Question: Old MathJax webview I will vote your Answer Definitely please give me Right answer of my question do next one Table 16.6 Minitab Calculations for

Old MathJax webview

I will vote your Answer Definitely please give me Right answer of my question

do next one

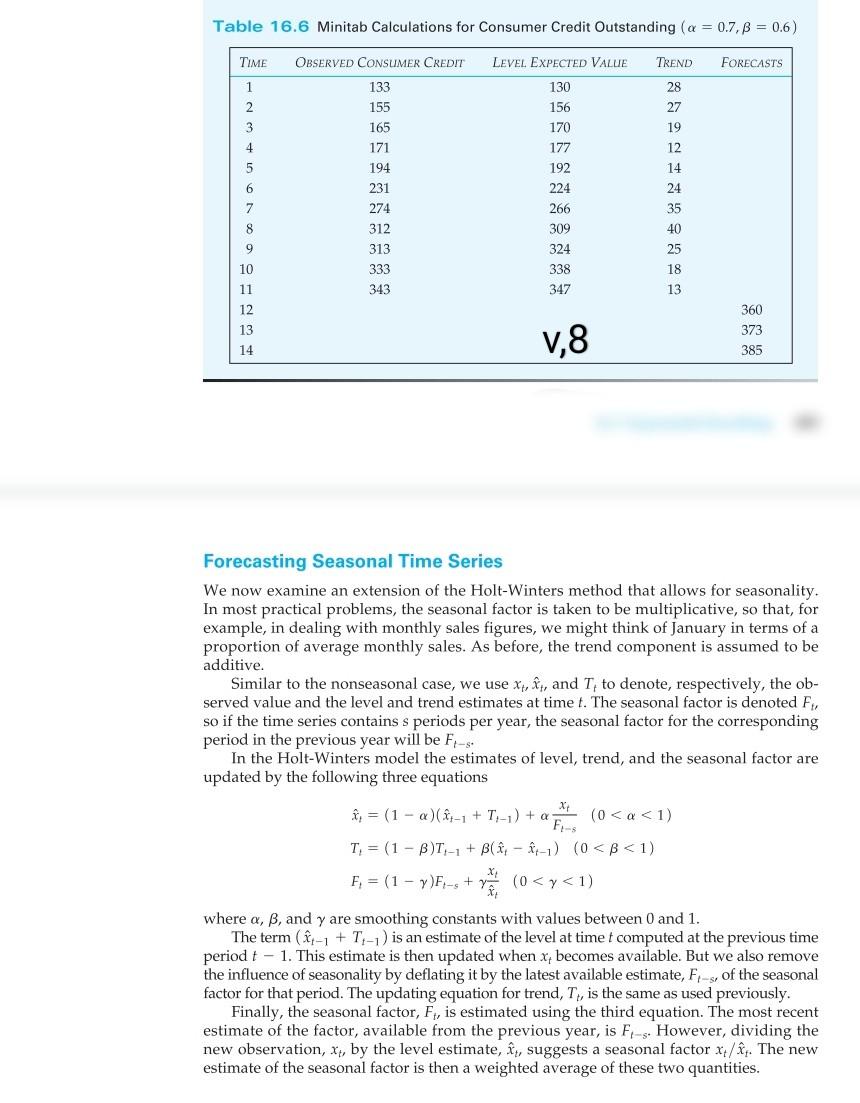

Table 16.6 Minitab Calculations for Consumer Credit Outstanding (a = 0.7,6 = 0.6) TIME OBSERVED CONSUMER CREDIT LEVEL EXPECTED VALUE TREND FORECASTS 1 133 130 28 2 155 156 27 3 165 170 19 4 171 177 12 5 194 192 14 6 231 224 24 274 266 35 8 312 309 40 9 313 324 25 10 333 338 18 11 343 347 13 12 360 13 373 1,8 14 385 Forecasting Seasonal Time Series We now examine an extension of the Holt-Winters method that allows for seasonality. In most practical problems, the seasonal factor is taken to be multiplicative, so that, for example, in dealing with monthly sales figures, we might think of January in terms of a proportion of average monthly sales. As before, the trend component is assumed to be additive. Similar to the nonseasonal case, we use xt, t, and T, to denote, respectively, the ob- served value and the level and trend estimates at time t. The seasonal factor is denoted F, so if the time series contains s periods per year, the seasonal factor for the corresponding period in the previous year will be F,-s. In the Holt-Winters model the estimates of level, trend, and the seasonal factor are updated by the following three equations , = (1 - a-1 + 1,-1) + a F (0Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock