Question: No information on volatility, just the above information = = = Consider a binomial model with T 2 periods, S 100, u = 1.6 and

No information on volatility, just the above information

No information on volatility, just the above information

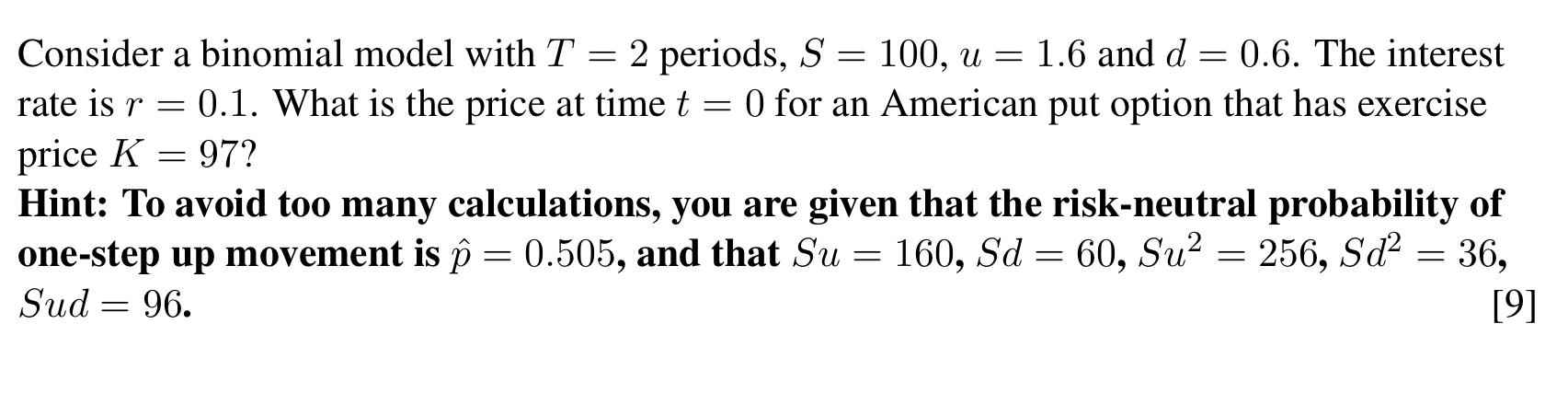

= = = Consider a binomial model with T 2 periods, S 100, u = 1.6 and d 0.6. The interest rate is r = 0.1. What is the price at time t = 0 for an American put option that has exercise price K = 97? Hint: To avoid too many calculations, you are given that the risk-neutral probability of one-step up movement is p = 0.505, and that Su= 160, Sd = 60, Su2 = 256, Sd2 = 36, Sud = 96. [9]

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock