On 1 January 20X4, a new machine was purchased at a list price of $30,500. The company

Question:

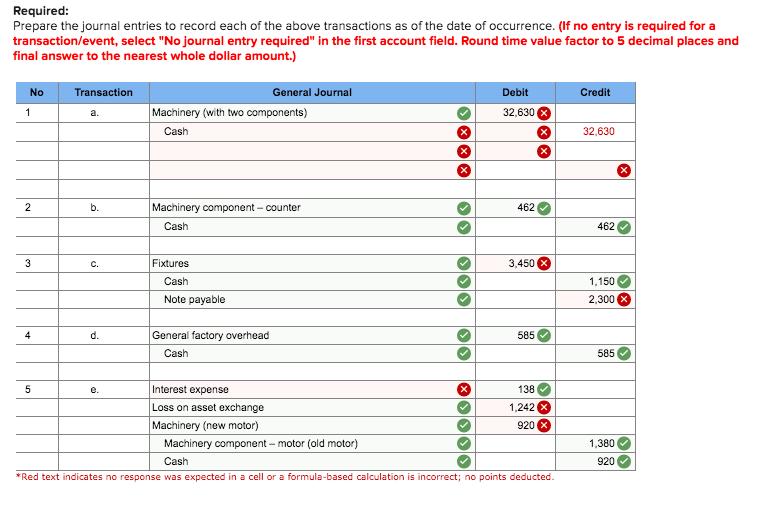

On 1 January 20X4, a new machine was purchased at a list price of $30,500. The company did not take advantage of a 2% cash discount available upon full payment of the invoice within 30 days. Shipping cost paid by the vendor was $420. Installation cost was $1,260, including $420 that represented 10% of the monthly salary of the factory superintendent (installation period, two days). A wall was moved two metres at a cash cost of $870 to make room for the machine. The machine was considered to have two components; an engine valued at $1,300 (net) and the general machine for the balance of the cost.

On 1 January 20X4, the company purchased an automatic counter to be attached to a machine in use; the cost was $462. The estimated useful life of the counter was 7 years, and the estimated life of the machine was 10 years. On 1 January 20X4, the company bought plant fixtures with a list price of $3,450, paying $1,150 cash and giving a one-year, non-interest-bearing note payable for the balance. The current interest rate for this type of note was 15%. Use the net method to record the note payable.

During January 20X4, the first month of operations, the newly purchased machine became inoperative due to a defect in manufacture. The vendor repaired the machine at no cost to GTT; however, the specially trained operator was idle during the two weeks the machine was inoperative. The operator was paid regular wages ($585) during the period, although the only work performed was to observe the repair by the factory representative.

During January 20X5, the company exchanged the electric motor on the machine in part (a) for a heavier motor and gave up the old motor and $920 cash. The market value of the new motor was $1,890. The parts list showed a $1,380 cost for the original motor, and it had been depreciated in 20X4 (estimated life, 10 years).

Expert Answer: