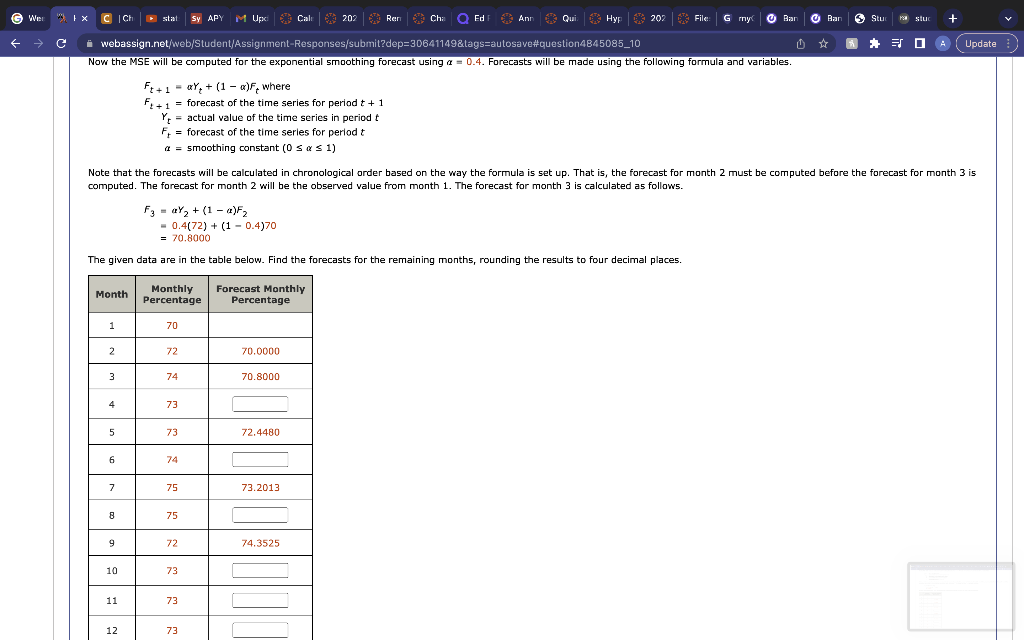

Question: Now the MSE will be computed for the exponential smoothing forecast using =0.4. Forecasts will be made using the following formula and variables. Ft+1Ft+1YtFt=Yt+(1)Ftwhere=forecastofthetimeseriesforperiodt+1=actualvalueofthetimeseriesinperiodt=forecastofthetimeseriesforperiodt=smoothingconstant(01) computed.

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock