On March 30, 2021, Leo purchased and placed in service a new car that cost $55,200....

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

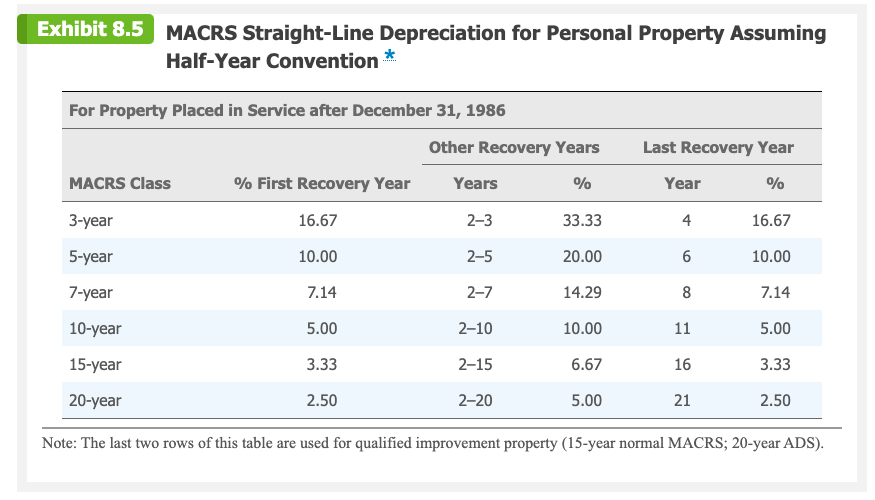

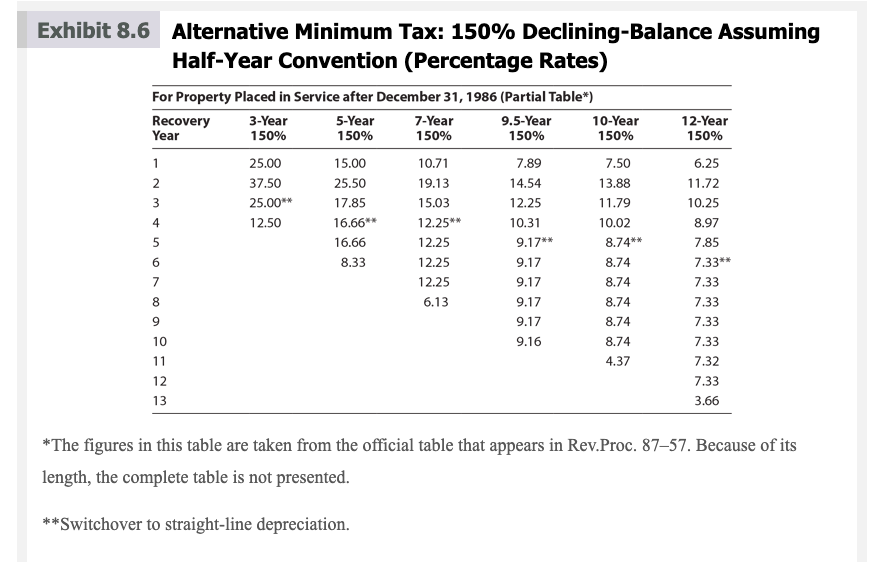

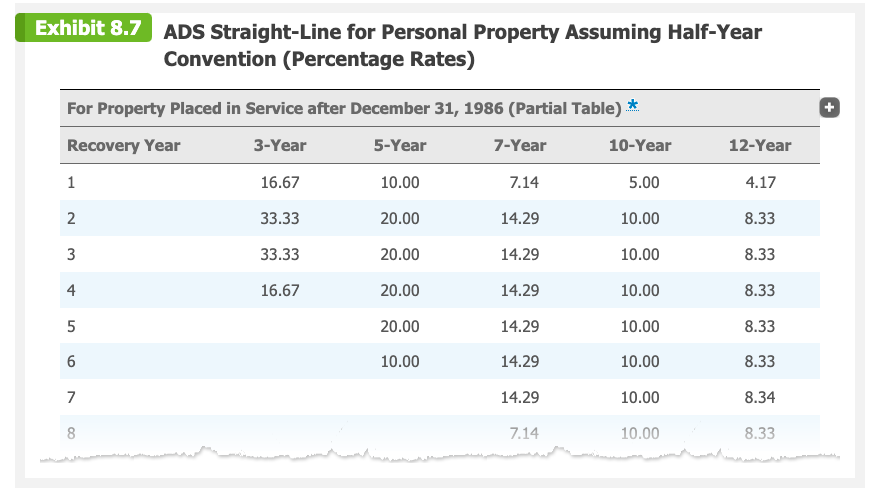

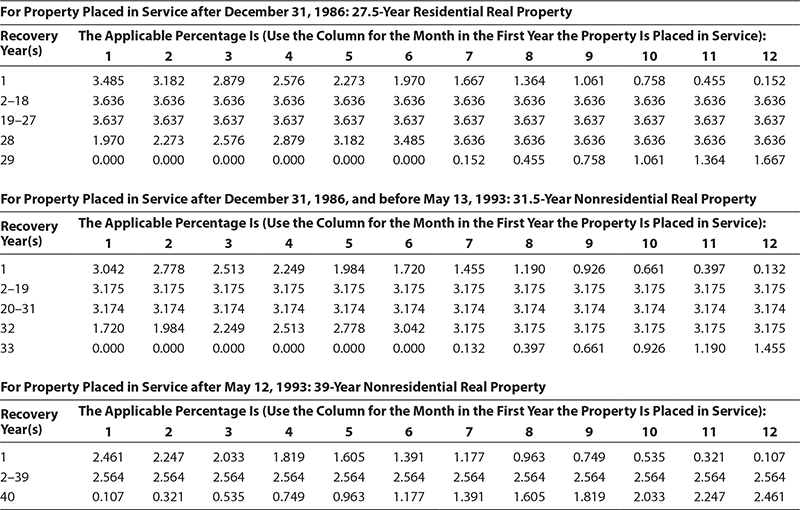

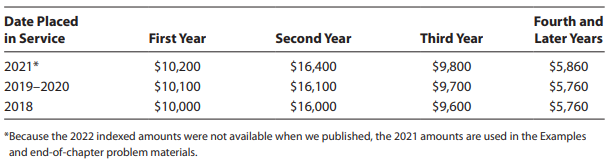

On March 30, 2021, Leo purchased and placed in service a new car that cost $55,200. The business use percentage for the car is always 100%. He does not take the additional first-year depreciation or any § 179. If required, round your answers to the nearest dollar. Click here to access the depreciation table of the textbook. Click here to access the limits for certain automobiles. a. What MACRS convention applies to the new car? Half-year b. Is the automobile considered "listed property"? Yes c. Leo's cost recovery deduction in 2021 is $ and for 2022 is $1 Exhibit 8.3 MACRS Accelerated Depreciation for Personal Property Assuming Half-Year Convention (Percentage Rates) For Property Placed in Service after December 31, 1986 3-Year (200% DB) 5-Year (200% DB) Recovery Year 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 33.33 44.45 14.81* 7.41 20.00 32.00 19.20 11.52* 11.52 5.76 *Switchover to straight-line depreciation. 7-Year (200% DB) 14.29 24.49 17.49 12.49 8.93* 8.92 8.93 4.46 10-Year (200% DB) 10.00 18.00 14.40 11.52 9.22 7.37 6.55* 6.55 6.56 6.55 3.28 15-Year (150% DB) 5.00 9.50 8.55 7.70 6.93 6.23 5.90* 5.90 5.91 5.90 5.91 5.90 5.91 5.90 5.91 2.95 20-Year (150% DB) 3.750 7.219 6.677 6.177 5.713 5.285 4.888 4.522 4.462* 4.461 4.462 4.461 4.462 4.461 4.462 4.461 4.462 4.461 4.462 4.461 2.231 Exhibit 8.4 MACRS Accelerated Depreciation for Personal Property Assuming Mid-Quarter Convention (Percentage Rates) For Property Placed in Service after December 31, 1986 (Partial Table * ) 3-Year First Quarter Second Quarter Recovery Year 1 2 Recovery Year 1 2 58.33 27.78 First Quarter 35.00 26.00 41.67 38.89 5-Year Second Quarter 25.00 30.00 7-Year Third Quarter 25.00 50.00 Third Quarter 15.00 34.00 Fourth Quarter 8.33 61.11 Fourth Quarter 5.00 38.00 + Exhibit 8.3 MACRS Accelerated Depreciation for Personal Property Assuming Half-Year Convention (Percentage Rates) For Property Placed in Service after December 31, 1986 3-Year (200% DB) 5-Year (200% DB) Recovery Year 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 33.33 44.45 14.81* 7.41 20.00 32.00 19.20 11.52* 11.52 5.76 *Switchover to straight-line depreciation. 7-Year (200% DB) 14.29 24.49 17.49 12.49 8.93* 8.92 8.93 4.46 10-Year (200% DB) 10.00 18.00 14.40 11.52 9.22 7.37 6.55* 6.55 6.56 6.55 3.28 15-Year (150% DB) 5.00 9.50 8.55 7.70 6.93 6.23 5.90* 5.90 5.91 5.90 5.91 5.90 5.91 5.90 5.91 2.95 20-Year (150% DB) 3.750 7.219 6.677 6.177 5.713 5.285 4.888 4.522 4.462* 4.461 4.462 4.461 4.462 4.461 4.462 4.461 4.462 4.461 4.462 4.461 2.231 Exhibit 8.5 MACRS Straight-Line Depreciation for Personal Property Assuming Half-Year Convention * For Property Placed in Service after December 31, 1986 MACRS Class 3-year 5-year 7-year 10-year 15-year 20-year Note: The last two rows of this table are used for qualified improvement property (15-year normal MACRS; 20-year ADS). % First Recovery Year 16.67 10.00 7.14 5.00 3.33 Other Recovery Years Last Recovery Year % % 2.50 Years 2-3 2-5 2-7 2-10 2-15 2-20 33.33 20.00 14.29 10.00 6.67 5.00 Year 4 6 8 11 16 21 16.67 10.00 7.14 5.00 3.33 2.50 Exhibit 8.6 Alternative Minimum Tax: 150% Declining-Balance Assuming Half-Year Convention (Percentage Rates) For Property Placed in Service after December 31, 1986 (Partial Table*) 5-Year 9.5-Year 150% 150% Recovery Year 1 2 3 4 6 7 8 9 10 11 123 3-Year 150% 25.00 37.50 25.00** 12.50 15.00 25.50 17.85 16.66** 16.66 8.33 7-Year 150% 10.71 19.13 15.03 12.25** 12.25 12.25 12.25 6.13 7.89 14.54 12.25 10.31 9.17** 9.17 9.17 9.17 9.17 9.16 10-Year 150% 7.50 13.88 11.79 10.02 8.74** 8.74 8.74 8.74 8.74 8.74 4.37 12-Year 150% 6.25 11.72 10.25 8.97 7.85 7.33** 7.33 7.33 7.33 7.33 7.32 7.33 3.66 *The figures in this table are taken from the official table that appears in Rev.Proc. 87-57. Because of its length, the complete table is not presented. **Switchover to straight-line depreciation. Exhibit 8.7 ADS Straight-Line for Personal Property Assuming Half-Year Convention (Percentage Rates) For Property Placed in Service after December 31, 1986 (Partial Table) * Recovery Year 3-Year 5-Year 7-Year 10-Year 16.67 10.00 33.33 20.00 20.00 20.00 20.00 10.00 1 2 3 4 5 6 7 8 لیا 33.33 16.67 7.14 14.29 14.29 14.29 14.29 14.29 14.29 7.14 5.00 10.00 10.00 10.00 10.00 10.00 10.00 10.00 12-Year 4.17 8.33 8.33 8.33 8.33 8.33 8.34 8.33 + For Property Placed in Service after December 31, 1986: 27.5-Year Residential Real Property Recovery The Applicable Percentage Is (Use the Column for the Month in the First Year the Property Is Placed in Service): Year(s) 1 2 3 4 5 6 7 8 10 11 3.485 3.182 2.576 2.273 1.970 3.636 3.636 3.636 2.879 3.636 3.636 3.636 3.637 3.637 3.637 1.970 2.273 2.576 2.879 3.182 0.000 0.000 0.000 0.000 0.000 3.637 3.637 1 2-18 19-27 28 29 1 2-19 20-31 For Property Placed in Service after December 31, 1986, and before May 13, 1993: 31.5-Year Nonresidential Real Property Recovery The Applicable Percentage Is (Use the Column for the Month in the First Year the Property Is Placed in Service): Year(s) 1 2 3 4 5 6 7 8 9 10 11 32 33 3.042 2.778 2.513 3.175 3.175 3.175 3.174 1.720 0.000 1 2-39 40 9 1.364 1.061 0.758 0.455 3.636 3.636 3.636 3.636 1.667 3.636 3.637 3.637 3.637 3.637 3.637 3.637 3.485 3.636 3.636 3.636 3.636 3.636 0.000 0.152 0.455 0.758 1.061 1.364 1 2.461 2.564 0.107 3.175 3.174 3.174 3.174 1.984 2.249 2.513 2.778 0.000 0.000 0.000 0.000 2.249 1.984 1.720 3.175 3.175 3.175 3.174 3.174 3.174 3.042 3.175 0.000 0.132 1.455 1.190 3.175 3.174 3.175 0.397 0.926 0.661 3.175 3.175 3.174 3.174 3.174 3.175 3.175 3.175 0.661 0.926 1.190 0.397 3.175 12 0.152 3.636 3.637 3.636 1.667 For Property Placed in Service after May 12, 1993: 39-Year Nonresidential Real Property Recovery The Applicable Percentage Is (Use the Column for the Month in the First Year the Property is placed in Service): Year(s) 2 3 4 5 6 7 8 9 10 11 1.177 0.963 0.749 2.247 2.033 1.819 1.605 1.391 2.564 2.564 2.564 0.749 0.963 1.177 1.391 1.605 1.819 2.564 2.564 2.564 2.564 2.564 0.321 0.535 0.535 0.321 2.564 2.564 2.033 2.247 12 0.132 3.175 3.174 3.175 1.455 12 0.107 2.564 2.461 Date Placed in Service 2021* 2019-2020 2018 First Year $10,200 $10,100 $10,000 Second Year $16,400 $16,100 $16,000 Third Year $9,800 $9,700 $9,600 Fourth and Later Years $5,860 $5,760 $5,760 "Because the 2022 indexed amounts were not available when we published, the 2021 amounts are used in the Examples and end-of-chapter problem materials. On March 30, 2021, Leo purchased and placed in service a new car that cost $55,200. The business use percentage for the car is always 100%. He does not take the additional first-year depreciation or any § 179. If required, round your answers to the nearest dollar. Click here to access the depreciation table of the textbook. Click here to access the limits for certain automobiles. a. What MACRS convention applies to the new car? Half-year b. Is the automobile considered "listed property"? Yes c. Leo's cost recovery deduction in 2021 is $ and for 2022 is $1 Exhibit 8.3 MACRS Accelerated Depreciation for Personal Property Assuming Half-Year Convention (Percentage Rates) For Property Placed in Service after December 31, 1986 3-Year (200% DB) 5-Year (200% DB) Recovery Year 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 33.33 44.45 14.81* 7.41 20.00 32.00 19.20 11.52* 11.52 5.76 *Switchover to straight-line depreciation. 7-Year (200% DB) 14.29 24.49 17.49 12.49 8.93* 8.92 8.93 4.46 10-Year (200% DB) 10.00 18.00 14.40 11.52 9.22 7.37 6.55* 6.55 6.56 6.55 3.28 15-Year (150% DB) 5.00 9.50 8.55 7.70 6.93 6.23 5.90* 5.90 5.91 5.90 5.91 5.90 5.91 5.90 5.91 2.95 20-Year (150% DB) 3.750 7.219 6.677 6.177 5.713 5.285 4.888 4.522 4.462* 4.461 4.462 4.461 4.462 4.461 4.462 4.461 4.462 4.461 4.462 4.461 2.231 Exhibit 8.4 MACRS Accelerated Depreciation for Personal Property Assuming Mid-Quarter Convention (Percentage Rates) For Property Placed in Service after December 31, 1986 (Partial Table * ) 3-Year First Quarter Second Quarter Recovery Year 1 2 Recovery Year 1 2 58.33 27.78 First Quarter 35.00 26.00 41.67 38.89 5-Year Second Quarter 25.00 30.00 7-Year Third Quarter 25.00 50.00 Third Quarter 15.00 34.00 Fourth Quarter 8.33 61.11 Fourth Quarter 5.00 38.00 + Exhibit 8.3 MACRS Accelerated Depreciation for Personal Property Assuming Half-Year Convention (Percentage Rates) For Property Placed in Service after December 31, 1986 3-Year (200% DB) 5-Year (200% DB) Recovery Year 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 33.33 44.45 14.81* 7.41 20.00 32.00 19.20 11.52* 11.52 5.76 *Switchover to straight-line depreciation. 7-Year (200% DB) 14.29 24.49 17.49 12.49 8.93* 8.92 8.93 4.46 10-Year (200% DB) 10.00 18.00 14.40 11.52 9.22 7.37 6.55* 6.55 6.56 6.55 3.28 15-Year (150% DB) 5.00 9.50 8.55 7.70 6.93 6.23 5.90* 5.90 5.91 5.90 5.91 5.90 5.91 5.90 5.91 2.95 20-Year (150% DB) 3.750 7.219 6.677 6.177 5.713 5.285 4.888 4.522 4.462* 4.461 4.462 4.461 4.462 4.461 4.462 4.461 4.462 4.461 4.462 4.461 2.231 Exhibit 8.5 MACRS Straight-Line Depreciation for Personal Property Assuming Half-Year Convention * For Property Placed in Service after December 31, 1986 MACRS Class 3-year 5-year 7-year 10-year 15-year 20-year Note: The last two rows of this table are used for qualified improvement property (15-year normal MACRS; 20-year ADS). % First Recovery Year 16.67 10.00 7.14 5.00 3.33 Other Recovery Years Last Recovery Year % % 2.50 Years 2-3 2-5 2-7 2-10 2-15 2-20 33.33 20.00 14.29 10.00 6.67 5.00 Year 4 6 8 11 16 21 16.67 10.00 7.14 5.00 3.33 2.50 Exhibit 8.6 Alternative Minimum Tax: 150% Declining-Balance Assuming Half-Year Convention (Percentage Rates) For Property Placed in Service after December 31, 1986 (Partial Table*) 5-Year 9.5-Year 150% 150% Recovery Year 1 2 3 4 6 7 8 9 10 11 123 3-Year 150% 25.00 37.50 25.00** 12.50 15.00 25.50 17.85 16.66** 16.66 8.33 7-Year 150% 10.71 19.13 15.03 12.25** 12.25 12.25 12.25 6.13 7.89 14.54 12.25 10.31 9.17** 9.17 9.17 9.17 9.17 9.16 10-Year 150% 7.50 13.88 11.79 10.02 8.74** 8.74 8.74 8.74 8.74 8.74 4.37 12-Year 150% 6.25 11.72 10.25 8.97 7.85 7.33** 7.33 7.33 7.33 7.33 7.32 7.33 3.66 *The figures in this table are taken from the official table that appears in Rev.Proc. 87-57. Because of its length, the complete table is not presented. **Switchover to straight-line depreciation. Exhibit 8.7 ADS Straight-Line for Personal Property Assuming Half-Year Convention (Percentage Rates) For Property Placed in Service after December 31, 1986 (Partial Table) * Recovery Year 3-Year 5-Year 7-Year 10-Year 16.67 10.00 33.33 20.00 20.00 20.00 20.00 10.00 1 2 3 4 5 6 7 8 لیا 33.33 16.67 7.14 14.29 14.29 14.29 14.29 14.29 14.29 7.14 5.00 10.00 10.00 10.00 10.00 10.00 10.00 10.00 12-Year 4.17 8.33 8.33 8.33 8.33 8.33 8.34 8.33 + For Property Placed in Service after December 31, 1986: 27.5-Year Residential Real Property Recovery The Applicable Percentage Is (Use the Column for the Month in the First Year the Property Is Placed in Service): Year(s) 1 2 3 4 5 6 7 8 10 11 3.485 3.182 2.576 2.273 1.970 3.636 3.636 3.636 2.879 3.636 3.636 3.636 3.637 3.637 3.637 1.970 2.273 2.576 2.879 3.182 0.000 0.000 0.000 0.000 0.000 3.637 3.637 1 2-18 19-27 28 29 1 2-19 20-31 For Property Placed in Service after December 31, 1986, and before May 13, 1993: 31.5-Year Nonresidential Real Property Recovery The Applicable Percentage Is (Use the Column for the Month in the First Year the Property Is Placed in Service): Year(s) 1 2 3 4 5 6 7 8 9 10 11 32 33 3.042 2.778 2.513 3.175 3.175 3.175 3.174 1.720 0.000 1 2-39 40 9 1.364 1.061 0.758 0.455 3.636 3.636 3.636 3.636 1.667 3.636 3.637 3.637 3.637 3.637 3.637 3.637 3.485 3.636 3.636 3.636 3.636 3.636 0.000 0.152 0.455 0.758 1.061 1.364 1 2.461 2.564 0.107 3.175 3.174 3.174 3.174 1.984 2.249 2.513 2.778 0.000 0.000 0.000 0.000 2.249 1.984 1.720 3.175 3.175 3.175 3.174 3.174 3.174 3.042 3.175 0.000 0.132 1.455 1.190 3.175 3.174 3.175 0.397 0.926 0.661 3.175 3.175 3.174 3.174 3.174 3.175 3.175 3.175 0.661 0.926 1.190 0.397 3.175 12 0.152 3.636 3.637 3.636 1.667 For Property Placed in Service after May 12, 1993: 39-Year Nonresidential Real Property Recovery The Applicable Percentage Is (Use the Column for the Month in the First Year the Property is placed in Service): Year(s) 2 3 4 5 6 7 8 9 10 11 1.177 0.963 0.749 2.247 2.033 1.819 1.605 1.391 2.564 2.564 2.564 0.749 0.963 1.177 1.391 1.605 1.819 2.564 2.564 2.564 2.564 2.564 0.321 0.535 0.535 0.321 2.564 2.564 2.033 2.247 12 0.132 3.175 3.174 3.175 1.455 12 0.107 2.564 2.461 Date Placed in Service 2021* 2019-2020 2018 First Year $10,200 $10,100 $10,000 Second Year $16,400 $16,100 $16,000 Third Year $9,800 $9,700 $9,600 Fourth and Later Years $5,860 $5,760 $5,760 "Because the 2022 indexed amounts were not available when we published, the 2021 amounts are used in the Examples and end-of-chapter problem materials.

Expert Answer:

Answer rating: 100% (QA)

a The halfyear convention applies to the new car because it was placed in service in the first quarter of the year b Yes the automobile is considered ... View the full answer

Related Book For

South-Western Federal Taxation 2022 Individual Income Taxes

ISBN: 9780357519073

45th Edition

Authors: James C. Young, Annette Nellen, William A. Raabe, Mark Persellin, William H. Hoffman

Posted Date:

Students also viewed these accounting questions

-

A researcher wanted to find out if there was difference between older movie goers and younger movie goers with respect to their estimates of a successful actors income. The researcher first...

-

Account Titles cash in bank ordinary share capital share premium-ordinary preference share share premium-ps ppe-building ppe-land mortgage payable ppe-office furnitures & Notes Payable Smallspoon...

-

GENERAL INSTRUCTIONS: You will execute multiple regression models using data in the worksheets, "Time Series Data" and "Cross Sectional Data." For all regressions, you will use the same dependent...

-

Toby dies on 2 March 2021, leaving an estate valued at 400,000. None of the transfers made on death are exempt from IHT. Calculate the IHT due on the estate if the total of the gross chargeable...

-

Best Buy and Circuit City are competitors, and both sell products through their Websites and in retail stores. Compare these companies income statements and answer the following. Required 1. Which...

-

An infinitely long straight wire carries a current I = 1.0 A that flows in the positive direction. The external magnetic field at position x along the wire is given by B(x) = Boe||/ay where Bo = 110...

-

What are the requirements of a modern surface condenser ?

-

The December 31, 2015, unadjusted trial balance for Demon Deacons Corporation is presented below. At year-end, the following additional information is available: a. The balance of Prepaid Rent,...

-

The Alpine House, Incorporated, is a large retailer of snow skis. The company assembled the Information shown below for the quarter ended March 31: Sales Selling price per pair of skis Variable...

-

(a) Prepare income statements for January and February for Fazli, Gervais, and Consolidation. Break down cost of sales into its three components. (b) Now assume that Fazli uses the equity method to...

-

Complete the following calculations. Find the uncertainty in each calculated value by the propagation of errors method. 1. It takes 10.5(1) s for a sprinter to run 100.00(5) m. Calculate the average...

-

Why is test anxiety a good thing? What are the three fears that cause anxiety? How do overcome these fears? What are some activities you can do to reduce test anxiety? Should you entirely deal with...

-

Road Builders Ltd. was the successful bidder for a contract with a provincial government to construct a 23- kilometre highway by-pass of a large city. As a part of its preparation for the contract...

-

For many organizations, a major problem is cultural blindness. In organizations you know, what factors cause managers to remain blind to the impact of cultural diversity?

-

To employ an employee the organization would look at 3 elements describe what are those elements?

-

Do you think that vacation days are a form of incentives? Why do you think so? provide brief explanation.

-

Bharath Ltd. is a new company. It has come up with the initial public issue. The issue price of the share is Rs 20 and the par value is Rs 10. Sudhakar, a prospective investor, is considering...

-

Show that gj concave AHUCQ Abadie For nonnegative variables, we have the following corollary.

-

Myers, who is single, has compensation income of $73,000 in 2021. He is an active participant in his employers qualified retirement plan. Myers contributes $6,000 to a traditional IRA. Of the $6,000...

-

Bob and Nancy are married and file a joint return in 2020. They are both under age 50 and employed, with wages of $50,000 each. Their total AGI is $112,000. Neither of them is an active participant...

-

In 2021, Chaya Corporation, an accrual basis, calendar year taxpayer, provided services to clients and earned $25,000. The clients signed notes receivable to Chaya that have a fair market value of...

-

Form a small group. Concentrate on BSE Sensex companies and compile the voluntary disclosures made by each of them. Draft a crisp research paper highlighting your findings and use thereof to various...

-

Billy Ray Nibert was convicted of capital murder in the Circuit Court, Hillsborough County and he appealed. The Supreme Court of Florida affirmed the conviction, vacated the death sentence and...

-

Hassan Abu-Jihaad was convicted of disclosing national defense information and of providing material support to terrorist by a jury in the District Court of Connecticut. Abu-Jihaad moved for a...

Study smarter with the SolutionInn App