Question: Note 15 below outlines further information about the fair valuing of these biological assets. From your perspective as a potential equity investor, explain the disadvantages

Note 15 below outlines further information about the fair valuing of these biological assets. From your perspective as a potential equity investor, explain the disadvantages of the accounting treatment of the aquaculture of salmon and how you might adjust for them in your analysis of NZ King Salmon using a valuation model (i.e. a discounted cash flow or NPV)

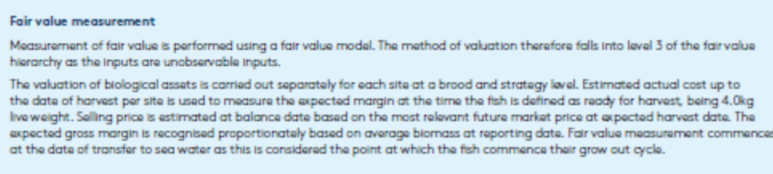

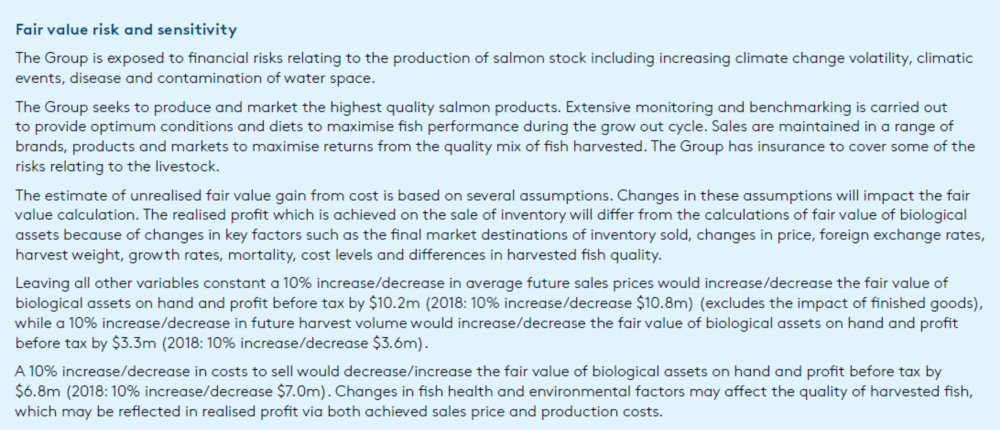

Fair value measurement Measurement of fair value is performed using a fair value model. The method of valuation therafora falls into laval 3 of the fair value hierarchy as the inputs are unobservable inputs. The valuation of biological assets is carried out separately for each site at a brood and strategy loval. Estimated actual cost up to the date of harvest per site is used to measure the expected margin at the time the fish is defined as ready for harvest, being 4.0kg live weight. Selling price is estimated at balance date based on the most relevant future market price at expected harvest date. The expected gross margin is recognised proportionataly based on average biomass at raporting data. Fair value measurement commence at the data of transfer to sea water as this is considerad the point at which the fish commence their grow out cycle. Fair value risk and sensitivity The Group is exposed to financial risks relating to the production of salmon stock including increasing climate change volatility, climatic events, disease and contamination of water space. The Group seeks to produce and market the highest quality salmon products. Extensive monitoring and benchmarking is carried out to provide optimum conditions and diets to maximise fish performance during the grow out cycle. Sales are maintained in a range of brands, products and markets to maximise returns from the quality mix of fish harvested. The Group has insurance to cover some of the risks relating to the livestock. The estimate of unrealised fair value gain from cost is based on several assumptions. Changes in these assumptions will impact the fair value calculation. The realised profit which is achieved on the sale of inventory will differ from the calculations of fair value of biological assets because of changes in key factors such as the final market destinations of inventory sold, changes in price, foreign exchange rates, harvest weight, growth rates, mortality, cost levels and differences in harvested fish quality. Leaving all other variables constant a 10% increase/decrease in average future sales prices would increase/decrease the fair value of biological assets on hand and profit before tax by $10.2m (2018: 10% increase/decrease $10.8m) (excludes the impact of finished goods), while a 10% increase/decrease in future harvest volume would increase/decrease the fair value of biological assets on hand and profit before tax by $3.3m (2018: 10% increase/decrease $3.6m). A 10% increase/decrease in costs to sell would decrease/increase the fair value of biological assets on hand and profit before tax by $6.8m (2018: 10% increase/decrease $7.0m). Changes in fish health and environmental factors may affect the quality of harvested fish, which may be reflected in realised profit via both achieved sales price and production costs. Fair value measurement Measurement of fair value is performed using a fair value model. The method of valuation therafora falls into laval 3 of the fair value hierarchy as the inputs are unobservable inputs. The valuation of biological assets is carried out separately for each site at a brood and strategy loval. Estimated actual cost up to the date of harvest per site is used to measure the expected margin at the time the fish is defined as ready for harvest, being 4.0kg live weight. Selling price is estimated at balance date based on the most relevant future market price at expected harvest date. The expected gross margin is recognised proportionataly based on average biomass at raporting data. Fair value measurement commence at the data of transfer to sea water as this is considerad the point at which the fish commence their grow out cycle. Fair value risk and sensitivity The Group is exposed to financial risks relating to the production of salmon stock including increasing climate change volatility, climatic events, disease and contamination of water space. The Group seeks to produce and market the highest quality salmon products. Extensive monitoring and benchmarking is carried out to provide optimum conditions and diets to maximise fish performance during the grow out cycle. Sales are maintained in a range of brands, products and markets to maximise returns from the quality mix of fish harvested. The Group has insurance to cover some of the risks relating to the livestock. The estimate of unrealised fair value gain from cost is based on several assumptions. Changes in these assumptions will impact the fair value calculation. The realised profit which is achieved on the sale of inventory will differ from the calculations of fair value of biological assets because of changes in key factors such as the final market destinations of inventory sold, changes in price, foreign exchange rates, harvest weight, growth rates, mortality, cost levels and differences in harvested fish quality. Leaving all other variables constant a 10% increase/decrease in average future sales prices would increase/decrease the fair value of biological assets on hand and profit before tax by $10.2m (2018: 10% increase/decrease $10.8m) (excludes the impact of finished goods), while a 10% increase/decrease in future harvest volume would increase/decrease the fair value of biological assets on hand and profit before tax by $3.3m (2018: 10% increase/decrease $3.6m). A 10% increase/decrease in costs to sell would decrease/increase the fair value of biological assets on hand and profit before tax by $6.8m (2018: 10% increase/decrease $7.0m). Changes in fish health and environmental factors may affect the quality of harvested fish, which may be reflected in realised profit via both achieved sales price and production costs

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts