On January 1, 2016, PT ABC acquired 90 percent of PT DEF. Details of the acquisition are

Question:

On January 1, 2016, PT ABC acquired 90 percent of PT DEF. Details of the acquisition are as follows:

Investment cost by PT ABC . . . . . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $576,000

Noncontrolling interest acquisition-date fair value . . . . . . . . . . . . . . . . . . . . 64,000

Silver total fair value . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $640,000

Silver book value . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 600,000

Excess fair value over book value assigned to brand name (20-year life) $ 40,000

Subsequently, on January 1, 2017, PT DEF purchased 10 percent of PT ABC for $150,000. This price equaled the book value of PT ABC’s underlying net assets and no allocation was made to either goodwill or any specific accounts.

On January 1, 2018, PT ABC and PT DEF each acquired 30 percent of the outstanding shares of PT JKL for $105,000 apiece, which resulted in PT ABC obtaining control over PT JKL. Details of this acquisition are as follows:

Consideration transferred by PT ABC and PT DEF ($105,000 each) . . . . . . . .$210,000

Noncontrolling interest acquisition-date fair value . . . . . . . . . . . . . . . . . . . . 140,000

PT JKL total fair value . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $350,000

PT JKL book value . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 300,000

Excess fair value over book value assigned to copyright (10-year life) $ 50,000

After the formation of this business combination PT DEF made significant intra-entity inventory sales to PT ABC. The volume of these transfers follows:

Year | Transfer Price to PT ABC | Markup on Transfer Price | Inventory Retained at Year-End (at transfer price) |

2016 | $100,000 | 30% | $ 60,000 |

2017 | 160,000 | 25 | 90,000 |

2018 | 200,000 | 28 | 120,000 |

In addition, on July 1, 2018, PT ABC sold PT JKL a tract of land for $25,000. This property cost $12,000 when the parent acquired it several years ago.

The initial value method is used to account for all investments. The individual firms recognize income from the investments when dividends are declared. Because consolidated statements are prepared for the business combination, accounting for the investments affects internal reporting only. During 2016 and 2017, PT ABC and PT DEF individually reported the following information:

PT ABC | PT DEF | |

2016: | ||

Separate company income . . . . . . . . . . . . . . . | $180,000 | $120,000 |

Dividend income—PT DEF (90%) . . . . . . . | 36,000 | –0– |

Dividends declared . . . . . . . . . . . . . . . . . . . | 80,000 | 40,000 |

2017: | ||

Separate company income . . . . . . . . . . . | 240,000 | 150,000 |

Dividend income—PT ABC (10%) . . . . | –0– | 9,000 |

Dividend income—PT DEF (90%) . . . . . . . | 27,000 | –0– |

Dividends declared . . . . . . . . . . . . . . . . . . . . . . | 90,000 | 30,000 |

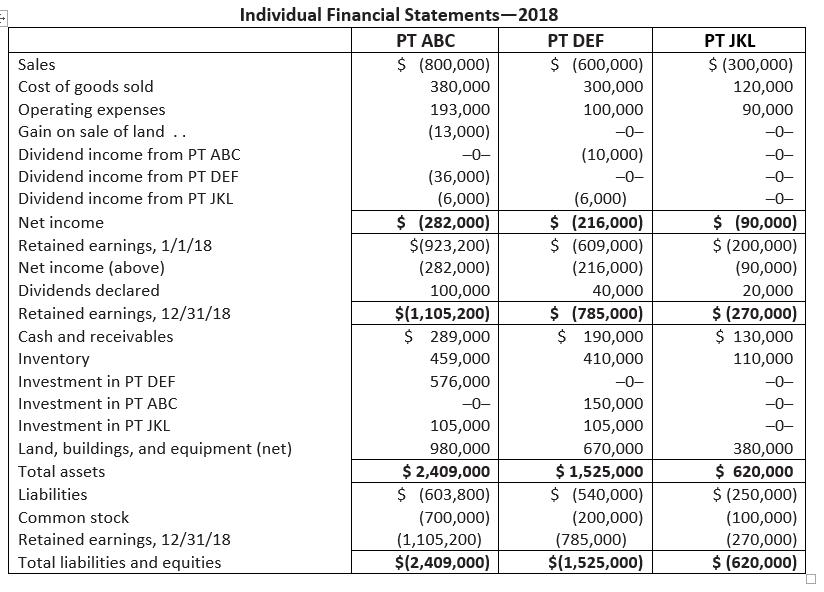

The 2018 financial statements for each of the three companies comprising this business combination are presented below. These figures ignore income tax effects.

Required

a. Prepare worksheet entries to consolidate the 2018 financial statements for this combination. Assume that the mutual ownership between PT ABC and PT DEF is accounted for by means of the treasury stock approach. Compute the noncontrolling interests in consolidated net income from PT JKL’s income and in PT DEF’s income.

b. Assume that consolidated net income (before deducting any balance for the noncontrolling interests) amounts to $498,900. Assume also that the effective tax rate is 40 percent and that PT ABC and PT DEF file a consolidated tax return but PT JKL files separately. Calculate the income tax expense recognized within the consolidated income statement for 2018.

Expert Answer:

Here are the worksheet entries to consolidate the 2018 financial statements for this combination ass... View the full answer

Advanced Accounting

ISBN: 978-1259444951

13th edition

Authors: Joe Ben Hoyle, Thomas Schaefer, Timothy Doupni