On January 1, 2017, Sheffield Company contracts to lease equipment for 5 years, agreeing to make a

Question:

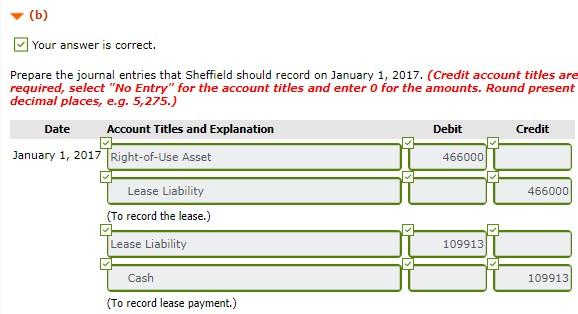

On January 1, 2017, Sheffield Company contracts to lease equipment for 5 years, agreeing to make a payment of $109,913 at the beginning of each year, starting January 1, 2017. The leased equipment is to be capitalized at $466,000. The asset is to be amortized on a double-declining-balance basis, and the obligation is to be reduced on an effective-interest basis. Sheffield’s incremental borrowing rate is 6%, and the implicit rate in the lease is 9%, which is known by Sheffield. Title to the equipment transfers to Sheffield at the end of the lease. The asset has an estimated useful life of 5 years and no residual value.

How would the value of the lease liability in part (b) change if Sheffield also agreed to pay the fixed annual insurance on the equipment of $2,000 at the same time as the rental payments? (Round answers to 0 decimal places, e.g. 5,275.) Please give an amount?

Expert Answer:

Intermediate Accounting IFRS

ISBN: 978-1119372936

3rd edition

Authors: Donald E. Kieso, Jerry J. Weygandt, Terry D. Warfield