downward-sloping demand curves and can earn only a normal profit in the long run b. pure monopoly because the firms face downward-sloping demand curves and a zero profit in the long run c. perfect competition because the firms face downward-sloping demand curves and similar to pure monopoly in that the firms can earn zero profit in the long run d. pure monopoly because the firms face downward-sloping demand curves and similar to perfect competition in that the firms can earn only a normal profit in the long run e. pure monopoly because the firms face downward-sloping demand curves and can earn an economic profit in the long run 46. One difference between perfect competition and monopolistic competition is that in perfect competition, firms cannot earn a long-run economic profit in perfect competition, firms take full advantage of economies of scale in long-run equilibrium; in monopolistic competition, firms do not a. b. c. only under perfect competition is there ease of entry and exit d. in monopolistic competition, the firm's demand curve is horizontal; in perfect competition, the firm's demand curve slopes downward e. in perfect competition, there are many firms; under monopolistic competition, there are few firms 47. Which of the following is unique to oligopoly among all the market structures? a. product differentiation b. profit maximization c. mutual interdependence d. advertising e. long-run economic profits 48. For firms in an oligopoly to be interdependent, goods must be undifferentiated goods must be differentiated firms must be small a. b. c. d. barriers to entry must be minimal e. goods can be either homogenous or differentiated 49. Which of the following is not an example of an oligopolistic barrier to entry? a. diseconomies of scale b. legal restrictions c. advertising and brand proliferation d. e. 50. Collusion occurs when a. b. a firm chooses a level of output to maximize its own profit firms get together to maximize joint profits C. firms refuse to follow their price leaders d. firms petition their U.S. senators for favors e. two firms' price and output decisions come into conflict high start-up costs control over an essential resource 51. Each member of a cartel a. faces a temptation to cheat on the agreement because lowering its price slightly below the established price will usually increase the firm's sales and profit b. faces a temptation to cheat on the agreement because raising its price slightly above the established price will usually increase the firm's sales and profit has no temptation to cheat on the agreement because lowering its price slightly below the established price will usually have no impact on the firm's sales and profit C. d. has no temptation to cheat on the agreement because raising its price slightly above the established price will usually decrease the firm's sales and profit e. has no temptation to cheat on the agreement because lowering its price slightly below the established price will usually lower the firm's sales and profit 52. In the game theory model of oligopoly, a. firms will be successful in colluding to raise prices b. one firm raises its prices, and other firms follow suit C. firms will match other firms' price cuts but not their price increases d. firms may attempt to avoid the worst outcome but may achieve a less-than-optimal outcome firms never avoid the worst outcome e. 53. A prisoner's dilemma can be described as a situation in which a. a decision maker is uncertain about the potential punishment for something done in the past b. an individual decision maker finds it in his best interest to pursue a course of action that can lead to a less than desirable outcome for the group c. d. e. 54. The payoff matrix refers to a. the difference between total revenue and total cost at different price levels b. a listing of the rewards and penalties associated with pursuing various strategies C. the difference between average and marginal cost for the non-competitive firm d. the difference between average and marginal revenue in a non-competitive industry e. the difference between average variable and average total cost to the firm producers act so as to avoid maximizing profits because of government retaliation individual firms seeks to maximize their own profits with no regard for the group the summation of individual demand curves creates an inelastic demand curve facing the industry 55. If the leading canned soup company introduces dozens of new flavors in order to dominate shelf space, the company is most likely trying to create a barrier to entry by a. increasing the total investment needed to reach the minimum efficient size b. spending more on advertising than potential competitors can afford c. exploiting economies of scale d. crowding out the competition e. establishing an undifferentiated oligopoly 56. Refer to the accompanying table. If Jeff confesses, Gerry will spend confesses and years in jail if he keeps quiet. Jeff a. b. 15; 15 35; 35: C. 0; 35 d. 35; 0 C. Confess Keep quiet 35 years in jail 15; 35 Confess 15 years in jail Gerry 15 years in jail Goes free Goes free Keep quiet 2 years in jail 35 years in jail 2 years in jail years in jail if he also 57. The accompanying table shows two firms in a duopoly. Each firm makes its decision without knowledge of the other firm's decision. The payoffs for each firm represent economic profits, and each firm strictly prefers more economic profit than less. If both firms were able to collude and make their supply decisions collectively, Flixbuster would sell subscriptions per month and Nextflix would sell subscriptions per month. Nextflix a. b. C. d. e. Sell 200 subscriptions $750,000 per month Sell 400 subscriptions $950,000 per month 200; 200 400; 400 Sell 200 subscriptions per month 400; 200 200; 400 600; 600 Flixbuster $750,000 $400,000 Sell 400 subscriptions per month $400,000 $600,000 $950,000 $600,000

Expert Answer:

Answer rating: 100% (QA)

The detailed answer for the above question is provided below 1 b sales taxes 2 c opportunity costs of capital owned and used by the firm 3 a total revenue minus implicit costs 4 C the increase in outp... View the full answer

Related Book For

Posted Date:

Students also viewed these economics questions

-

Question 1 Find the volume of the solid generated by revolving the region bounded by the graphs of the equations y-6-z V=0 around the x-axis. -12.7246 Question 2 A region, R, is bouned by the curves...

-

My employee seems to leave work anytime between 5PM and 6PM, uniformly. a) What is the probability he will still be at work at 5:45 PM? b) What is the probability he will still be at work at 5:45 PM...

-

Some companies have very narrow product mixes, producing just one or two products, while others have many different products. What are the advantages of each approach?

-

You are the cashier employed at Tastee Limited. On November 30, 2020, you started with a float of $6,500 and at the end of the business day your cash in the cash till were as follows: Notes Coins...

-

During the year, the following sales transactions occur. There is a charge of 3% on all credit card transactions and a 1% charge on all debit card transactions. Calculate the amount recorded as cash...

-

Friendly Ice Cream Corporation operates and franchises full-service restaurants from Maine to South Carolina. The company also manufactures the ice cream that is served in its restaurants and sold in...

-

Based on the following pedigree for a trait determined by a single gene (affected individuals are shown as filled symbols), state whether it would be possible for the trait to be inherited in each of...

-

Guillen, Inc. began work on a $7,000,000 contract in 2012 to construct an office building. Guillen uses the completed-contract method. At December 31, 2012, the balances in certain accounts were...

-

Suppose you have 135 households in your neighborhood, can you use "=RAND()" function in Excel to randomly select 20 of them to send a survey? a) Write down the codes you would use. b) Show your work...

-

Oasis Co., a U.S. shareholder, owns 100% of Shack Co. and 100% of Studio Co., both CFCs. Shack Co. has $300,000 of gross income, of which $50,000 is effectively connected income, and $30,000 is...

-

What is globalization, and how does it affect different countries? Explain and provide examples

-

Question 4 Recent information on the earnings per share and share price of Par Co is as follows: Year Earnings per share (cents) Year-end share price ($) 2011 2012 2013 2014 64 68 70 62 9-15 9.88...

-

In the article by O'hara they raise a number of salient points about negotiating with someone more powerful. Which points resonated with you most strongly and why? O'Hara, C. "How to Negotiate With...

-

Calculatethe NPV (assume 1Jan22) of the projected FCFs (2022e-2025e) of Company XYZ with a WACC ranging from 8% to 14%. Use the following data: Company XYZ

-

Pick ONE of the compare/contrast choices (a, b, or c). a. Compare and contrast these concepts: Team Role Clarity and Role Acceptance b. Compare and contrast these concepts: Team Cohesion and...

-

Neil took a poll of people in Noda, asking them if they would prefer eating at Sabor or Cabo Fish Taco. He took the poll during the week, by asking people who found outside, during his working hours....

-

In a group of 12 horses, some are 9 years old and the remainder are 11 years old. The total of their ages is 122. How many horses are 9 years old?

-

l ask this second time correnct answer is 38,01 can we look pls Consider a non-conducting rod of length 8.8 m having a uniform charge density 4.5 nC/m. Find the electric potential at P, a...

-

1. Horizontal analysis of accounts receivable: a. calculates accounts receivable as a percentage of total assets. b. highlights the change in accounts receivable as a percentage of the prior year's...

-

Lowder Company purchased 275 units of inventory on account for $5,775. Due to some defects in the merchandise, Lowder received a $2 per unit allowance and paid only $5,225. Lowder then sold 150 units...

-

Describe the two methods for reporting operating cash flows. Do they result in the same amount? Which one is used by most companies?

-

Fiscal policy can make the central banks job impossible because: a. Politicians tend to take a short-term view, encouraging doubt about the commitment to price stability or financial stability. b. In...

-

The best central banks: a. Are independent of political pressure. b. Are accountable to elected representatives and the public. c. Communicate their objectives, actions, and policy deliberations...

-

Assess the effectiveness of the Federal Reserve System.

Study smarter with the SolutionInn App