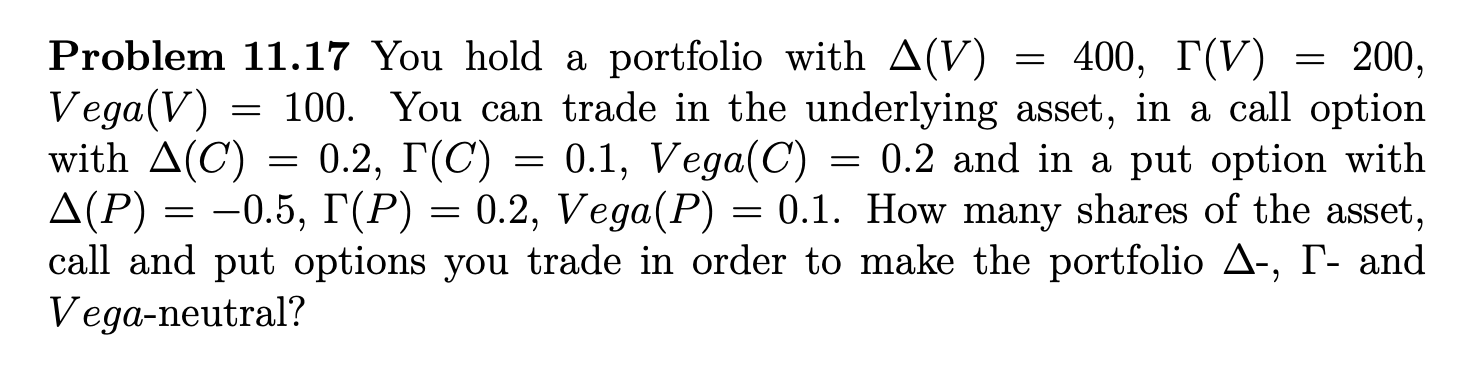

Question: (Only typing....don't upload photos for answer) . Problem 11.17 You hold a portfolio with A(V) = 400, T(V) = 200, Vega(V) = 100. You can

(Only typing....don't upload photos for answer)

.

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock