Question: Notice: The first question is calculate modified duration, not effective duration. 2. The Hospital Pension Fund contains noncallable US Treasuries shown in the table below.

Notice: The first question is calculate modified duration, not effective duration.

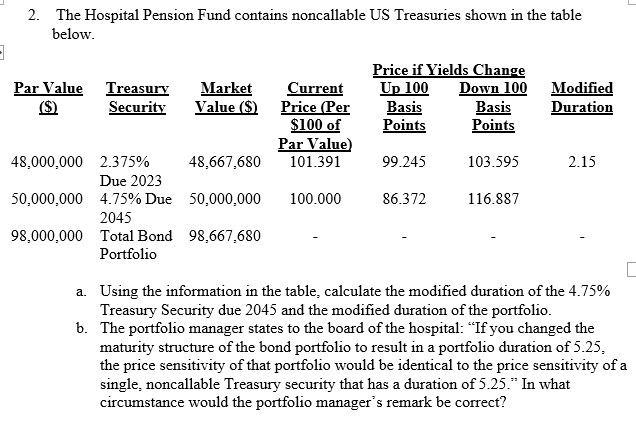

2. The Hospital Pension Fund contains noncallable US Treasuries shown in the table below. Price if Yields Change Up 100 Down 100 Modified Basis Basis Duration Points Points 99.245 Par Value Treasury Market Current ($) Security Value ($) Price (Per $100 of Par Value) 48,000,000 2.375% 48,667,680 101.391 Due 2023 50.000.000 4.75% Due 50,000,000 100.000 2045 98.000.000 Total Bond 98.667.680 Portfolio 103.595 2.15 86.372 116.887 a. Using the information in the table, calculate the modified duration of the 4.75% Treasury Security due 2045 and the modified duration of the portfolio. b. The portfolio manager states to the board of the hospital: If you changed the maturity structure of the bond portfolio to result in a portfolio duration of 5.25, the price sensitivity of that portfolio would be identical to the price sensitivity of a single, noncallable Treasury security that has a duration of 5.25." In what circumstance would the portfolio manager's remark be correct

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts