On January 1, 2015, Purple Rain Company acquired Sunshine Company. Purple Rain Company paid $60 per share

Question:

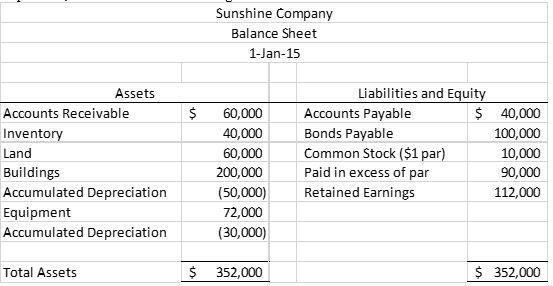

On January 1, 2015, Purple Rain Company acquired Sunshine Company. Purple Rain Company paid $60 per share for 80% of Sunshine’s common stock. The price paid by Purple reflected a control premium. The NCI shares were estimated to have a market value of $55 per share. On the date of acquisition, Sunshine had the following balance sheet:

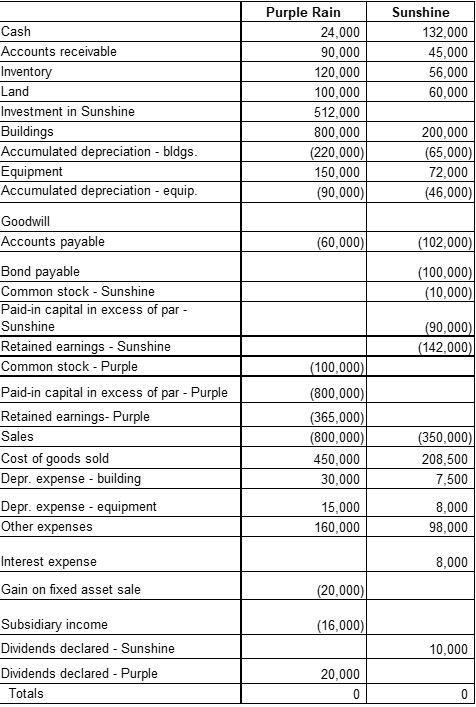

Buildings, which have a 20-year life, were understated by $120,000. Equipment, which has a 5-year life was understated by $40,000. Any remaining excess was considered goodwill. Purple used the simple equity method to account for its investment in Sunshine. January 1, 2016, Purple held merchandise sold to it from Sunshine for $12,000. This beginning inventory had an applicable gross profit of 20%. During 2016, Sunshine sold merchandise to Purple for $90,000. On December 31, 2016, Purple held $18,000 of this merchandise in its inventory (applicable gross profit rate of 25%). Purple owed Sunshine $20,000 on December 31, 2016 as a result of this intercompany sale. On January 1, 2016, Purple sold equipment with a book value of $35,000 to Sunshine for $45,000. Purple also sold assets to nonaffiliates. During 2016, the equipment was used by Sunshine. Depreciation is computed over a 5-year life, using the straight-line method. Purple and Sunshine had the following trial balances on December 31, 2016 (end of second year):

a. Prepare a value analysis and determination of distribution of excess schedule for the investment in Sunshine on January 1, 2015.

b. Write out the elimination entries (in journal form) for the December 31, 2016 consolidation.

c. Prepare the consolidated worksheet as of December 31, 2016, including the income distribution schedule. (The trial balance above is also attached in Excel format.)

Expert Answer:

Blufon2 Rse Pase a valve arallysis and a detexRnaffion and dishibetion of excess schedele ... View the full answer

Fundamentals of Taxation 2016

ISBN: 9781259812774

9th edition

Authors: Ana Cruz, Michael Deschamps, Frederick Niswander, Debra Prendergast, Dan Schisler, Jinhee Trone