Question: Now you try one: Nvidia ( NVDA ) and Super Micro Computer ( SMCI ) Calculate the 9 9 % , 1 0 - day

Now you try one: Nvidia NVDA and Super Micro Computer SMCI

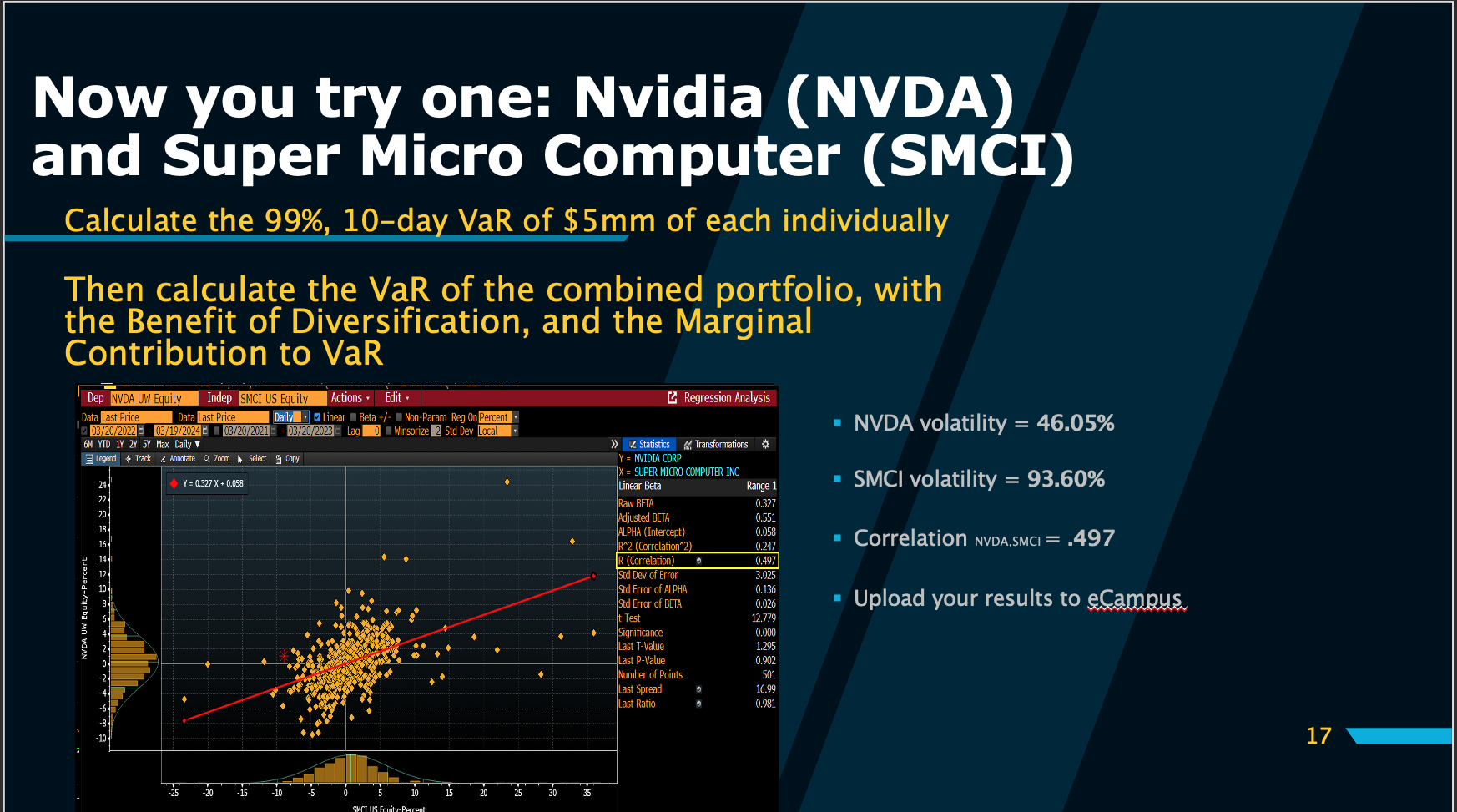

Calculate the day VaR of $ of each individually

Then calculate the VaR of the combined portfolio, with the Benefit of Diversification, and the Marginal Contribution to VaR

NVDA volatility

SMCI volatility

Correlation NVDA,SMCI

Steps done in excel!!!!

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock