Question: Old MathJax webview XRX-1 Please do not copy other answers. This is a different question. If copied from other answers I will downvote and report

Old MathJax webview

XRX-1 Please do not copy other answers. This is a different question. If copied from other answers I will downvote and report your account .

Q1.

Q2.

Full information is already provided

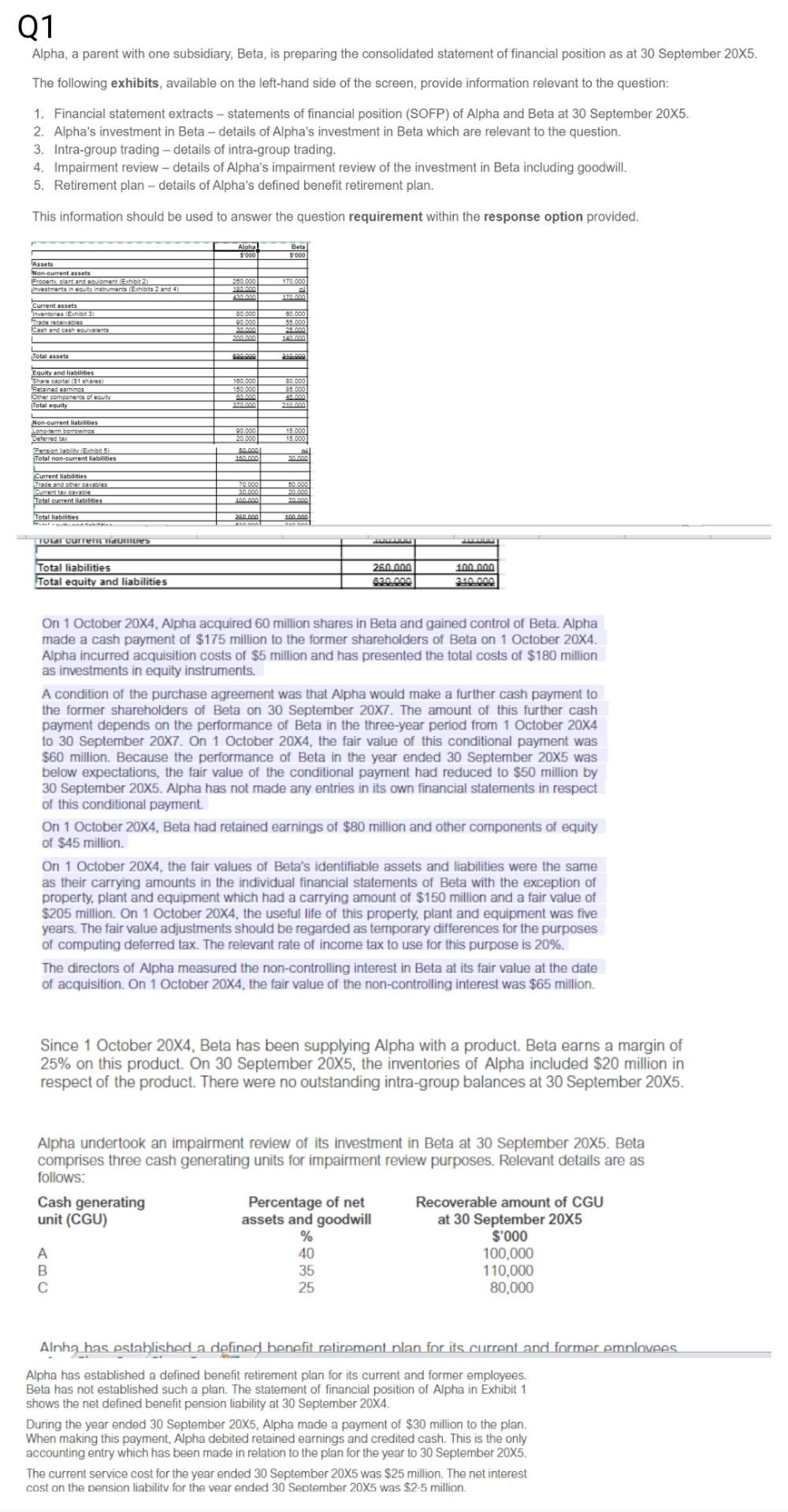

Q1 Alpha, a parent with one subsidiary, Beta, is preparing the consolidated statement of financial position as at 30 September 20X5. The following exhibits, available on the left-hand side of the screen, provide information relevant to the question: 1. Financial statement extracts - statements of financial position (SOFP) of Alpha and Beta at 30 September 20X5. 2. Aipha's investment in Beta - details of Alpha's investment in Beta which are relevant to the question. 3. Intra-group trading - details of intra-group trading. 4. Impairment review - details of Alpha's impairment review of the investment in Beta including goodwill. 5. Retirement plan - details of Alpha's defined benefit retirement plan. This information should be used to answer the question requirement within the response option provided. Alpha 5000 59000 Rssets Non current assets Propertimento investments in our struments Eshots 2 and 259699 SA ERRI Current assets Inventores de les Cash and cash ouivalents Sea EBS 60.000 P2.000 80.000 59.000 2014 Total assets Equity and liabilities Share capital 51 shares stained emines Other components of out Total equity 500.000 80.000 85.000 159099 AMA 212 15 000 Non-current abilities Long-term bow Deferred to Pension Exhibit Total non-current liabilities 00.000 20.000 50.0001 160 Current liabilities Trade andere TO.000 2000 100.000 20.0001 Total current abilities Total liabilities 250.000 at 100.000 TULGI UUTTET TILES Total liabilities Total equity and liabilities 260.000 220.000 100 na 210.000 On 1 October 20X4, Alpha acquired 60 million shares in Beta and gained control of Beta. Alpha made a cash payment of $175 million to the former shareholders of Beta on 1 October 20X4. Alpha incurred acquisition costs of $5 million and has presented the total costs of $180 million as investments in equity instruments. A condition of the purchase agreement was that Alpha would make a further cash payment to the former shareholders of Beta on 30 September 20X7. The amount of this further cash payment depends on the performance of Beta in the three-year period from 1 October 20X4 to 30 September 20X7. On 1 October 20X4, the fair value of this conditional payment was $60 million. Because the performance of Beta in the year ended 30 September 2005 was below expectations, the fair value of the conditional payment had reduced to $50 million by 30 September 20X5. Alpha has not made any entries its own financial statements in respect of this conditional payment. On 1 October 20X4, Beta had retained earnings of $80 million and other components of equity of $45 million. On 1 October 20X4, the fair values of Beta's identifiable assets and liabilities were the same as their carrying amounts in the individual financial statements of Beta with the exception of property, plant and equipment which had a carrying amount of $150 million and a fair value of $205 million. On 1 October 20X4, the useful life of this property, plant and equipment was five years. The fair value adjustments should be regarded as temporary differences for the purposes of computing deferred tax. The relevant rate of income tax to use for this purpose is 20%. The directors of Alpha measured the non-controlling interest in Beta at its fair value at the date of acquisition. On 1 October 20X4, the fair value of the non-controlling interest was $65 million Since 1 October 20X4, Beta has been supplying Alpha with a product. Beta earns a margin of 25% on this product. On 30 September 2005, the inventories of Alpha included $20 million in respect of the product. There were no outstanding intra-group balances at 30 September 20X5. Alpha undertook an impairment review of its investment in Beta at 30 September 2005. Beta comprises three cash generating units for impairment review purposes. Relevant details are as follows: Cash generating Percentage of net Recoverable amount of CGU unit (CGU) assets and goodwill at 30 September 20X5 % $'000 A 40 100,000 B 35 110,000 25 80,000 Alnha has established a defined benefit retirement nlan for its current and former employees Alpha has established a defined benefit retirement plan for its current and former employees. Beta has not established such a plan. The statement of financial position of Alpha in Exhibit 1 shows the net defined benefit pension liability at 30 September 20X4. During the year ended 30 September 20X5, Alpha made a payment of $30 million to the plan. When making this payment, Alpha debited retained earnings and credited cash. This is the only accounting entry which has been made in relation to the plan for the year to 30 September 20X5. The current service cost for the year ended 30 September 20X5 was $25 million. The net interest cost on the pension liability for the vear ended 30 September 20X5 was $2.5 million Using the information in Exhibits 1 - 5, prepare the consolidated statement of financial position of Alpha at 30 September 20X5. Note: Unless specifically referred to in the exhibits you should ignore deferred tax. necessary between 1 October 2012 and 30 June 2018. Note 4 - Intra-group trading Alpha supplies a component to Beta at a mark-up of 25% on its production cost. The trade receivables of Alpha at 30 September 2018 include $10 million receivable from Beta in respect of sales of the component. Beta paid Alpha $10 million to clear the outstanding balance on 29 September 2018. Alpha received and recorded this amount on 3 October 2018. On 30 September 2018, the inventories of Beta included $15 million in respect of components purchased from Alpha. All such inventory is measured at original cost to Beta. Note 5 - Property lease On 1 October 2017, Alpha began to lease a property under a 10-year lease. The annual rate of interest implicit in the lease was 5%. The lease rentals payable by Alpha were $10 million, payable annually in arrears. The lease does not transfer ownership of the property to Alpha at the end of the lease term. The lease contains no option for Alpha to purchase the property at the end of the lease term. On 1 October 2017, Alpha incurred direct costs of $4 million in arranging this lease. The only accounting entries made by Alpha in respect of this lease were to charge $14 million to the statement of profit or loss. Using a discount rate of 5%, the cumulative present value of $1 payable annually in arrears for ten years is $7.72. 5 [P.T.O. Required: (a) Compute the profit or loss on disposal of the investment in Delta which would be shown in the consolidated statement of profit or loss of Alpha for the year ended 30 September 2018 (b) Prepare the consolidated statement of financial position of Alpha at 30 September 2018. You need only consider the deferred tax implications of any adjustments you make where the question specifically refers to deferred tax. Note: You should show all workings to the nearest $'000

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts