Question: Not understanding the explanation to the answer given in the problem. Did they solve for beta then use CapM? It's unclear to me what they

Not understanding the explanation to the answer given in the problem. Did they solve for beta then use CapM? It's unclear to me what they have done to solve for Y. Please provide detailed explanation.

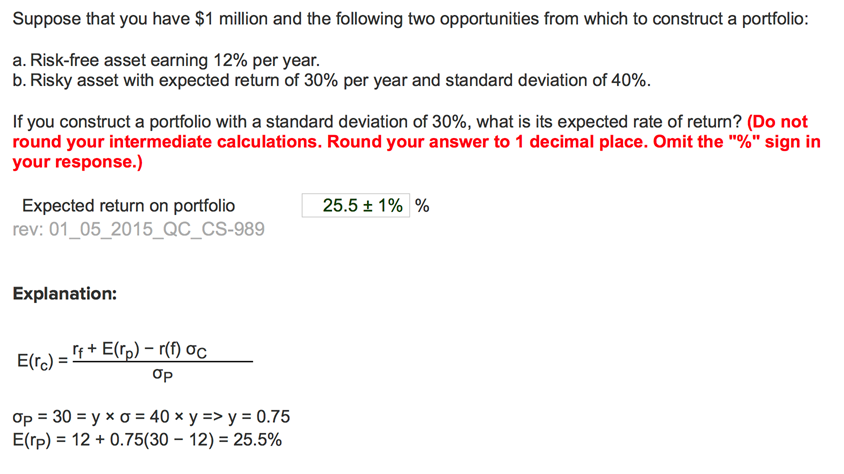

Suppose that you have $1 million and the following two opportunities from which to construct a portfolio: a. Risk-free asset earning 12% per year b. Risky asset with expected return of 30% per year and standard deviation of 40%. If you construct a portfolio with a standard deviation of 30%, what is its expected rate of retum? (Do not round your intermediate calculations. Round your answer to 1 decimal place. Omit the "%" sign in your response.) 25.5 1% % Expected return on portfolio rev: 0105 2015 QC_CS-989 Explanation: E(r)-12 + 0.75(30-12)-25.5%

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts