Question: Oleo Software* Oleo Software was started in 2006 by two University of Washington graduates, Jim Little, a computer science major who specialized in user interfaces,

Oleo Software*

Oleo Software was started in 2006 by two University of Washington graduates, Jim Little, a computer science major who specialized in user interfaces, and Terry Bena, an economics major who studied optimization techniques.Their initial product, Oleo Professional, was designed for large retailers faced with a variety of optimization decisions regarding their warehouses: Where to locate warehouses, which products to stock in which warehouse, and where to locate products within each warehouse.

When Oleo Software started, Jim and Terry did everything.A typical day would include meetings with current customers (to get a better understanding of customer needs) and potential customers (to generate new business).Long days were followed by long nights of developing and maintaining their software.As the company grew, this approach became unsustainable, as Jim and Terry faced growing demands for customer support, increasingly complex software development issues, and the need to deal with administration of their growing business

In 2009, they added their first administrative assistant as well as a programmer.They also launched a new product line, OleoLite, a lower cost version of their software with fewer features designed to meet the needs of smaller retailers.Over the next several years they continued hiring additional programmers to develop new features for existing products and to help with development of new products. They also added staff to take care of various accounting, clerical, and maintenance issues. As they added additional staff, Jim and Terry were able to devote more of their attention to marketing and strategic planning and less time to programming.

In 2012, they launched two new products for distributors rather than retailers, Distleo for large distributors and a lower cost version for smaller distributors, DistleoLite.To promote their expanded line of products, they hired a vice-president of marketing, who also began to grow the marketing staff.Over the years, they saw substantial growth in overall revenue (see Figure 1 for total revenue by year and Figure 2 for revenue by product line).

By 2014, the rate of revenue growth had slowed and profits began to flatten out. Jim and Terry hired the company's first CFO, Brett Johnson, and explicitly charged him to address concerns about the declining rate of growth in profits. After reviewing results for the most recent years, Johnson saw that the growth of costs had begun to outpace the growth of revenues. Johnson decided to control costs and reverse this trend, noting: "Marketing is already working hard to increase sales, so my job as CFO is to figure out what we can do to lower costs." Johnson thought it might be possible to find ways to reduce expenditures on indirect costs but these costs were not allocated to products in Oleo's existing costing system: "When we had only one product, we didn't have to worry about which products were generating which costs, so we didn't worry about allocating costs. However, now that we are producing four different products, we need to develop a good understanding of the full cost of each product."

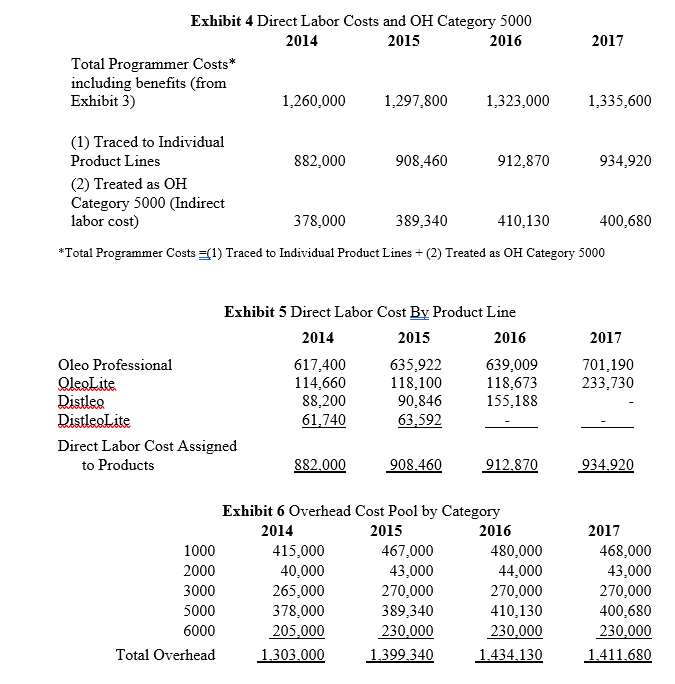

Johnson designed a new costing system to determine the cost (and profitability) of each product line.In this system, the total cost of programmer time spent working on specific products is traced to each product.However, not all programmer time can be traced to individual product lines. For programmer time that relates to development or maintenance of multiple product lines or to development of possible new product lines that have not yet been defined, the cost is recorded in Category 5000 of general overhead. (See Exhibits 2 and 4 for further explanation of salary and benefit costs.)

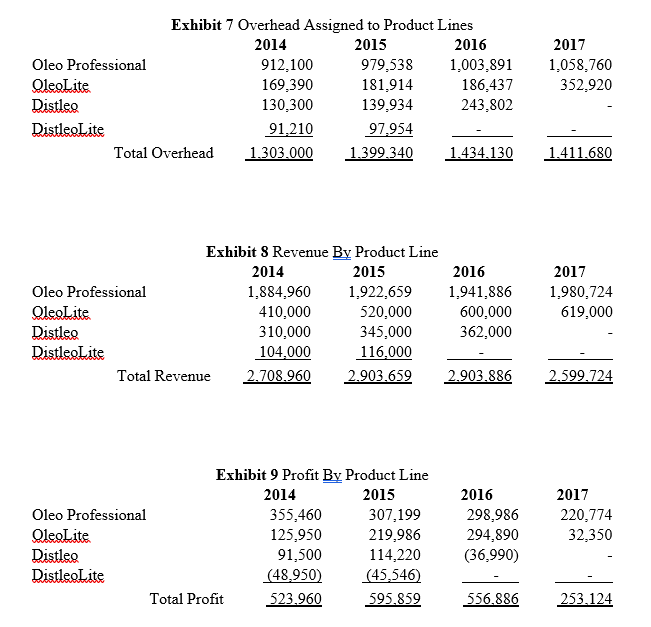

Overhead is allocated to product lines using direct labor costs as the allocation base (see Exhibit 5 for the direct labor costs used to do this allocation and Exhibit 7 to see the result of the allocation).As summarized in Exhibit 2 and shown in detail in Exhibit 6, all costs other than direct labor costs are included in the overhead cost pool, including

-costs of personnel that perform accounting, clerical, and maintenance functions

-materials, supplies, and miscellaneous costs

-cost of leasing the facilities and equipment used by Oleo

-salaries and benefits for indirect labor costs

-salaries for Jim and Terry.[1]

The results from applying the new system to 2014 and 2015 were an eye-opener for Oleo management.They saw that one of their newer products, DistleoLite, was unprofitable, even though sales had been increasing.Everyone agreed that the best way to get back on a path to growth in profitability was to drop the unprofitable DistleoLite line as of the end of 2015.

Unfortunately, results for 2016 were even more disappointing.Although sales for each of the three products that had been retained grew, total revenue was basically flat.More importantly, even though the unprofitable DisteoLite product had been dropped, profits didn't improve.Instead, profits actually decreased substantially. Further, now Distleo was no longer profitable.Everyone still agreed that it was important to discontinue products that were losing money, so the decision was made to drop Distleo as of the end of 2016.

Jim and Terry have just received the results for 2017, shown in the attached figures and graphs.They have two major concerns:First, although sales have increased for each of the two remaining products, overall revenue and profitability have again declined - in fact profits dropped in half!Second, profitability of OleoLite has declined and is now only about 10% of what it had been in 2016.Jim and Terry are worried that it won't be long before OleoLite becomes unprofitable so they are considering the possibility of dropping OleoLite, which is only marginally profitable, so that the entire organization can return to a focus on their mainstay product, Oleo Professional.

Questions

Brett Johnson's new costing system at Oleo assigns overhead to products using direct labor costs as the allocation base.Make sure you understand how the information in Exhibits 5 and 6 is used to calculate the overhead allocated to product lines in Exhibit 7.Also, make sure you see how profit in Exhibit 9 is computed by taking revenue from Exhibit 8 and subtracting direct labor from Exhibit 5 and assigned overhead from Exhibit 7.To illustrate these relationships, explain how the profit of $219,986 for OleoLite in 2015 is derived from Revenue for OleoLite in 2015 in Exhibit 8, Direct Labor in Exhibit 5, and Overhead in Exhibit 7.

1. What was the rationale behind the decision to drop the DistleoLite product line at the end of 2015?What does this rationale assume about the incremental effects on revenue and costs?

2.How did revenue and costs change in 2016 after the DistleoLite product line was dropped, i.e., what were the actual incremental effects on revenue and costs?Why do you think costs increased slightly in 2017 even though a product line was dropped?

3.Why did the formerly profitable Distleo product line become unprofitable in 2016?Given what you know about how direct labor costs are traced to product lines, why do you think the direct labor costs for Distleo increased so dramatically? Why does the increase in direct labor costs for Distleo also translate into an increase in overhead costs assigned to Distleo?

4.How did revenue and costs change in 2017 after dropping the Distleo product line, i.e., what were the actual incremental effects on revenue and costs?Why do you think costs decreased only slightly in 2017 when this product line was dropped?

5.If Jim and Terry decide to drop the OleoLite product line, do you expect profit to decrease by the amount of the profit of $32,350 on the OleoLite product line?

6.Based on the results that have occurred so far, does it appear that the decisions to drop product lines were good short-run decisions?What could have been changed in the short-run or what could be changed in the long-run that would make it a good decision to drop the unprofitable products?

[1] For the first few years of operation, Jim and Terry drew no salary.However, as the business grew and became more profitable, they begin to draw increasingly large salaries.By 2014, their salaries plus benefits amounted to $205,000, and from 2015 onward salaries plus benefits were $230,000.

Exhibit 1

Oleo Software Products

Oleo ProfessionalOriginal product: warehouse optimization software for retailers

OleoLiteWarehouse software for smaller retailers, launched in 2009

DistleoWarehouse software for large distributors, launched in 2012

DistleoLiteWarehouse software for smaller distributors, launched in 2012

Exhibit 2

Oleo Software

Description of Components of Overhead

CategoryDescription

1000Support personnel, including accounting, clerical, maintenance

2000Materials, supplies, and miscellaneous

3000Lease costs

5000Indirect labor costs, including benefits (includes cost of all programmer time not allocated to specific products as direct labor)

6000Salaries and benefits for founders, Jim Little and Terry Bena

Exhibit 3 Condensed Income Statements

2014 2015 2016 2017

Revenue 2,708,960 2,903,659 2,903,886 2,599,724

Total Programmer Costs 1,260,000 1,297,800 1,323,000 1,335,600

Lease Costs 265,000 270,000 270,000 270,000

Founder Salaries 205,000 230,000 230,000 230,000

All other costs 455,000 510,000 524,000 511,000

Net Income 523,960 595,859 556,886

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts