Question: NOEN 6. Problem 8.07 (Portfolio Required Return) eBook H1 Problem Walk-Through Suppose you are the money manager of a $4.64 million investment fund. The fund

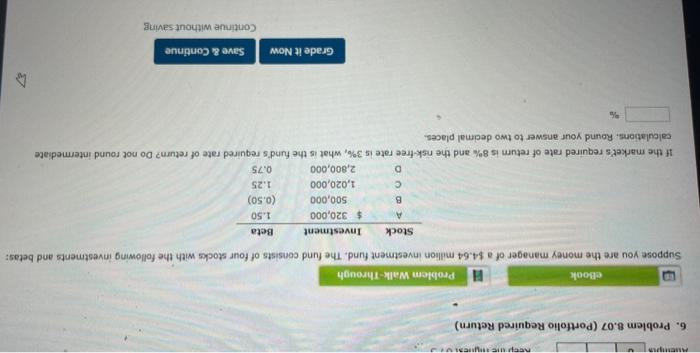

NOEN 6. Problem 8.07 (Portfolio Required Return) eBook H1 Problem Walk-Through Suppose you are the money manager of a $4.64 million investment fund. The fund consists of four stocks with the following investments and betas: Stock Investment Beta A $ 320,000 1.50 B 500,000 (0.50) 1,020,000 1.25 D 2,800,000 0.75 If the market's required rate of return is 8% and the risk-free rate is 3%, what is the fund's required rate of return? Do not round intermediate calculations. Round your answer to two decimal places. 3 Grade it Now Save & Continue Continue without saving

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock