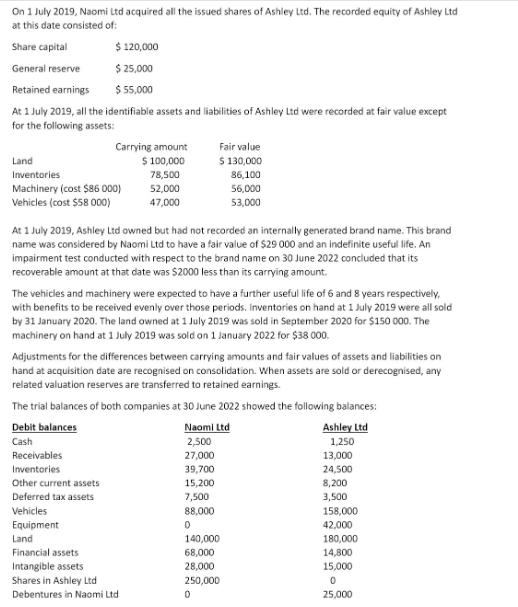

On 1 July 2019, Naomi Ltd acquired all the issued shares of Ashley Ltd. The recorded...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

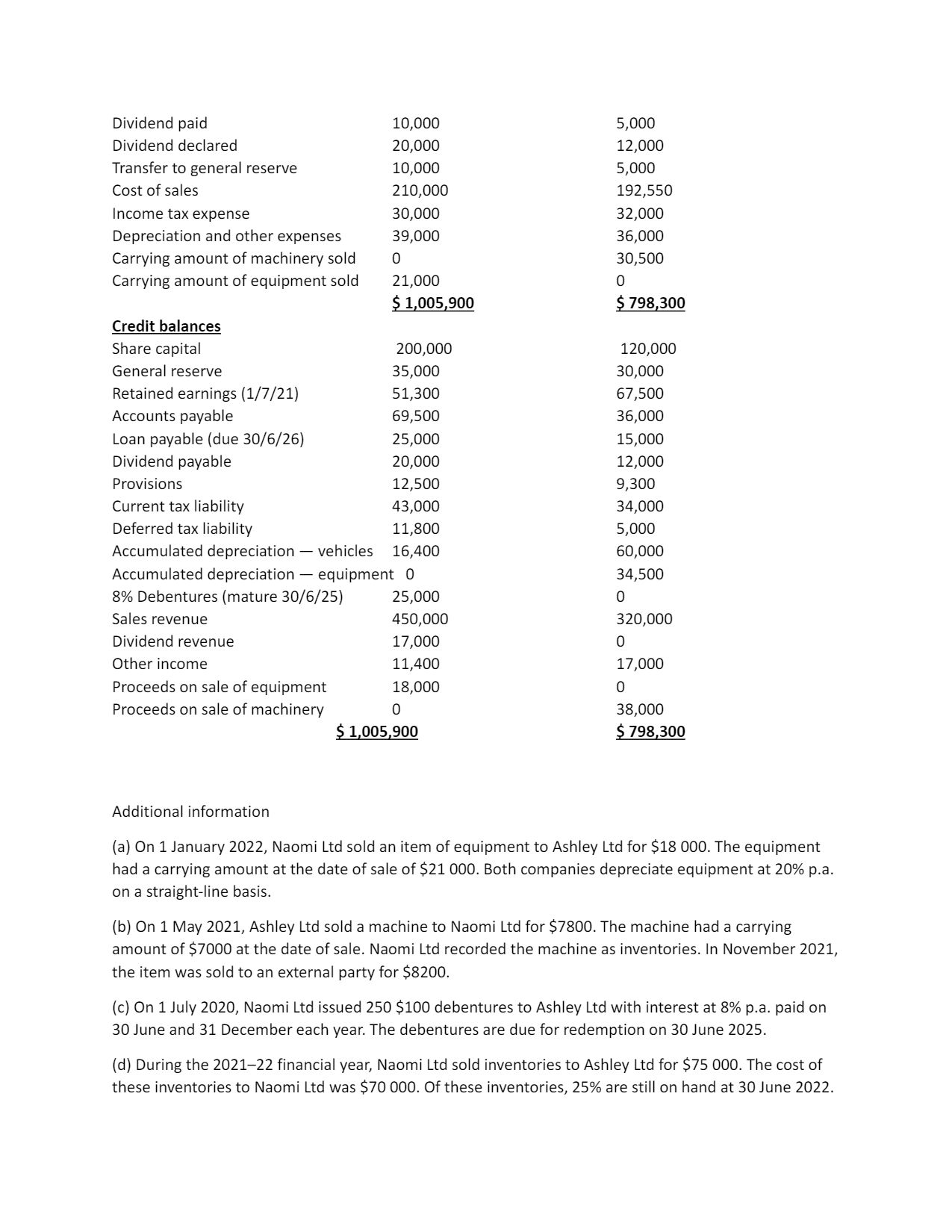

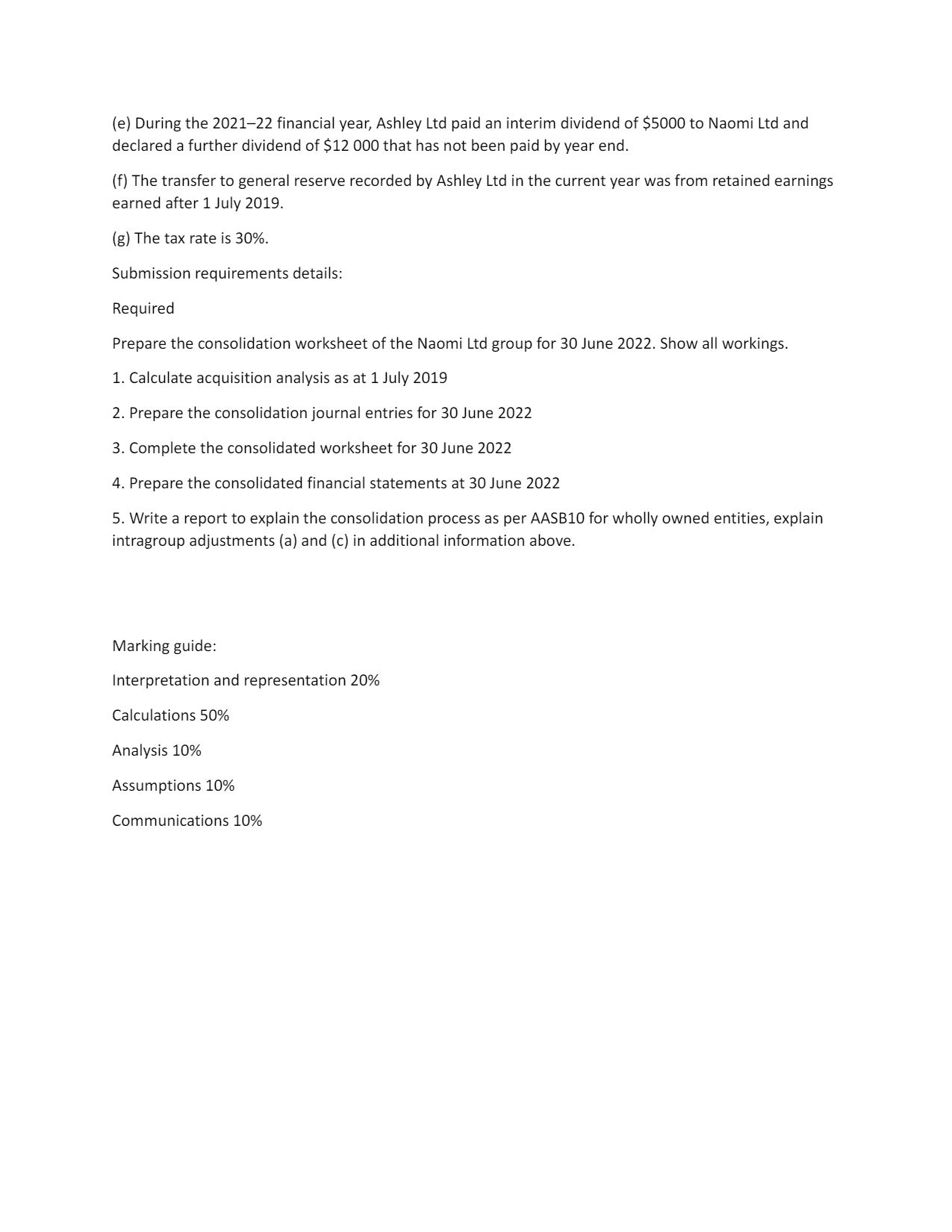

On 1 July 2019, Naomi Ltd acquired all the issued shares of Ashley Ltd. The recorded equity of Ashley Ltd at this date consisted of: Share capital General reserve $120,000 $25,000 Retained earnings $ 55,000 At 1 July 2019, all the identifiable assets and liabilities of Ashley Ltd were recorded at fair value except for the following assets: Carrying amount Fair value Land $100,000 $130,000 Inventories 78,500 86,100 Machinery (cost $86 000) 52,000 56,000 Vehicles (cost $58 000) 47,000 53,000 At 1 July 2019, Ashley Ltd owned but had not recorded an internally generated brand name. This brand name was considered by Naomi Ltd to have a fair value of $29 000 and an indefinite useful life. An impairment test conducted with respect to the brand name on 30 June 2022 concluded that its recoverable amount at that date was $2000 less than its carrying amount. The vehicles and machinery were expected to have a further useful life of 6 and 8 years respectively, with benefits to be received evenly over those periods. Inventories on hand at 1 July 2019 were all sold by 31 January 2020. The land owned at 1 July 2019 was sold in September 2020 for $150 000. The machinery on hand at 1 July 2019 was sold on 1 January 2022 for $38 000. Adjustments for the differences between carrying amounts and fair values of assets and liabilities on hand at acquisition date are recognised on consolidation. When assets are sold or derecognised, any related valuation reserves are transferred to retained earnings. The trial balances of both companies at 30 June 2022 showed the following balances: Debit balances Naomi Ltd Ashley Ltd Cash 2,500 1,250 Receivables 27,000 13,000 Inventories 39,700 24,500 Other current assets 15,200 8,200 Deferred tax assets 7,500 3,500 Vehicles 88,000 158,000 Equipment 0 42,000 Land 140,000 180,000 Financial assets 68,000 14,800 Intangible assets 28,000 15,000 Shares in Ashley Ltd 250,000 0 Debentures in Naomi Ltd 0 25,000 Dividend paid 10,000 5,000 Dividend declared 20,000 12,000 Transfer to general reserve 10,000 5,000 Cost of sales 210,000 192,550 Income tax expense 30,000 32,000 Depreciation and other expenses 39,000 36,000 Carrying amount of machinery sold 0 30,500 Carrying amount of equipment sold 21,000 0 $ 1,005,900 $ 798,300 Credit balances Share capital 200,000 120,000 General reserve 35,000 30,000 Retained earnings (1/7/21) 51,300 67,500 Accounts payable 69,500 36,000 Loan payable (due 30/6/26) 25,000 15,000 Dividend payable 20,000 12,000 Provisions 12,500 9,300 Current tax liability 43,000 34,000 Deferred tax liability 11,800 5,000 Accumulated depreciation - vehicles 16,400 60,000 Accumulated depreciation - equipment 0 34,500 8% Debentures (mature 30/6/25) 25,000 0 Sales revenue 450,000 320,000 Dividend revenue 17,000 0 Other income 11,400 17,000 Proceeds on sale of equipment 18,000 0 Proceeds on sale of machinery 0 $ 1,005,900 38,000 $ 798,300 Additional information (a) On 1 January 2022, Naomi Ltd sold an item of equipment to Ashley Ltd for $18 000. The equipment had a carrying amount at the date of sale of $21 000. Both companies depreciate equipment at 20% p.a. on a straight-line basis. (b) On 1 May 2021, Ashley Ltd sold a machine to Naomi Ltd for $7800. The machine had a carrying amount of $7000 at the date of sale. Naomi Ltd recorded the machine as inventories. In November 2021, the item was sold to an external party for $8200. (c) On 1 July 2020, Naomi Ltd issued 250 $100 debentures to Ashley Ltd with interest at 8% p.a. paid on 30 June and 31 December each year. The debentures are due for redemption on 30 June 2025. (d) During the 2021-22 financial year, Naomi Ltd sold inventories to Ashley Ltd for $75 000. The cost of these inventories to Naomi Ltd was $70 000. Of these inventories, 25% are still on hand at 30 June 2022. (e) During the 2021-22 financial year, Ashley Ltd paid an interim dividend of $5000 to Naomi Ltd and declared a further dividend of $12 000 that has not been paid by year end. (f) The transfer to general reserve recorded by Ashley Ltd in the current year was from retained earnings earned after 1 July 2019. (g) The tax rate is 30%. Submission requirements details: Required Prepare the consolidation worksheet of the Naomi Ltd group for 30 June 2022. Show all workings. 1. Calculate acquisition analysis as at 1 July 2019 2. Prepare the consolidation journal entries for 30 June 2022 3. Complete the consolidated worksheet for 30 June 2022 4. Prepare the consolidated financial statements at 30 June 2022 5. Write a report to explain the consolidation process as per AASB10 for wholly owned entities, explain intragroup adjustments (a) and (c) in additional information above. Marking guide: Interpretation and representation 20% Calculations 50% Analysis 10% Assumptions 10% Communications 10% On 1 July 2019, Naomi Ltd acquired all the issued shares of Ashley Ltd. The recorded equity of Ashley Ltd at this date consisted of: Share capital General reserve $120,000 $25,000 Retained earnings $ 55,000 At 1 July 2019, all the identifiable assets and liabilities of Ashley Ltd were recorded at fair value except for the following assets: Carrying amount Fair value Land $100,000 $130,000 Inventories 78,500 86,100 Machinery (cost $86 000) 52,000 56,000 Vehicles (cost $58 000) 47,000 53,000 At 1 July 2019, Ashley Ltd owned but had not recorded an internally generated brand name. This brand name was considered by Naomi Ltd to have a fair value of $29 000 and an indefinite useful life. An impairment test conducted with respect to the brand name on 30 June 2022 concluded that its recoverable amount at that date was $2000 less than its carrying amount. The vehicles and machinery were expected to have a further useful life of 6 and 8 years respectively, with benefits to be received evenly over those periods. Inventories on hand at 1 July 2019 were all sold by 31 January 2020. The land owned at 1 July 2019 was sold in September 2020 for $150 000. The machinery on hand at 1 July 2019 was sold on 1 January 2022 for $38 000. Adjustments for the differences between carrying amounts and fair values of assets and liabilities on hand at acquisition date are recognised on consolidation. When assets are sold or derecognised, any related valuation reserves are transferred to retained earnings. The trial balances of both companies at 30 June 2022 showed the following balances: Debit balances Naomi Ltd Ashley Ltd Cash 2,500 1,250 Receivables 27,000 13,000 Inventories 39,700 24,500 Other current assets 15,200 8,200 Deferred tax assets 7,500 3,500 Vehicles 88,000 158,000 Equipment 0 42,000 Land 140,000 180,000 Financial assets 68,000 14,800 Intangible assets 28,000 15,000 Shares in Ashley Ltd 250,000 0 Debentures in Naomi Ltd 0 25,000 Dividend paid 10,000 5,000 Dividend declared 20,000 12,000 Transfer to general reserve 10,000 5,000 Cost of sales 210,000 192,550 Income tax expense 30,000 32,000 Depreciation and other expenses 39,000 36,000 Carrying amount of machinery sold 0 30,500 Carrying amount of equipment sold 21,000 0 $ 1,005,900 $ 798,300 Credit balances Share capital 200,000 120,000 General reserve 35,000 30,000 Retained earnings (1/7/21) 51,300 67,500 Accounts payable 69,500 36,000 Loan payable (due 30/6/26) 25,000 15,000 Dividend payable 20,000 12,000 Provisions 12,500 9,300 Current tax liability 43,000 34,000 Deferred tax liability 11,800 5,000 Accumulated depreciation - vehicles 16,400 60,000 Accumulated depreciation - equipment 0 34,500 8% Debentures (mature 30/6/25) 25,000 0 Sales revenue 450,000 320,000 Dividend revenue 17,000 0 Other income 11,400 17,000 Proceeds on sale of equipment 18,000 0 Proceeds on sale of machinery 0 $ 1,005,900 38,000 $ 798,300 Additional information (a) On 1 January 2022, Naomi Ltd sold an item of equipment to Ashley Ltd for $18 000. The equipment had a carrying amount at the date of sale of $21 000. Both companies depreciate equipment at 20% p.a. on a straight-line basis. (b) On 1 May 2021, Ashley Ltd sold a machine to Naomi Ltd for $7800. The machine had a carrying amount of $7000 at the date of sale. Naomi Ltd recorded the machine as inventories. In November 2021, the item was sold to an external party for $8200. (c) On 1 July 2020, Naomi Ltd issued 250 $100 debentures to Ashley Ltd with interest at 8% p.a. paid on 30 June and 31 December each year. The debentures are due for redemption on 30 June 2025. (d) During the 2021-22 financial year, Naomi Ltd sold inventories to Ashley Ltd for $75 000. The cost of these inventories to Naomi Ltd was $70 000. Of these inventories, 25% are still on hand at 30 June 2022. (e) During the 2021-22 financial year, Ashley Ltd paid an interim dividend of $5000 to Naomi Ltd and declared a further dividend of $12 000 that has not been paid by year end. (f) The transfer to general reserve recorded by Ashley Ltd in the current year was from retained earnings earned after 1 July 2019. (g) The tax rate is 30%. Submission requirements details: Required Prepare the consolidation worksheet of the Naomi Ltd group for 30 June 2022. Show all workings. 1. Calculate acquisition analysis as at 1 July 2019 2. Prepare the consolidation journal entries for 30 June 2022 3. Complete the consolidated worksheet for 30 June 2022 4. Prepare the consolidated financial statements at 30 June 2022 5. Write a report to explain the consolidation process as per AASB10 for wholly owned entities, explain intragroup adjustments (a) and (c) in additional information above. Marking guide: Interpretation and representation 20% Calculations 50% Analysis 10% Assumptions 10% Communications 10%

Expert Answer:

Related Book For

Posted Date:

Students also viewed these accounting questions

-

Topic: Consolidation worksheet with adjustment entries for intragroup transactions: inventories, PPE, services On 1 July 2 0 1 9 , Naomi Ltd acquired all the issued shares of Ashley Ltd . The...

-

How do recruitment and selection practices contribute to high performance in an organization?

-

Describe the sustainable approach to developing alternatives in the decision making process.

-

Solve the equation. 3+p= 7- 32-P V

-

Millions of high school graduates decide annually to enroll in a college or university. Many factors can influence a students choice of where to enroll. List the five steps of the decision-making...

-

Northstar uses ABC to account for its chrome wheel manufacturing process. Company man-agers have identified four manufacturing activities that incur manufacturing overhead costs: materials handling,...

-

Review the major theoretical models , including the neuroscience, evolutionary, behavior genetics, psychodynamic, behavioral, cognitive, and social-cultural theoretical models. Think about the major...

-

Multiple Choice Questions: 1) Which of the following will result in an unfavorable direct labor cost variance? A) When actual direct labor hours exceed standard direct labor hours B) When actual...

-

Mega Vaganza Berhad is a business that sold sport shoes catered for teenagers. The following information is extracted from the business Trial Balance as at 31 December 2022: Debit RM Credit RM...

-

Ernesto is the company's chief financial officer. He must explain to the board of directors how the figures in the company's financial statements were calculated. This will be an easy and routine...

-

Find the value of an investment of $14,771 for 14 years at an annual interest rate of 5.27% compounded continuously.

-

Alice wants to buy apples, beets, and carrots. An apple, a beet, and a carrot cost 16 dollars, two apples and three beets cost 23 dollars, and one apple, two beets, and three carrots cost 35 dollars....

-

Megan and Nancy each want save $250 000 for their retirement 40 years. a) Nancy begins her regular deposits immediately. How much must she deposit end 12% per year compounded annually achieve her...

-

Make a presentation on the organizational culture of Nike

-

Economic feasibility is an important guideline in designing cost accounting systems. Do you agree? Explain.

-

Vertical analysis would rarely be performed on which of the following statements or schedules? a. Income statement b. Adjusting entry worksheet c. Balance sheet d. All of the above are common targets...

-

A statement that lists the assets, liabilities, and stockholders equity of a company in percentages only with no dollar amounts is a a. common-size income statement. b. benchmarking analysis. c....

-

In vertical analysis, the base used for comparison on the income statement is a. total expenses. b. total assets. c. net sales. d. gross profit.

Study smarter with the SolutionInn App