Question: only a final answer is needed. Consider the two (excess return) index-model regression results for equities funds A and B. The risk-free rate over the

only a final answer is needed.

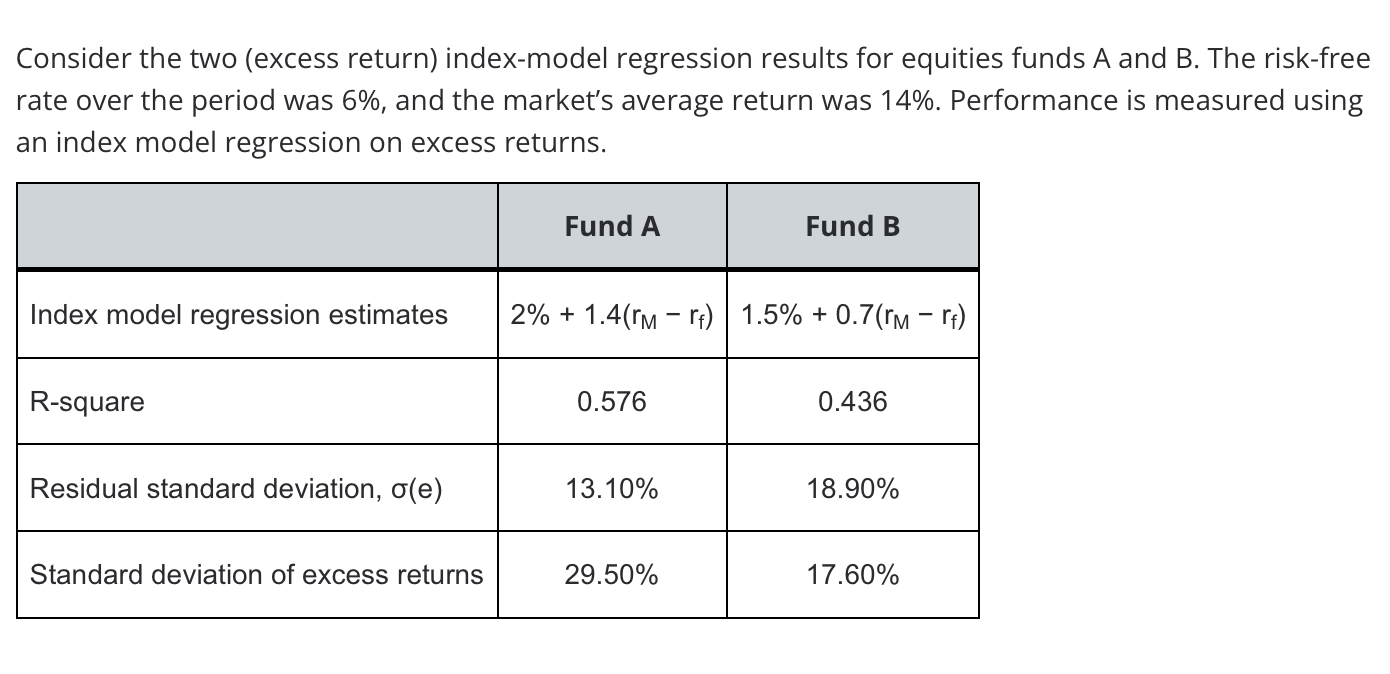

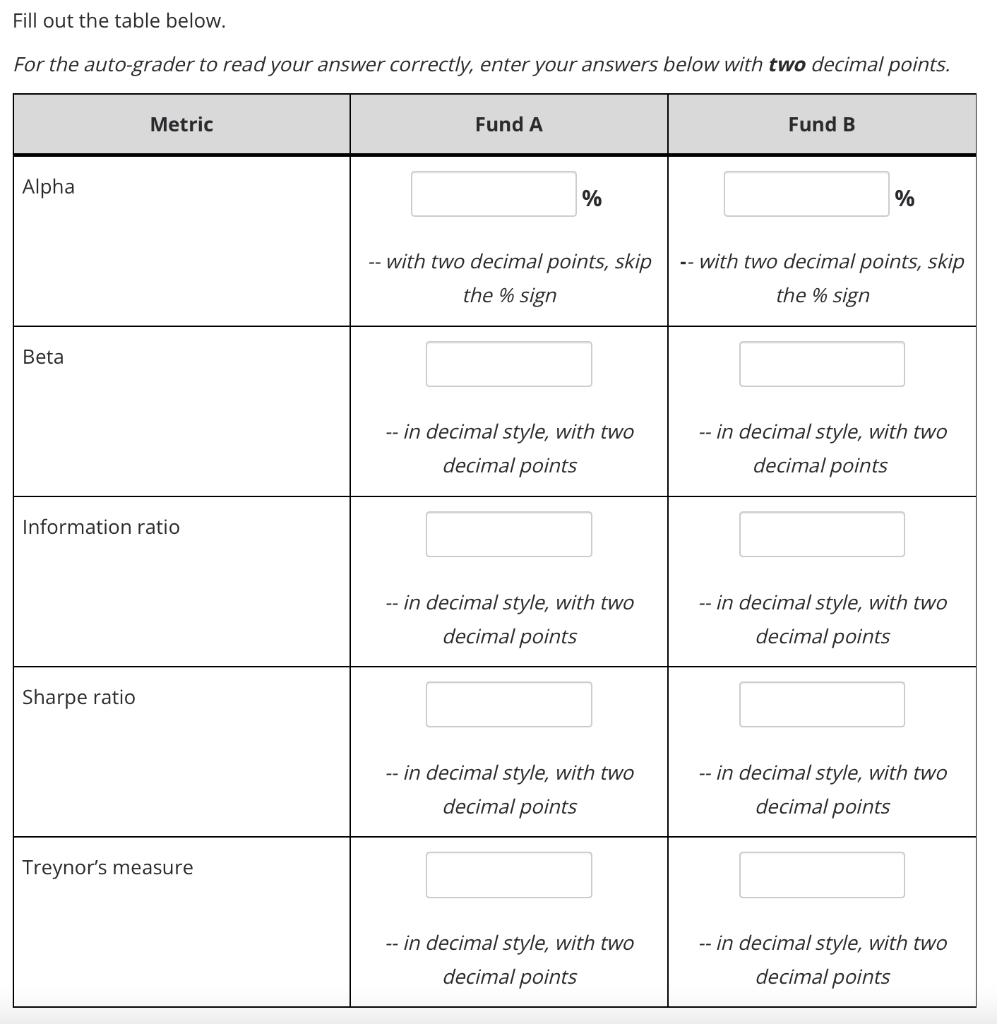

Consider the two (excess return) index-model regression results for equities funds A and B. The risk-free rate over the period was 6%, and the market's average return was 14%. Performance is measured using an index model regression on excess returns. Fund A Fund B Index model regression estimates 2% + 1.4(rm rf) 1.5% +0.7(rm rf) R-square 0.576 0.436 Residual standard deviation, o(e) 13.10% 18.90% Standard deviation of excess returns 29.50% 17.60% Fill out the table below. For the auto-grader to read your answer correctly, enter your answers below with two decimal points. Metric Fund A Fund B Alpha % % -- with two decimal points, skip the % sign -- with two decimal points, skip the % sign Beta -- in decimal style, with two decimal points -- in decimal style, with two decimal points Information ratio -- in decimal style, with two decimal points -- in decimal style, with two decimal points Sharpe ratio -- in decimal style, with two decimal points -- in decimal style, with two decimal points Treynor's measure -- in decimal style, with two decimal points -- in decimal style, with two decimal points

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts