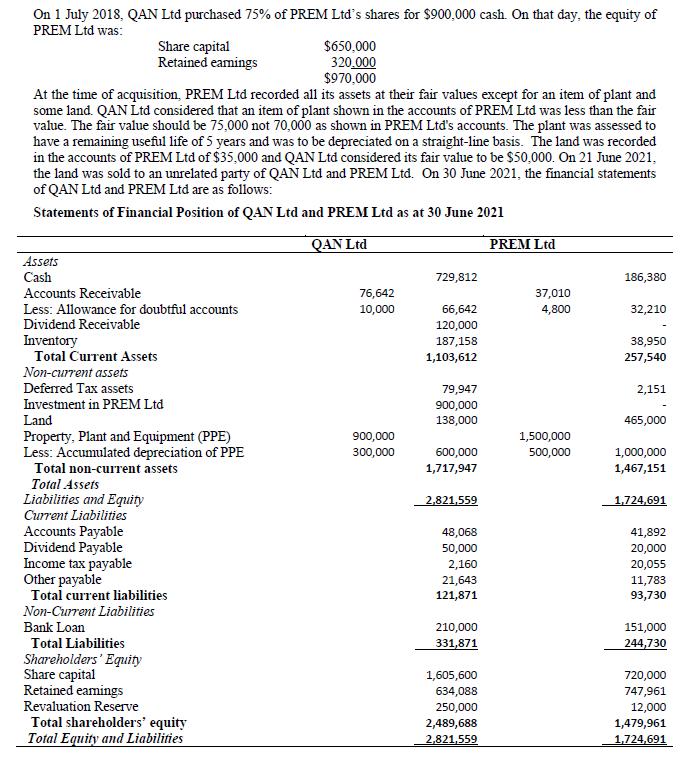

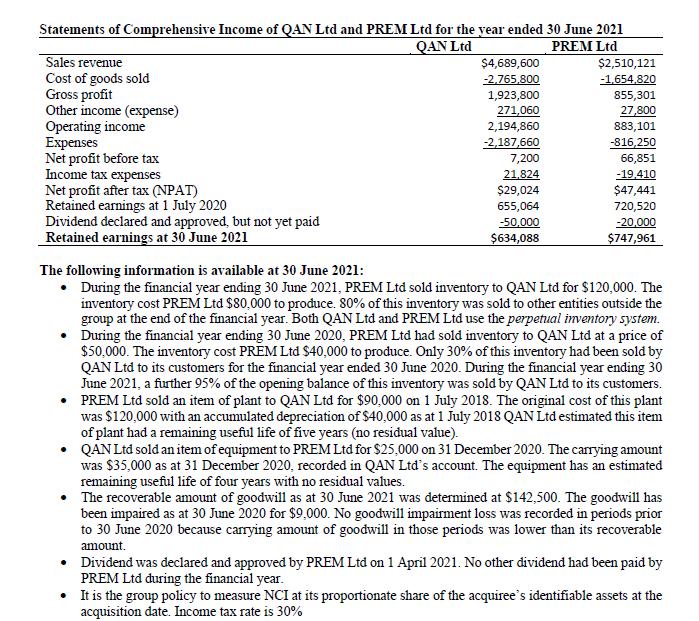

On 1 July 2018, QAN Ltd purchased 75% of PREM Ltd's shares for $900,000 cash. On...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

On 1 July 2018, QAN Ltd purchased 75% of PREM Ltd's shares for $900,000 cash. On that day, the equity of PREM Ltd was: $650,000 320.000 $970,000 At the time of acquisition, PREM Ltd recorded all its assets at their fair values except for an item of plant and some land. QAN Ltd considered that an item of plant shown in the accounts of PREM Ltd was less than the fair value. The fair value should be 75,000 not 70,000 as shown in PREM Ltd's accounts. The plant was assessed to have a remaining useful life of 5 years and was to be depreciated on a straight-line basis. The land was recorded in the accounts of PREM Ltd of $35,000 and QAN Ltd considered its fair value to be $50,000. On 21 June 2021, the land was sold to an unrelated party of QAN Ltd and PREM Ltd. On 30 June 2021, the financial statements Share capital Retained eamings of QAN Ltd and PREM Ltd are as follows: Statements of Financial Position of QAN Ltd and PREM Ltd as at 30 June 2021 QAN Ltd PREM Ltd Assets Cash 729,812 186,380 Accounts Receivable 76,642 37,010 Less: Allowance for doubtful accounts Dividend Receivable 10,000 66,642 4,800 32,210 120,000 Inventory Total Current Assets 187,158 38,950 1,103,612 257,540 Non-current assets Deferred Tax assets 79,947 2,151 Investment in PREM Ltd 900,000 138,000 Land 465,000 Property, Plant and Equipment (PPE) Less: Accumulated depreciation of PPE 900,000 1,500,000 300,000 600,000 500,000 1,000,000 Total non-current assets 1,717,947 1,467,151 Total Assets Liabilities and Eqity Current Liabilities 2,821,559 1,724,691 Accounts Payable Dividend Payable Income tax payable Other payable Total current liabilities Non-Current Liabilities 48,068 41,892 20,000 20,055 50,000 2,160 21,643 121,871 11,783 93,730 Bank Loan 210,000 151,000 Total Liabilities 331,871 244,730 Shareholders' Equity Share capital Retained eamings 1,605,600 720,000 634,088 747,961 Revaluation Reserve 250,000 12,000 Total shareholders' equity Total Equity and Liabilities 2,489,688 1,479,961 2,821,559 1,724,691 Statements of Comprehensive Income of QAN Ltd and PREM Ltd for the year ended 30 June 2021 PREM Ltd $2,510,121 -1,654,820 QAN Ltd Sales revenue Cost of goods sold Gross profit Other income (expense) Operating income Expenses Net profit before tax Income tax expenses Net profit after tax (NPAT) Retained earnings at 1 July 2020 Dividend declared and approved, but not yet paid Retained earnings at 30 June 2021 $4,689,600 -2,765,800 1,923,800 855,301 27,800 883,101 -816,250 66,851 271,060 2,194,860 -2,187,660 7,200 21.824 -19,410 $29,024 $47,441 655,064 720,520 -50,000 -20,000 $634,088 $747,961 The following information is available at 30 June 2021: • During the financial year ending 30 June 2021, PREM Ltd sold inventory to QAN Ltd for $120,000. The inventory cost PREM Ltd $80,000 to produce. 80% of this inventory was sold to other entities outside the group at the end of the financial year. Both QAN Ltd and PREM Ltd use the perpetual inventory system. • During the financial year ending 30 June 2020, PREM Ltd had sold inventory to QAN Ltd at a price of $50,000. The inventory cost PREM Ltd $40,000 to produce. Only 30% of this inventory had been sold by QAN Ltd to its customers for the financial year ended 30 June 2020. During the financial year ending 30 June 2021, a further 95% of the opening balance of this inventory was sold by QAN Ltd to its customers. • PREM Ltd sold an item of plant to QAN Ltd for $90,000 on 1 July 2018. The original cost of this plant was $120,000 with an accumulated depreciation of $40,000 as at 1 July 2018 QAN Ltd estimated this item of plant had a remaining useful life of five years (no residual value). • QAN Ltd sold an item of equipment to PREM Ltd for $25,000 on 31 December 2020. The carrying amount was $35,000 as at 31 December 2020, recorded in QAN Ltd's account. The equipment has an estimated remaining useful life of four years with no residual values. • The recoverable amount of goodwill as at 30 June 2021 was determined at $142,500. The goodwill has been impaired as at 30 June 2020 for $9,000. No goodwill impairment loss was recorded in periods prior to 30 June 2020 because carrying amount of goodwill in those periods was lower than its recoverable amount. • Dividend was declared and approved by PREM Ltd on 1 April 2021. No other dividend had been paid by PREM Ltd during the financial year. • It is the group policy to measure NCI at its proportionate share of the acquiree's identifiable assets at the acquisition date. Income tax rate is 30% 4. Using the format of the template provided, complete a consolidation worksheet and post all consolidation journal entries into the worksheet. (35 marks) On 1 July 2018, QAN Ltd purchased 75% of PREM Ltd's shares for $900,000 cash. On that day, the equity of PREM Ltd was: $650,000 320.000 $970,000 At the time of acquisition, PREM Ltd recorded all its assets at their fair values except for an item of plant and some land. QAN Ltd considered that an item of plant shown in the accounts of PREM Ltd was less than the fair value. The fair value should be 75,000 not 70,000 as shown in PREM Ltd's accounts. The plant was assessed to have a remaining useful life of 5 years and was to be depreciated on a straight-line basis. The land was recorded in the accounts of PREM Ltd of $35,000 and QAN Ltd considered its fair value to be $50,000. On 21 June 2021, the land was sold to an unrelated party of QAN Ltd and PREM Ltd. On 30 June 2021, the financial statements Share capital Retained eamings of QAN Ltd and PREM Ltd are as follows: Statements of Financial Position of QAN Ltd and PREM Ltd as at 30 June 2021 QAN Ltd PREM Ltd Assets Cash 729,812 186,380 Accounts Receivable 76,642 37,010 Less: Allowance for doubtful accounts Dividend Receivable 10,000 66,642 4,800 32,210 120,000 Inventory Total Current Assets 187,158 38,950 1,103,612 257,540 Non-current assets Deferred Tax assets 79,947 2,151 Investment in PREM Ltd 900,000 138,000 Land 465,000 Property, Plant and Equipment (PPE) Less: Accumulated depreciation of PPE 900,000 1,500,000 300,000 600,000 500,000 1,000,000 Total non-current assets 1,717,947 1,467,151 Total Assets Liabilities and Eqity Current Liabilities 2,821,559 1,724,691 Accounts Payable Dividend Payable Income tax payable Other payable Total current liabilities Non-Current Liabilities 48,068 41,892 20,000 20,055 50,000 2,160 21,643 121,871 11,783 93,730 Bank Loan 210,000 151,000 Total Liabilities 331,871 244,730 Shareholders' Equity Share capital Retained eamings 1,605,600 720,000 634,088 747,961 Revaluation Reserve 250,000 12,000 Total shareholders' equity Total Equity and Liabilities 2,489,688 1,479,961 2,821,559 1,724,691 Statements of Comprehensive Income of QAN Ltd and PREM Ltd for the year ended 30 June 2021 PREM Ltd $2,510,121 -1,654,820 QAN Ltd Sales revenue Cost of goods sold Gross profit Other income (expense) Operating income Expenses Net profit before tax Income tax expenses Net profit after tax (NPAT) Retained earnings at 1 July 2020 Dividend declared and approved, but not yet paid Retained earnings at 30 June 2021 $4,689,600 -2,765,800 1,923,800 855,301 27,800 883,101 -816,250 66,851 271,060 2,194,860 -2,187,660 7,200 21.824 -19,410 $29,024 $47,441 655,064 720,520 -50,000 -20,000 $634,088 $747,961 The following information is available at 30 June 2021: • During the financial year ending 30 June 2021, PREM Ltd sold inventory to QAN Ltd for $120,000. The inventory cost PREM Ltd $80,000 to produce. 80% of this inventory was sold to other entities outside the group at the end of the financial year. Both QAN Ltd and PREM Ltd use the perpetual inventory system. • During the financial year ending 30 June 2020, PREM Ltd had sold inventory to QAN Ltd at a price of $50,000. The inventory cost PREM Ltd $40,000 to produce. Only 30% of this inventory had been sold by QAN Ltd to its customers for the financial year ended 30 June 2020. During the financial year ending 30 June 2021, a further 95% of the opening balance of this inventory was sold by QAN Ltd to its customers. • PREM Ltd sold an item of plant to QAN Ltd for $90,000 on 1 July 2018. The original cost of this plant was $120,000 with an accumulated depreciation of $40,000 as at 1 July 2018 QAN Ltd estimated this item of plant had a remaining useful life of five years (no residual value). • QAN Ltd sold an item of equipment to PREM Ltd for $25,000 on 31 December 2020. The carrying amount was $35,000 as at 31 December 2020, recorded in QAN Ltd's account. The equipment has an estimated remaining useful life of four years with no residual values. • The recoverable amount of goodwill as at 30 June 2021 was determined at $142,500. The goodwill has been impaired as at 30 June 2020 for $9,000. No goodwill impairment loss was recorded in periods prior to 30 June 2020 because carrying amount of goodwill in those periods was lower than its recoverable amount. • Dividend was declared and approved by PREM Ltd on 1 April 2021. No other dividend had been paid by PREM Ltd during the financial year. • It is the group policy to measure NCI at its proportionate share of the acquiree's identifiable assets at the acquisition date. Income tax rate is 30% 4. Using the format of the template provided, complete a consolidation worksheet and post all consolidation journal entries into the worksheet. (35 marks)

Expert Answer:

Related Book For

Accounting

ISBN: 978-1118608227

9th edition

Authors: Lew Edwards, John Medlin, Keryn Chalmers, Andreas Hellmann, Claire Beattie, Jodie Maxfield, John Hoggett

Posted Date:

Students also viewed these accounting questions

-

On 1 July 2018 Harris Ltd purchased an 80% controlling interest in Shamin Ltd for a consideration of S350,000. On that date the pre-control equity of Shamin consisted of Paid up capital Retained...

-

on 1 july 2018 Grant ltd acquired an item of equipment with an acquisition cost of $590,000. the equipment can be used for 9 years. residual value is $50,000. on 30 june 2019, the end of financial...

-

On 1 July 2018 Alto Ltd purchased land for $4 000 000, in cash. Alto Ltd uses the cost model to account for land. On 1 July 2018 Alto Ltd purchased equipment for $1 000 000, in cash. Alto Ltd uses...

-

Can public works increase equilibrium wages?

-

Explain the role of financing in a company's EPS

-

What kinds of public diplomacy efforts does the United States undertake to promote its way of life and foreign policy objectives?

-

Choose a country from three of the regions presented in Table 6.7. Using the Internet, collect as much information as you believe is needed to identify the potential for market segments based on age,...

-

On January 1, 2012, Roosevelt Company purchased 12% bonds, having a maturity value of $500,000, for $537,907.40. The bonds provide the bondholders with a 10% yield. They are dated January 1, 2012,...

-

An Olympic lifter (m =103kg) is holding a lift with a mass of 350 kg. The bar exerts a purely vertical force that is equally distributed between both hands. Each arm has a mass of 9 kg, are 0.8m long...

-

14. In this problem you will prove some results about the binomial coefficients, using induction. Recall that () - n! (n k)!k!' where n is a positive integer, and 0

-

7) (12 pts) Consider a network where the sliding window protocol is in use with SWS = RWS = 2 frames and a one way delay of 100ms (i.e. for a frame sent at time t, it arrives at t + 100ms). Assume...

-

NASA. https://climate.nasa.gov/evidence/ climate change evidence: How do we know? Use this link and show the difference between inductive generalization and statistical syllogism using (P1, P2 /C)

-

Read the labels of mineral supplements, compare the DRI's and determine if the supplements could be considered megadoses. Please include your comments on this.

-

In addition to traditional research, students will also engage in real world investigations in NYC. For example, exploring the funding (and budget cuts) for AIDS programs might include a visit to an...

-

How would you describe Garmin's structure? Select two other types of structures and assess whether modification of the selected organization's structure should be considered. Justify the reasons for...

-

Leanne buys, refurbishes, and resells used mobile phones. She agrees to give a refurbished mobile phone from the her warehouse to Dell, a 17-year-old, if Dell promises to pay for the mobile phone by...

-

Separate variables and use partial fractions to solve the initial value problems in Problems 18. Use either the exact solution or a computer-generated slope field to sketch the graphs of several...

-

You are the assistant accountant at Krispies Co. Ltd, a distributor of snack foods. Krispies has a large loan from a bank, and part of the loan agreement stipulates that the company must maintain a...

-

Details of BJM Pty Ltds income statement for the past year are: Sales (22000 units) Cost of sales: Direct materials Direct labour Variable factory overhead Fixed factory overhead $ 440000 396000...

-

The fixed budget performance report for the year ended 30 June 2018 for Motueka Mint is as follows: Budget Actual Variance Units of production: 84 000 94 000 10 000 F Factory overhead: Variable...

-

Goods are products a business sells like a. haircuts. b. conveyer belts. c. car insurance. d. health care.

-

Which of the following are the factors of production? a. Labor, natural resources, capital, entrepreneurs, technology, and intellectual property b. Labor, capital, entrepreneurs, motivation, and good...

-

Which of the following is a current sociocultural trend? a. A decrease in the overall U.S. population b. An increase in the population of Americans ages 30 to 45 years old c. A decrease in the U.S....

Study smarter with the SolutionInn App