Question: ONLY ANSWER D ) last question Problem 10 Here are data on five mutual funds: Fund Return Standard Deviation Beta A 14 6 1.5 B

ONLY ANSWER D ) last question

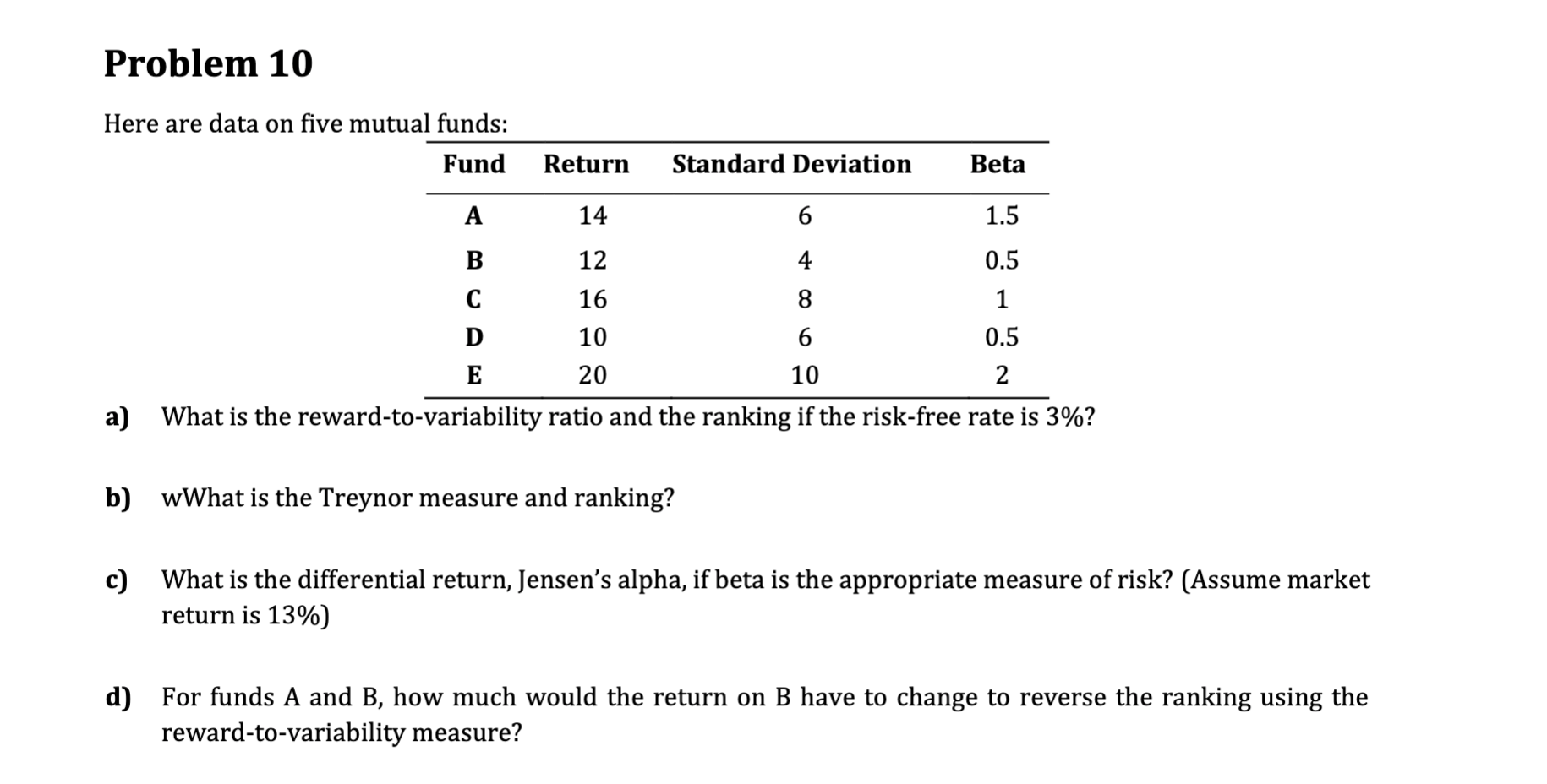

Problem 10 Here are data on five mutual funds: Fund Return Standard Deviation Beta A 14 6 1.5 B 12 4 0.5 16 8 1 D 10 6 0.5 E 20 10 2 a) What is the reward-to-variability ratio and the ranking if the risk-free rate is 3%? b) wWhat is the Treynor measure and ranking? c) What is the differential return, Jensen's alpha, if beta is the appropriate measure of risk? (Assume market return is 13%) d) For funds A and B, how much would the return on B have to change to reverse the ranking using the reward-to-variability measure

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock