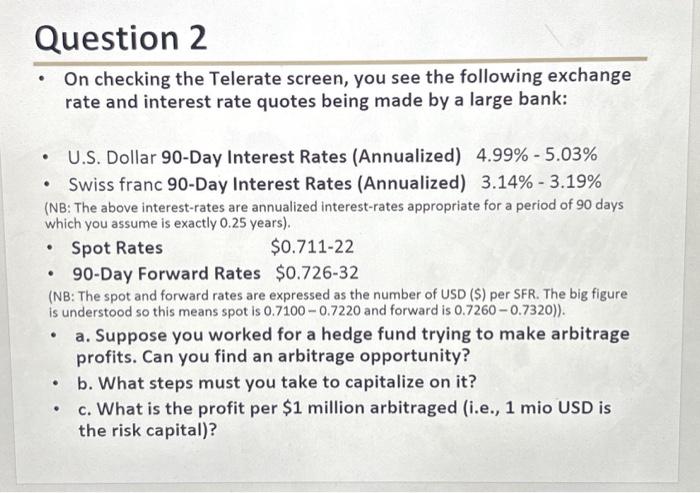

Question: - On checking the Telerate screen, you see the following exchange rate and interest rate quotes being made by a large bank: - U.S. Dollar

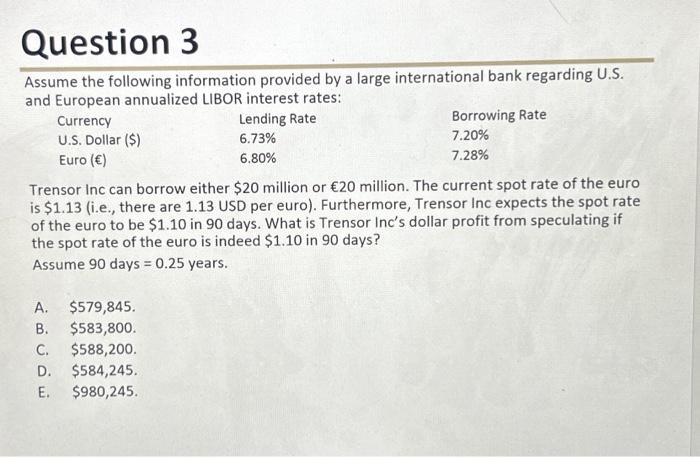

- On checking the Telerate screen, you see the following exchange rate and interest rate quotes being made by a large bank: - U.S. Dollar 90-Day Interest Rates (Annualized) 4.99%5.03% - Swiss franc 90-Day Interest Rates (Annualized) 3.14\% - 3.19\% (NB: The above interest-rates are annualized interest-rates appropriate for a period of 90 days which you assume is exactly 0.25 years). - Spot Rates $0.71122 - 90-Day Forward Rates \$0.726-32 (NB: The spot and forward rates are expressed as the number of USD (\$) per SFR. The big figure is understood so this means spot is 0.71000.7220 and forward is 0.72600.7320) ). - a. Suppose you worked for a hedge fund trying to make arbitrage profits. Can you find an arbitrage opportunity? - b. What steps must you take to capitalize on it? - c. What is the profit per $1 million arbitraged (i.e., 1 mio USD is the risk capital)? Assume the following information provided by a large international bank regarding U.S. and European annualized LIBOR interest rates: e Trensor Inc can borrow either $20 million or 20 million. The current spot rate of the euro is $1.13 (i.e., there are 1.13 USD per euro). Furthermore, Trensor Inc expects the spot rate of the euro to be $1.10 in 90 days. What is Trensor Inc's dollar profit from speculating if the spot rate of the euro is indeed $1.10 in 90 days? Assume 90 days =0.25 years. A. $579,845. B. $583,800. C. $588,200. D. $584,245. E. $980,245

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts