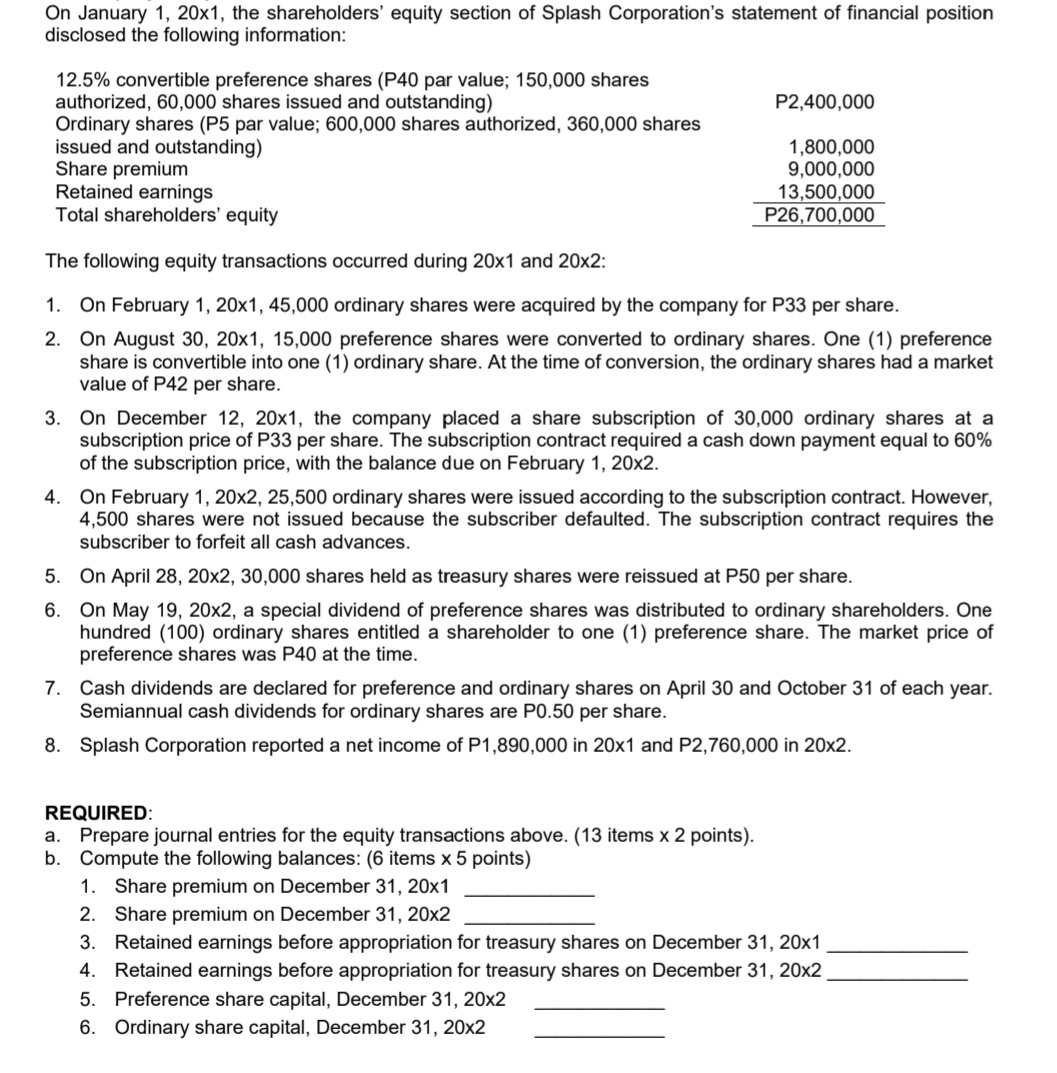

On January 1, 20x1, the shareholders' equity section of Splash Corporation's statement of financial position disclosed...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

a Journal Entries for Equity Transactions February 1 20x1 Acquisition of 45000 ordinary shares as treasury shares Debit Treasury Shares 1485000 Credit ... View the full answer

Related Book For

Financial Accounting A User Perspective

ISBN: 978-0470676608

6th Canadian Edition

Authors: Robert E Hoskin, Maureen R Fizzell, Donald C Cherry

Posted Date: