Question: Only answer 5.7 a&b ercises 5.2-5.9 make use of the following information Ex about the mean returns and covariances for three stocks. The numbers used

Only answer 5.7 a&b

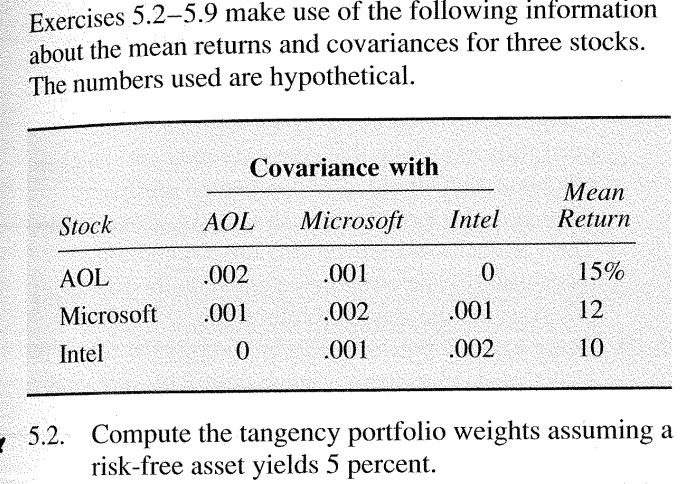

ercises 5.2-5.9 make use of the following information Ex about the mean returns and covariances for three stocks. The numbers used are hypothetical Covariance with Mean AOL MicrosoftIntelReturn Stock AOL Intel 001 002 001 15% 12 10 002 Microsoft001 0 0 001 002 Compute the tangency portfolio weights assuming a risk-free asset yields 5 percent. 5.2. ercises 5.2-5.9 make use of the following information Ex about the mean returns and covariances for three stocks. The numbers used are hypothetical Covariance with Mean AOL MicrosoftIntelReturn Stock AOL Intel 001 002 001 15% 12 10 002 Microsoft001 0 0 001 002 Compute the tangency portfolio weights assuming a risk-free asset yields 5 percent. 5.2

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts