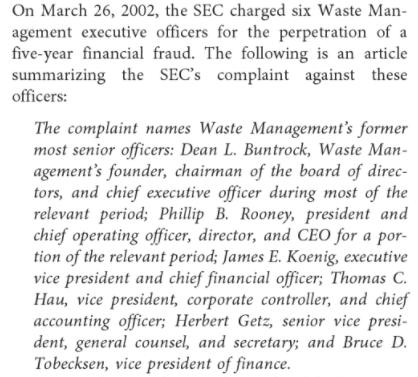

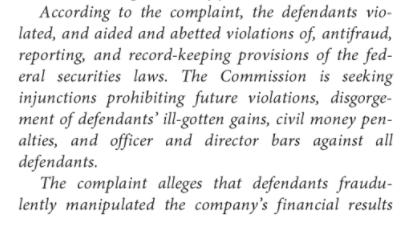

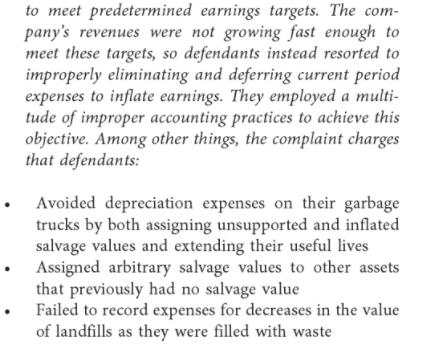

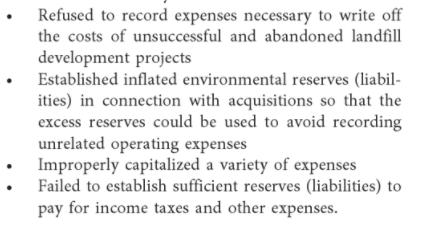

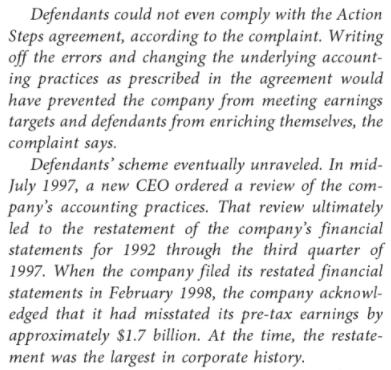

On March 26, 2002, the SEC charged six Waste Man- agement executive officers for the perpetration...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text: