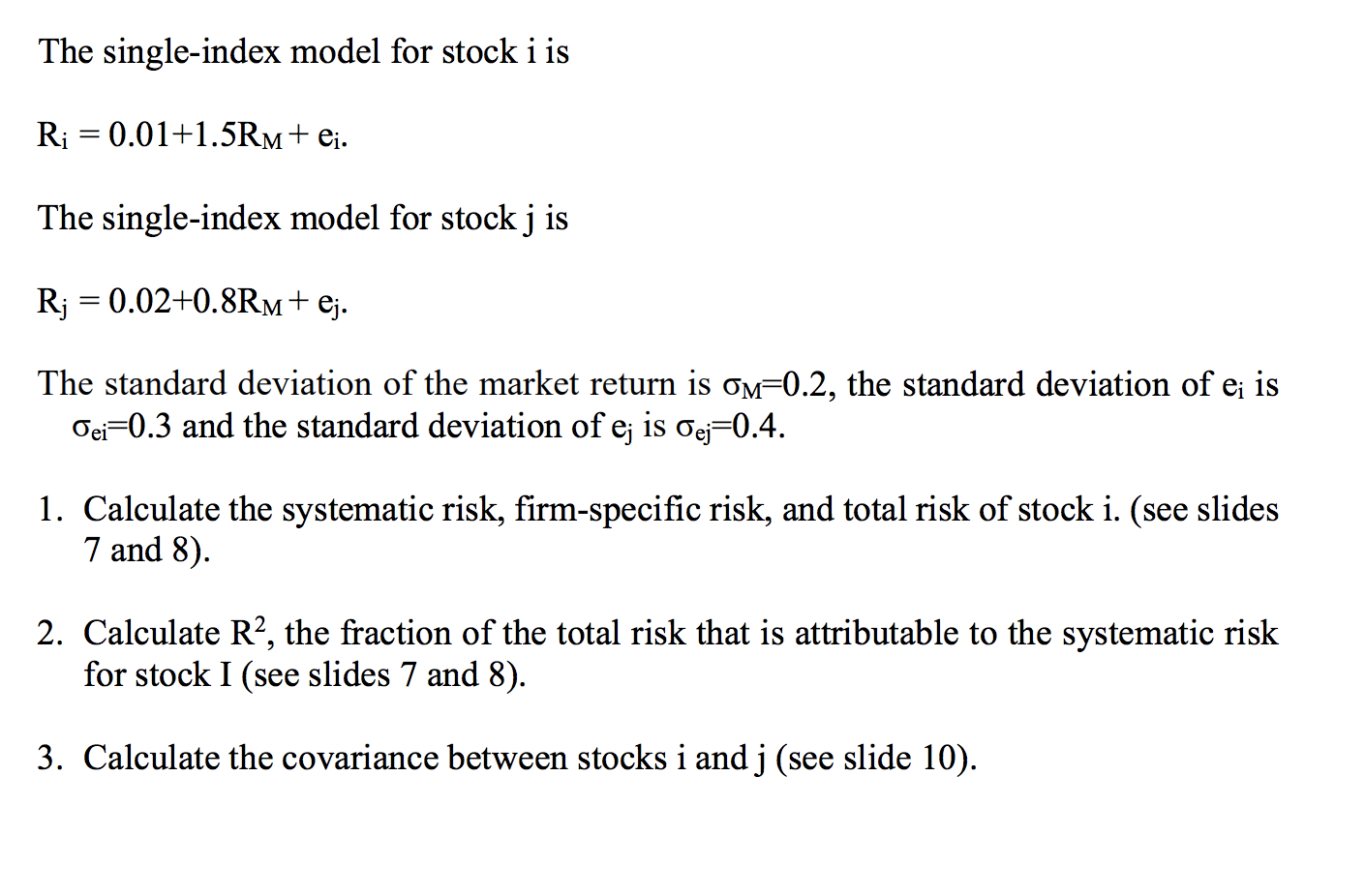

Question: Only answer question 3 please. Systematic risk= .09, Firm specific risk=.09, Total risk= 0.18, R2=49.9% The single-index model for stock i is R; = 0.01+1.5Rm+

Only answer question 3 please.

Systematic risk= .09, Firm specific risk=.09, Total risk= 0.18, R2=49.9%

The single-index model for stock i is R; = 0.01+1.5Rm+ ej. The single-index model for stock j is Rj = 0.02+0.8Rm+ ej. The standard deviation of the market return is om=0.2, the standard deviation of e; is Oei=0.3 and the standard deviation of ej is dej=0.4. 1. Calculate the systematic risk, firm-specific risk, and total risk of stock i. (see slides 7 and 8). 2. Calculate R2, the fraction of the total risk that is attributable to the systematic risk for stock I (see slides 7 and 8). 3. Calculate the covariance between stocks i and j (see slide 10)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts