Question: Note: Assume that you have return and factor data, and you estimate mu_j and beta_j for j=1,2. For part a., construct the portfolio that eliminates

Note: Assume that you have return and factor data, and you estimate mu_j and beta_j for j=1,2. For part a., construct the portfolio that eliminates beta risk using the data and estimates. Then for part b., use your solution from part a. to show that the riskless portfolio must have expected return r_f, and solve for lambda given mu_j, r_f, and beta_j for any asset j.

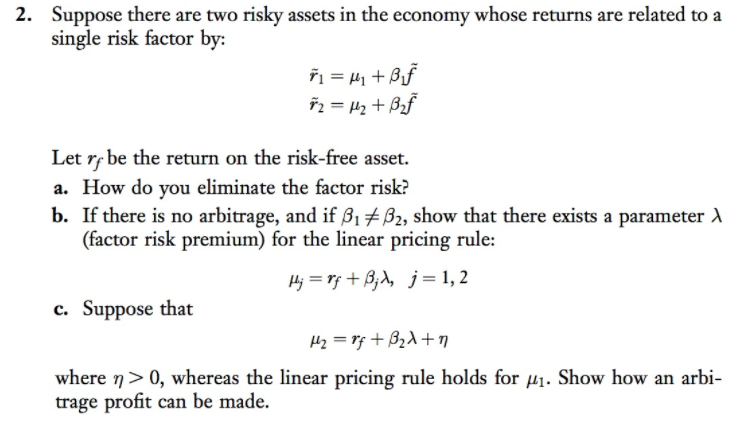

2. Suppose there are two risky assets in the economy whose returns are related to a ngle risk factor by: Let rf be the return on the risk-free asset. a. How do you eliminate the factor risk? b. If there is no arbitrage, and if -A, show that there exists a parameter (factor risk premium) for the linear pricing rule: c. Suppose that where > 0, whereas the linear pricing rule holds for 1-Show how an arbi- trage profit can be made. 2. Suppose there are two risky assets in the economy whose returns are related to a ngle risk factor by: Let rf be the return on the risk-free asset. a. How do you eliminate the factor risk? b. If there is no arbitrage, and if -A, show that there exists a parameter (factor risk premium) for the linear pricing rule: c. Suppose that where > 0, whereas the linear pricing rule holds for 1-Show how an arbi- trage profit can be made

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts