Question: Only need help with the second part which starts with consider the same problem as above, but suppose.... Thanks a lot! Consider a finite-horizon investment

Only need help with the second part which starts with "consider the same problem as above, but suppose...". Thanks a lot!

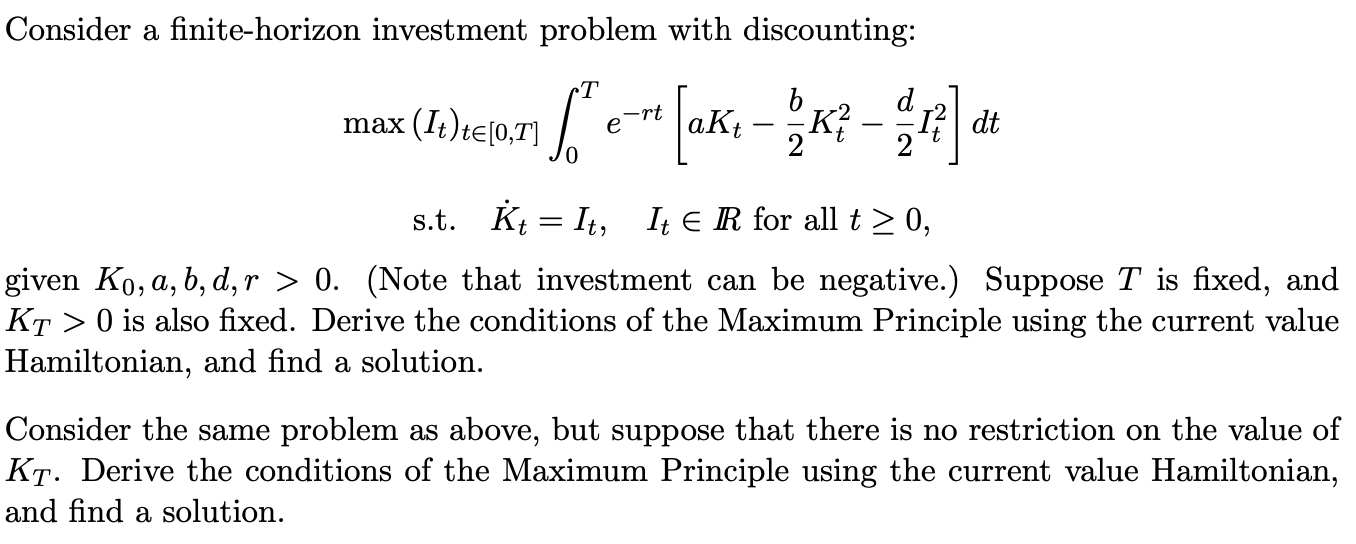

Consider a finite-horizon investment problem with discounting: max(It)t[0,T]0Tert[aKt2bKt22dIt2]dt s.t. Kt=It,ItR for all t0, given K0,a,b,d,r>0. (Note that investment can be negative.) Suppose T is fixed, and KT>0 is also fixed. Derive the conditions of the Maximum Principle using the current value Hamiltonian, and find a solution. Consider the same problem as above, but suppose that there is no restriction on the value of KT. Derive the conditions of the Maximum Principle using the current value Hamiltonian, and find a solution. Consider a finite-horizon investment problem with discounting: max(It)t[0,T]0Tert[aKt2bKt22dIt2]dt s.t. Kt=It,ItR for all t0, given K0,a,b,d,r>0. (Note that investment can be negative.) Suppose T is fixed, and KT>0 is also fixed. Derive the conditions of the Maximum Principle using the current value Hamiltonian, and find a solution. Consider the same problem as above, but suppose that there is no restriction on the value of KT. Derive the conditions of the Maximum Principle using the current value Hamiltonian, and find a solution

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts