Question: Old MathJax webview It's complete question You enter into the following option positions with firm ABC Inc, which expire in one year : (i) Buy

Old MathJax webview

It's complete question

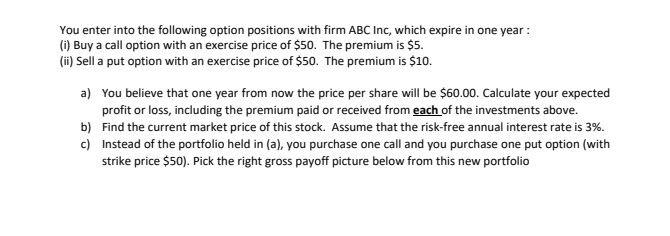

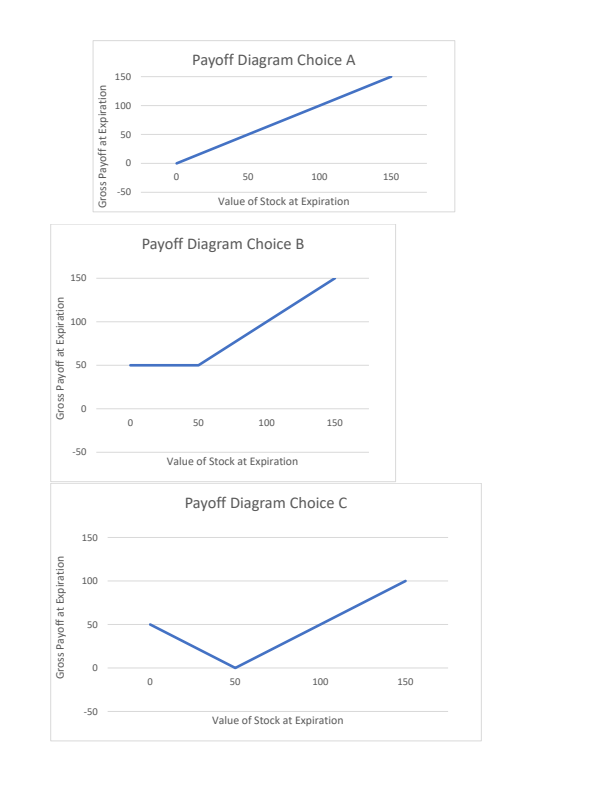

You enter into the following option positions with firm ABC Inc, which expire in one year : (i) Buy a call option with an exercise price of $50. The premium is $5. (i) Sell a put option with an exercise price of $50. The premium is $10. a) You believe that one year from now the price per share will be $60.00. Calculate your expected profit or loss, including the premium paid or received from each of the investments above. b) Find the current market price of this stock. Assume that the risk-free annual interest rate is 3%. c) Instead of the portfolio held in (a), you purchase one call and you purchase one put option (with strike price $50). Pick the right gross payoff picture below from this new portfolio Payoff Diagram Choice A 150 100 50 Gross Payoff at Expiration 50 100 150 -50 Value of Stock at Expiration Payoff Diagram Choice B 150 100 Gross Payoff at Expiration 0 50 100 150 -50 Value of Stock at Expiration Payoff Diagram Choice C 150 100 Gross Payoff at Expiration 50 0 50 100 150 -50 Value of Stock at Expiration Payoff Diagram Choice D 150 100 Gross Payoff at Expiration 0 50 100 150 -50 Value of Stock at Expiration Payoff Diagram Choice E 150 100 Gross Payoff at Expiration 0 50 100 150 -50 Value of Stock at Expiration

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts