Question: not sure how to do the math for this question. can u. clearly write how to solve. step by step Suppooe Avon and Wova stocks

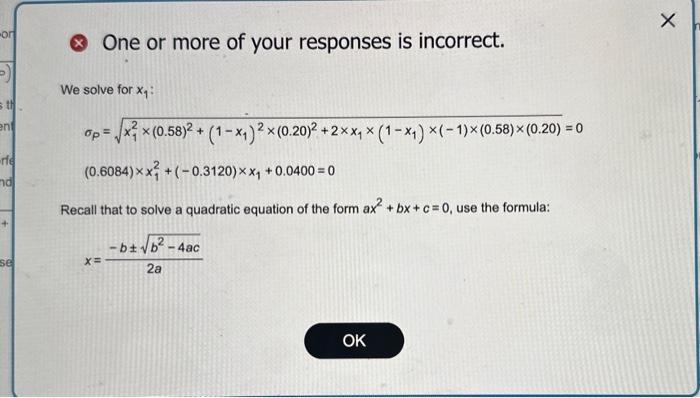

Suppooe Avon and Wova stocks have volatities of 45% and 28%, Respectwely, and they are perfectly nepatvely ooselated. What portbolo of these tao stocks has zero risk? The portfoles of fiese two stacki that has zero hak is No d Avon and Sof Nova. (Round to two deainal places.) * One or more of your responses is incorrect. We solve for x1 : p=x12(0.58)2+(1x1)2(0.20)2+2x1(1x1)(1)(0.58)(0.20)=0(0.6084)x12+(0.3120)x1+0.0400=0 Recall that to solve a quadratic equation of the form ax2+bx+c=0, use the formula: x=2abb24ac Suppooe Avon and Wova stocks have volatities of 45% and 28%, Respectwely, and they are perfectly nepatvely ooselated. What portbolo of these tao stocks has zero risk? The portfoles of fiese two stacki that has zero hak is No d Avon and Sof Nova. (Round to two deainal places.) * One or more of your responses is incorrect. We solve for x1 : p=x12(0.58)2+(1x1)2(0.20)2+2x1(1x1)(1)(0.58)(0.20)=0(0.6084)x12+(0.3120)x1+0.0400=0 Recall that to solve a quadratic equation of the form ax2+bx+c=0, use the formula: x=2abb24ac

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts