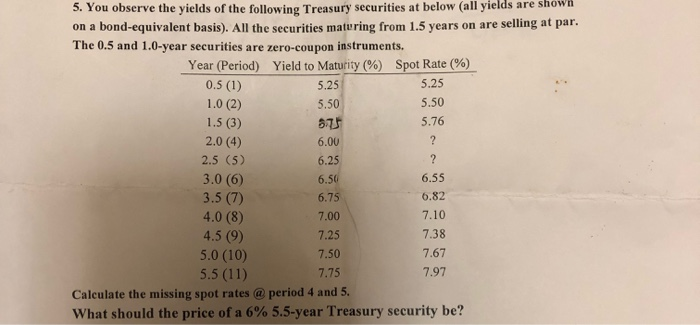

Question: on a bond-equivalent basis). All the securities maturing from 1.5 years on are selling at par. The 0.5 and 1.0-year securities are zero-coupon instruments. Spot

on a bond-equivalent basis). All the securities maturing from 1.5 years on are selling at par. The 0.5 and 1.0-year securities are zero-coupon instruments. Spot Rate (%) Year (Period) Yield to Maturity (%) 5.25 5.25 5.50 1.0 (2) 5.50 5.76 1.5 (3) 2.0 (4) 875 6.00 2.5 (5) 3.0 (6) 3.5 (7) 4.0 (8) 4.5 (9) 5.0 (10) 5.5 (11) 6.25 6.55 6.50 6.75 6.82 7.10 7.00 7.38 7.25 7.67 7.50 7.97 7.75 Calculate the missing spot rates @ period 4 and 5. what should the price of a 6% 55-year Treasury security be

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock