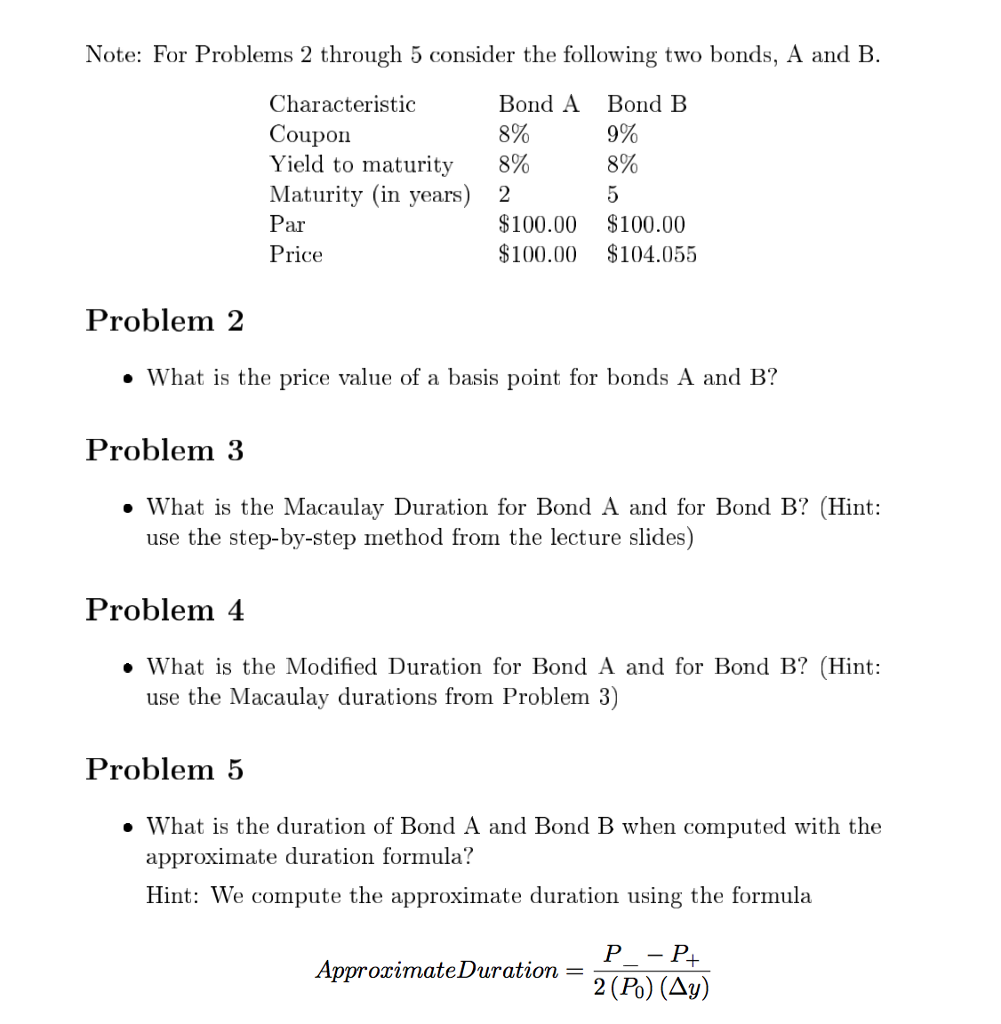

Question: Note: For Problems 2 through 5 consider the following two bonds, A and B Characteristic Coupon Yield to maturity 8% Maturity (in years) 2 Bond

Note: For Problems 2 through 5 consider the following two bonds, A and B Characteristic Coupon Yield to maturity 8% Maturity (in years) 2 Bond A 8% Bond B 9% 8% $100.00 $100.00 $100.00 $104.055 ar Price Problem 2 . What is the price value of a basis point for bonds A and B? Problem 3 . What is the Macaulay Duration for Bond A and for Bond B? (Hint: use the step-by-step method from the lecture slides) Problem 4 What is the Modified Duration for Bond A and for Bond B? (Hint: use the Macaulay durations from Problem 3) Problem 5 What is the duration of Bond A and Bond B when computed with the approximate duration formula? Hint: We compute the approximate duration using the formula P -P ApproximateDuration - 2(Po)(y)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts